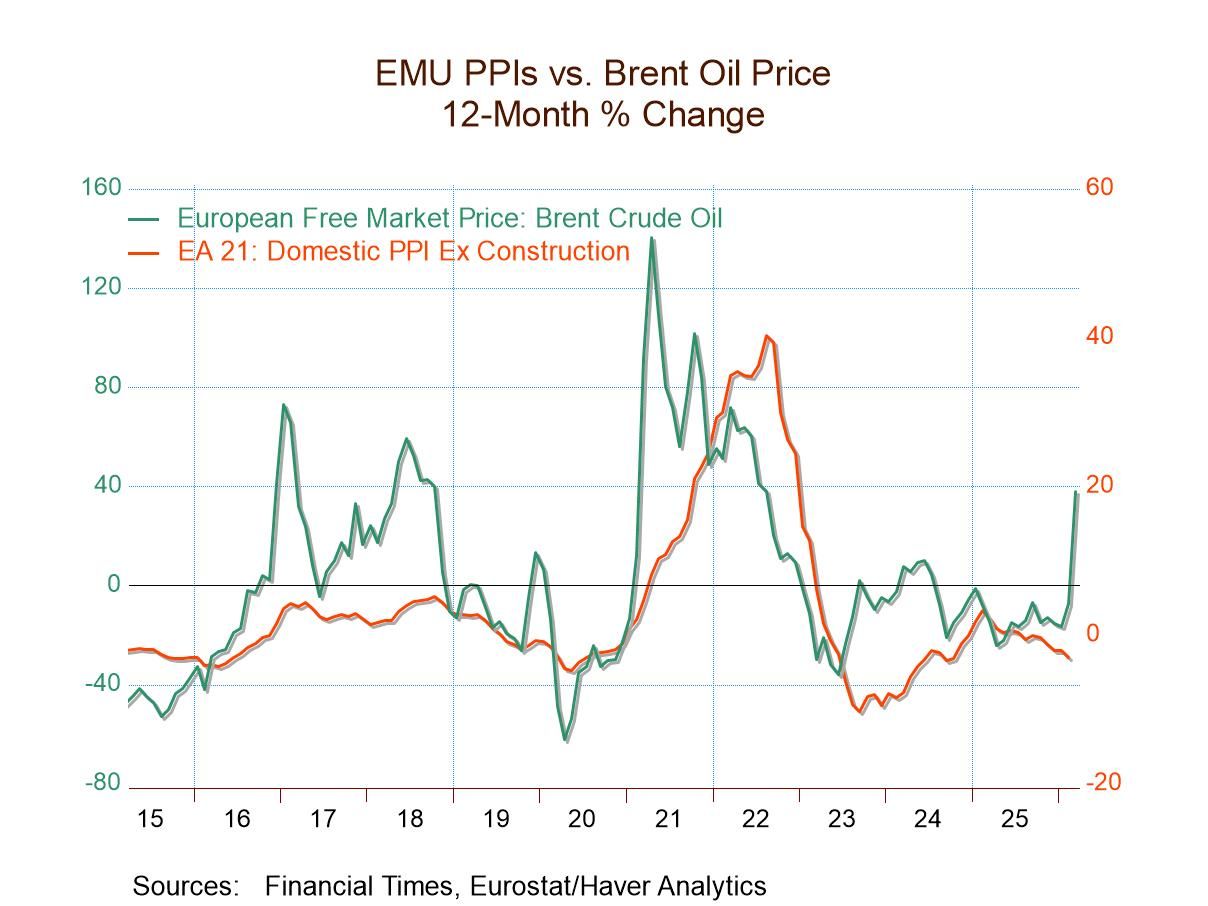

EMU PPI Trends Are Chaotic; It Could Get Worse

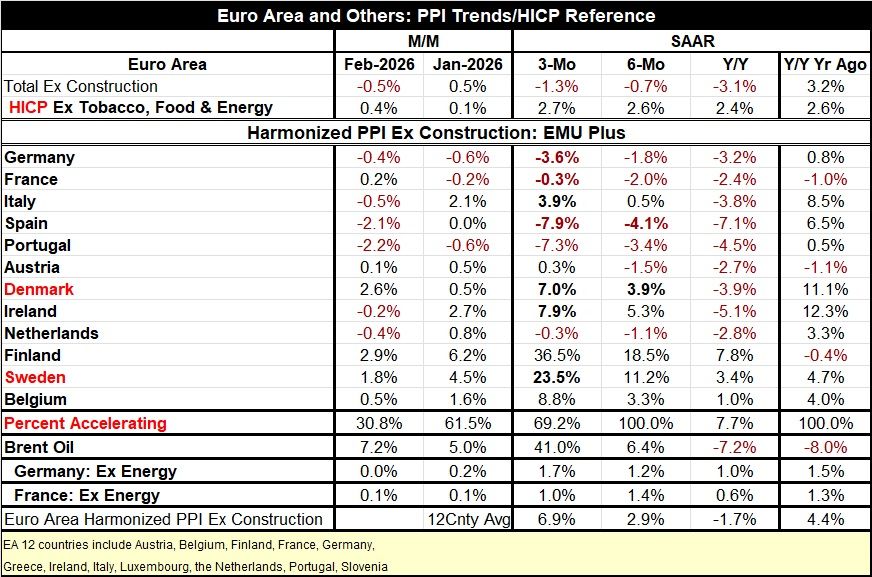

Chaotic trends Producer price trends for the European Monetary Union in February show great deal of weakness. The headline measure in February for total PPI prices (excluding construction) fell 0.5% after rising 0.5% in January. The three-month annualized change was -1.3%, over six months it was -0.7%, and year-over-year it was -3.1%. The trend is not particularly conclusive although the table also produces the trend for the HICP-core on the same timeline where there is acceleration in train. Despite this report and any trends, it may show that the risk to inflation in the PPI is now through elevated Brent crude prices, which we see in the chart has been historically well correlated with changes in the PPI.

The past may not be prologue The chart offers some insight into this matter as we see that recently the spike in Brent crude is substantial—and the chart doesn't even take us up-to-date to what we're dealing with in the markets today! We can see that in 2021 when all prices went up sharply, that preceded a spike in the PPI as well. However, in 2017 when there was a short-lived spike, there wasn't much impact on producer prices at all. Then, later in 2018, when prices spiked not quite so high or suddenly, but had a bit more sustained growth, there also was a very small knock-on impact on producer prices. One of the key features for whether the Brent rise gets into producer prices or not is how long-lived the spike remains in force and how people perceive it. In this case, there's closing of the Strait of Hormuz and a war in place; there's a good chance that investors are going to treat this as a real event and one with potential longevity. That means that this spike will elevate producer prices.

Overall PPI is tempered but, by country...not so much However, the table is based on data through February, and so oil spiking prices really haven't entered the picture as far as the table is concerned. On that basis, we're seeing a lot of price declines: an annualized three-month decline of 7.9% in Spain, 7.3% in Portugal, 3.6% in Germany, and so on. These figures clearly do not reflect what will be the lasting effect on oil prices as we get deeper into 2026. Even despite this weakness in headline inflation across countries in the monetary union, and in Europe generally, inflation is tempered year-over-year where it only rises compared to a year earlier for 7.7% of the reporters, but then over six months inflation accelerates for all of the reporters compared to its 12-month pace, and then, over three months it accelerates for about 70% of the reporters compared to the six-month pace.

PPI headline vs. core... where available There are two observations at the bottom of the table for the PPI excluding energy—for France and Germany. In both cases, the difference between the excluding energy price and the headline price is remarkable. For Germany, the ex-energy price is rising and clearly accelerating; in contrast, the headline trends show prices declining or a tendency toward deceleration. For France, the ex-energy prices are rising and sustaining larger increases over six months and three months than over 12 months. However, for France, in the table, the total PPI headline inflation rate declines on all horizons although the pace of decline is undergoing erosion. Once we set aside the weighting scheme for the monetary union, the PPI is looking instead at the average result of the countries in the table (an average that includes some non-monetary union members) where the inflation rate is clearly headed higher, not lower.

The trend and the future Despite the controversies implicit in these data, at its last meeting the European Central Bank put markets on notice that, if the war were still ongoing, there was a high likelihood that the ECB would raise interest rates at its next meeting. It's easy to see why since the inflation picture isn't particularly glowing. Even before the new oil price impact is factored in, there is evidence of acceleration in producer prices.

War! And price trends War creates a lot of uncertainty. In addition to oil prices, there are going to be knock-on effects for weakness across the global economy and also a tendency for oil prices to spread increases since the oil price increase is high enough that it's likely to have a significant impact on transportation costs for all goods. Central banks are clearly going to be on notice and wary. Even so, it's also true that spiking oil prices, even if they spread inflation, tend to spread economic weakness. Policymaking in 2026 is going to be far more contentious and difficult than it was in 2025, everywhere globally.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia