EMU Inflation Surges; Core Clings to Old Trend

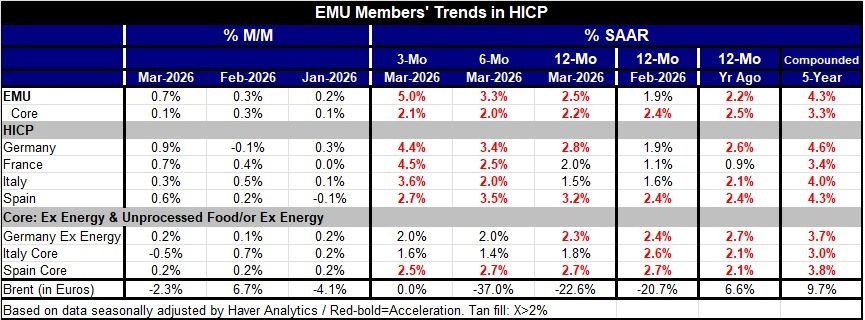

Inflation has begun to flash higher in the euro area as the early inflation indicators in March show an increase of 0.7% month-to-month, even as the core sticks to a low reading of 0.1% in March.

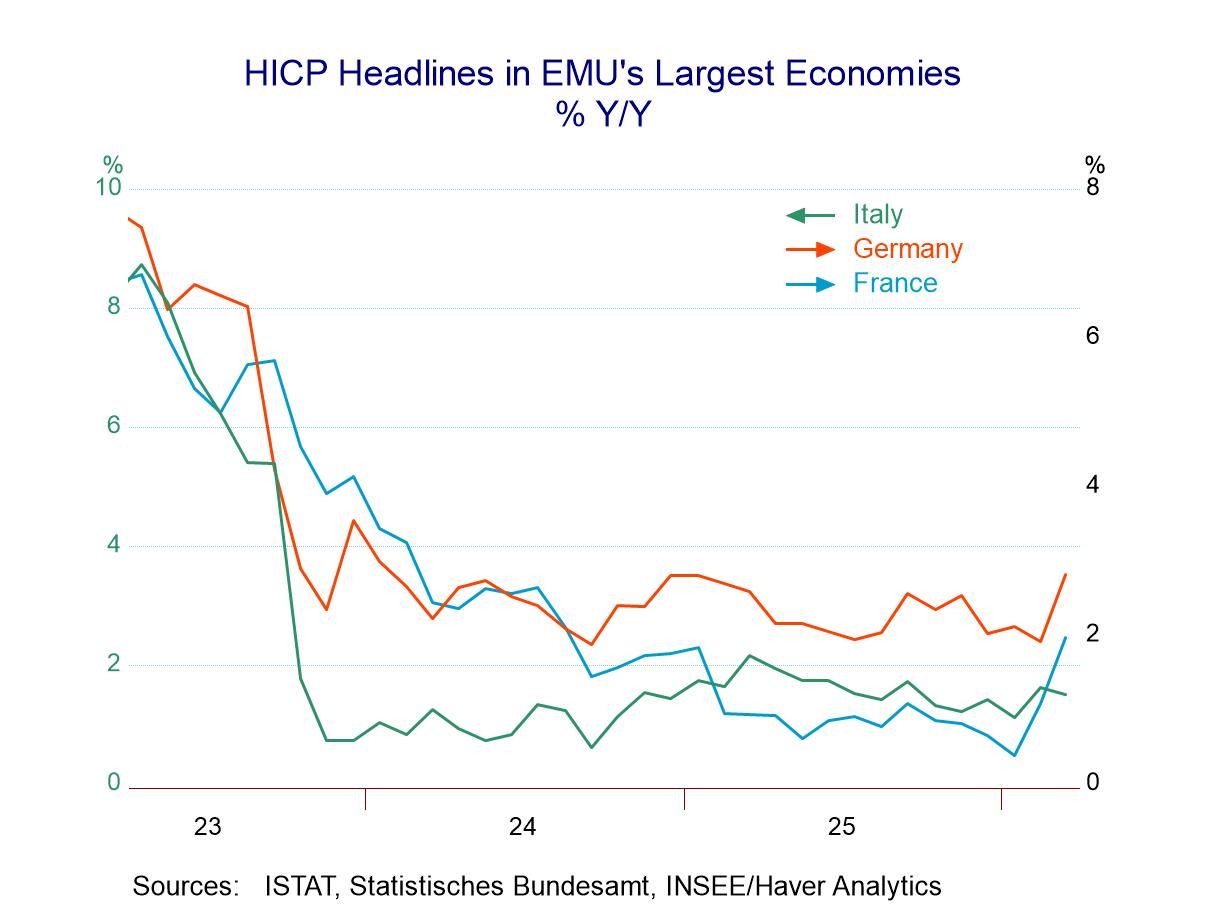

Large economy HICP headlines show pressure The month-to-month increases in the large economies and the monetary union are giving off uncomfortable readings, with Germany posting a 0.9% increase month-to-month, France 0.7%, Italy a more subdued 0.3%, and Spain 0.6%. These numbers help to produce excessive 3-month inflation rates of 4.4% annualized for Germany, 4.5% for France, 3.6% for Italy, and 2.7% for Spain—all of them over the top (that expression, of course, refers to European Central Bank’s inflation objective of 2%).

Year-on-year trends What I listed above are the three-month annualized inflation rates. What the ECB is more interested in is the more-subdued and better-behaved year-over-year rate. On that score, the year-over-year rate is 2.8% for Germany, 2% for France, 1.5% for Italy, and 3.2% for Spain. For the European Monetary Union as a whole, it is 2.5%, while for the EMU core, inflation is 2.2%.

In terms of the year-over-year inflation rates, Germany and Spain are clearly excessive. France is basically on the money for target, while Italian inflation is running cool. GDP-weighted inflation in the monetary union is too high at 2.5%, and on a core basis, it is at what is probably an acceptable 2.2% pace—above target but not demonstrably so.

Core inflation Core inflation or ex-energy inflation, for the three countries that report early show the ex-energy inflation rate for Germany at 2.3% over 12 months; in Italy it is 1.8%, and for Spain it is 2.7%. The core inflation rates are on the high side—not extraordinary, but nevertheless elevated—and the headline inflation rates themselves are accelerating. Looking at the 3-month, 6-month and 12-month inflation rates, we see acceleration in play for Germany, France, Italy, and Spain, as well as, for the monetary union as a whole where the 3-month inflation rate has reached 5% annualized (yikes!).

Oil…no! Don’t blame oil yet—that lies ahead We know that oil prices are spurting, but on this timeline ending in March, Brent oil prices measured in euros fell by 2.3%, and year-over-year Brent oil prices are down by 22.6%. So these results are yet to be clobbered by events in the Middle East—events that have lifted oil prices and other energy costs quite dramatically.

ECB is on Guard — Christine Lagarde It's not surprising that amid these pressures the European Central Bank, as well as the Bank of England, have said that if the war continues at the time of their next meeting, it's likely that they'll hike rates. However, in the United States, the Fed continues to be coy and to give us no guidance and to talk in terms that suggest it is still, in some sense, ‘data dependent’ although this does not seem to be a time to be data dependent. Policymaking now is really a bet on how the war in the Middle East progresses and whether the Strait of Hormuz is going to be opened, and that has very little to do with looking back at past data.

A new frontier…for some

Policymaking seems to have moved into a new frontier although it seems clear that all the policymakers have realized this. The Federal Reserve, which usually likes to fancy itself as being on the frontier of what makes good monetary policy, appears to not yet have grasped the realities of this situation. What we have is a situation where a Fed chair has been pursuing a certain policy for a prolonged period—prioritizing the labor market

Consistent error and bias This unfortunate constellation of events of communication and of poor forecasting has led to five continuous years of inflation overshooting by the Federal Reserve and most other central banks. Let’s admit that when the anchor currency’s policies are adrift, it is harder for others to control their own inflation, rather than giving the Fed ‘a pass’ because global inflation has been high.

OK…blame events—but blame inaction, too While the Fed can look back and blame COVID, blame tariffs, blame the war in Ukraine, and blame problems in the Middle East, it can also look in the mirror and blame itself—time and time again. Through all of these distractions, the Federal Reserve never took its eye off of the job market, always putting priority on jobs while diverting attention from the overshoot of the inflation target. All through this time, the Fed tried to characterize itself as weighting both sides of the dual mandate equally, although with the unemployment rate in the U.S. so low and basically still at a level that could be deemed full employment, and with five years of consistent inflation overshooting and oil prices spurting, the Federal Reserve still isn't ready to say that it's prepared to put its neck on the line to control inflation, or even lean against the wind. What we may be seeing is a replay of the early 1970s, when the Europeans decided that oil price inflation was something they should not ignore, and with the Bundesbank leading the way as interest rates went up, while the Federal Reserve dallied and tried to soften the blow on the economy by raising interest rates less and cutting interest rates early in the process and thereby sealing its own doom in the tomb of excessive inflation.

Not again Christine Lagarde at the ECB has said she does not plan on making the same mistake again. By that, she's referring to the slow rate hikes that the ECB delivered during COVID. To some extent at that time, the ECB, like other central banks, was following the lead of the Federal Reserve that really dragged its feet. Now there is very little evidence that the Fed has learned from that experience.

The manipulation game Between the central bank in the U.S. and the U.S. Treasury, there are serious attempts to try to manipulate inflation expectations to keep them in line and then call them ‘controlled.’ Meanwhile, surveys of inflation expectations, like those from the University of Michigan, show that in some quarters inflation expectations are running wild. Part of the reason for that is noting that central bankers have allowed inflation to overshoot for such a long period of time. So why should they trust the Fed or the ECB over the next 5 or 10 years? They could continue to act this same way for the next five or ten years. The Fed engaged in asset purchases to bring down long-term rates and continues that with ‘QE.’ Now the Treasury has stopped issuing new long-term bonds. This is manipulation.

What’s next Central bankers have a lot to pay attention to, and like the time of the last oil shock in the early 1970s, it looks like—once again—it's the Europeans who want to lead the way toward price stability—not the Americans.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia