Employment Cost Index: Continued Deceleration

Summary

- Vigorous growth during the pandemic-related recovery gives way to moderate advances recently.

- Labor costs seem in line with the Fed’s inflation target.

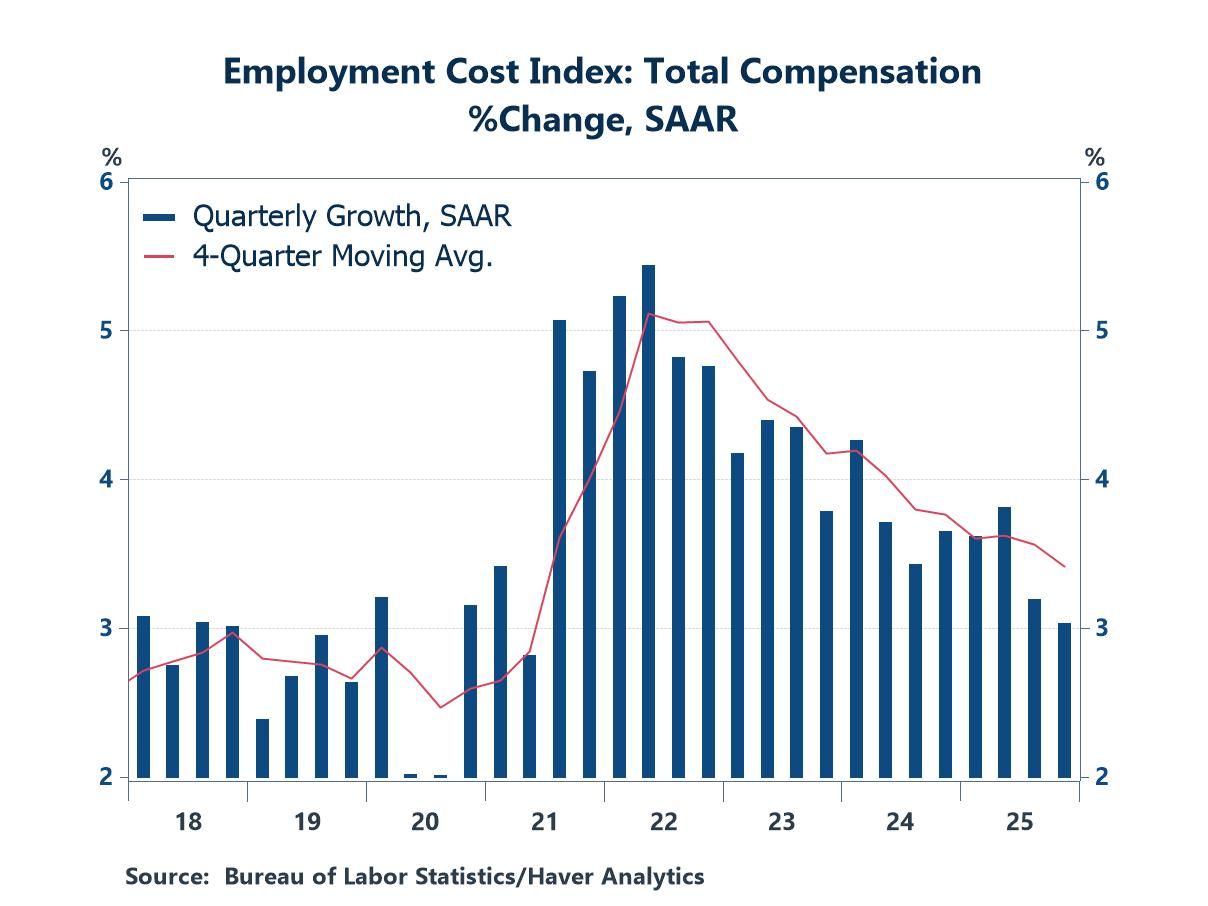

The Employment Cost Index rose at an annual rate of 3.0% in the final three months of 2025 (0.7% not annualized). The latest observation reinforced the deceleration that began in the latter part of 2022 and returned the change to the range in place before the pandemic - albeit the upper portion of that range.

Most of the deceleration occurred in the goods-producing sector, where the latest increase of 2.5% (annual rate) trailed the average of 3.9% in the prior three quarters. The service sector saw compensation growth of 3.1%, down from an average of 3.5% in the prior three quarters. The difference between the performances of goods and service is not surprising, as compensation growth in the goods-producing sector tends to be more volatile, and it has typically been softer in the past few years.

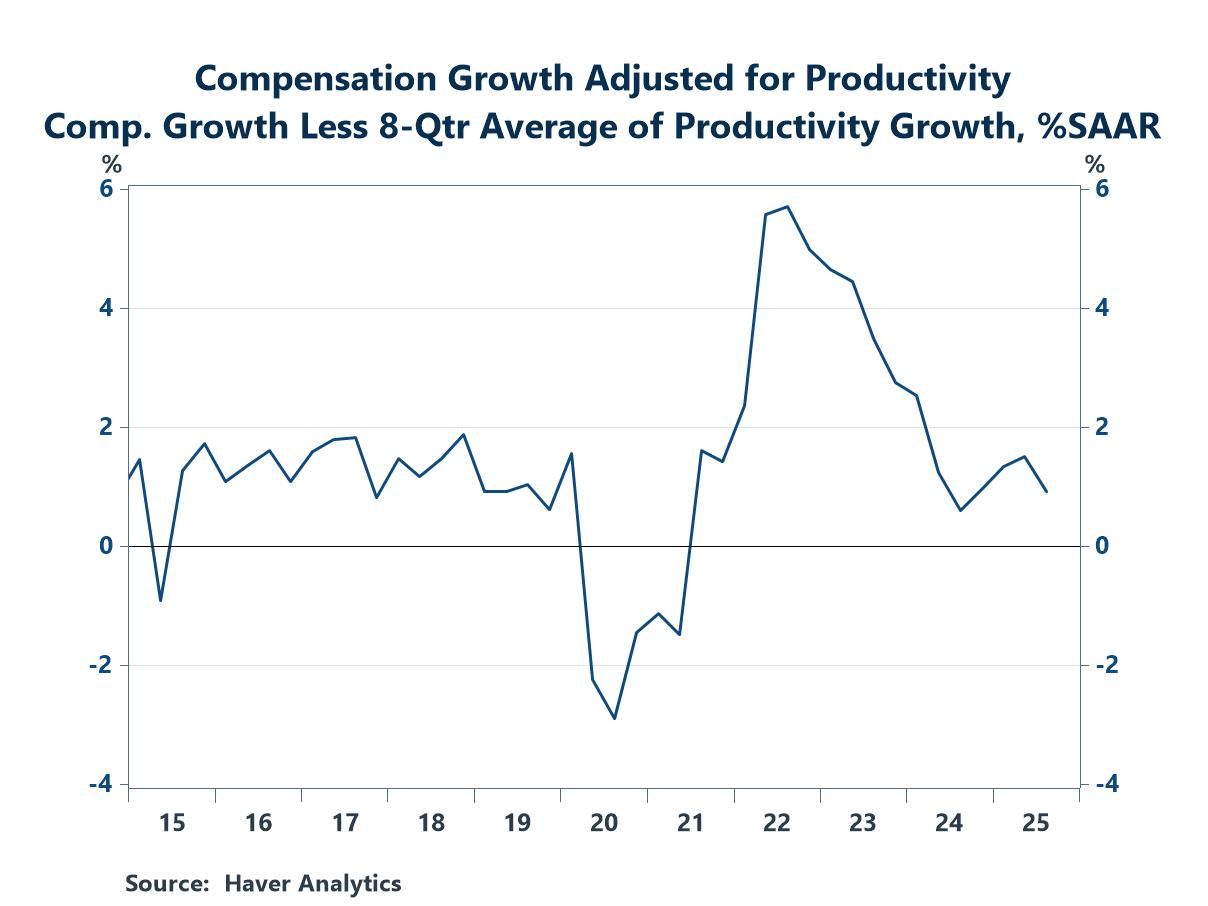

Fed Chair Jerome Powell has argued recently that labor costs are not a driving force behind above-target inflation, and recent results on the employment cost index support this view. While the increase in compensation of 3.0% in Q4 is a percentage point above the Fed’s target, businesses can maintain profits without passing along the full extent of the increase. Productivity growth, which has been strong recently (average growth of 2.3% in the past eight quarters), can effectively offset compensation growth and dampen the inflation impulse.

The chart on the upper right shows quarterly growth in total compensation less the 8-quarter increase in productivity (the 8-quarter average smooths the high degree of volatility in productivity growth). This metric, which gives insight into the likely path of inflation, has been below 2.0% for the past 6 quarters, with the latest increase totaling less than 1.0%. (the chart ends in 2025-Q3 because productivity statistics for Q4 are not available).

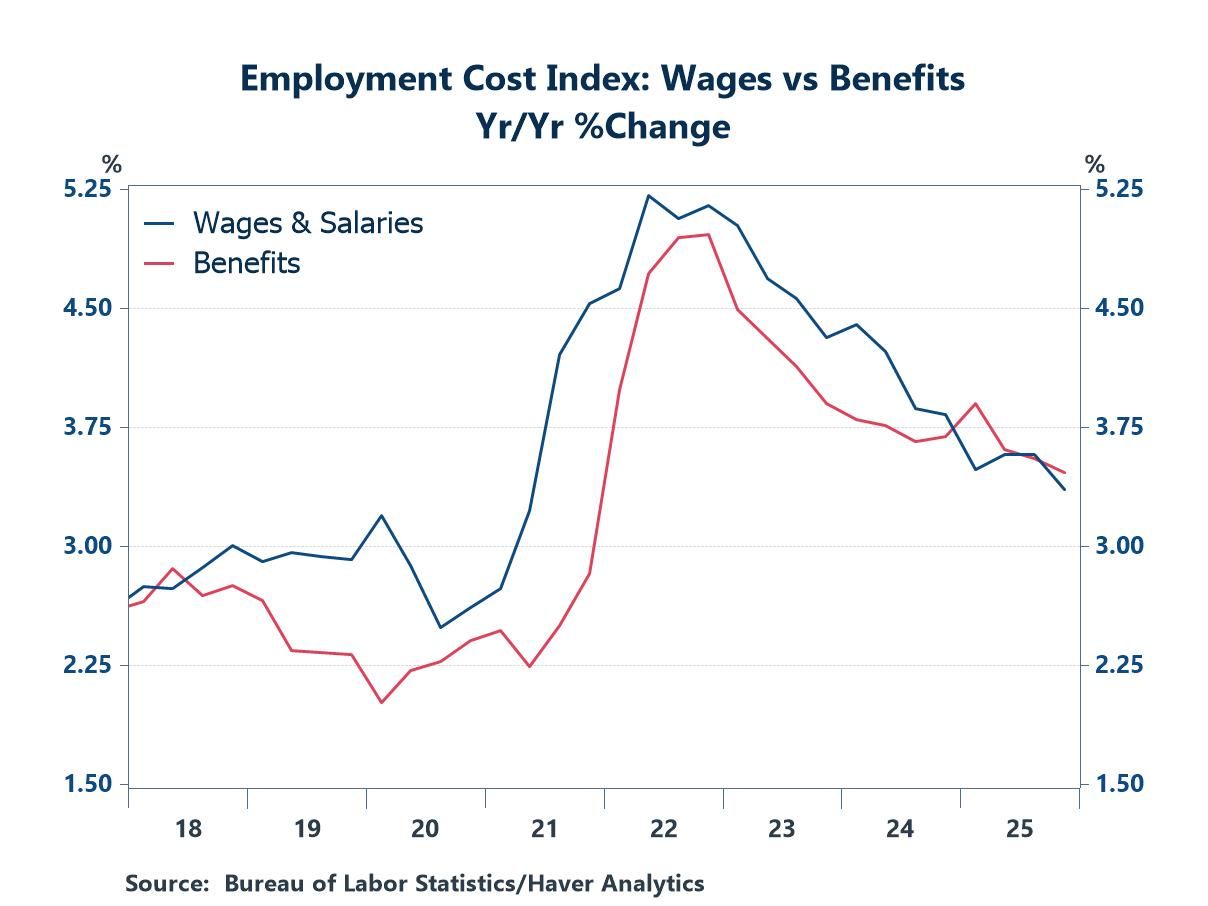

Total compensation in the ECI includes both wages and benefits. In the third quarter, both components rose by the same amount (0.7% quarter-to-quarter, or 3.0% at an annual rate). This balance is a shift from the pattern of recent years, when wages typically posted firmer growth. The advantage to wages in the past few years, in turn, represents a break from the more common tendency for benefits to grow at a faster pace.

The employment cost index measures the change in the cost of labor, free from the influence of employment shifts across occupations and industries. It is provided by the Bureau of Labor Statistics and is available in Haver’s USECON database. Consensus estimates from the Action Economics Forecast Survey are in Haver’s AS1REPNA database.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Global

Global