Asia| Jun 29 2026

Asia| Jun 29 2026Economic Letter from Asia: Oil Down, Emerging Risks

In this week's Letter, we explore the significant pullback in oil prices that followed the US-Iran memorandum of understanding and consider its broader economic implications. The agreement saw a fragile ceasefire ensue and a gradual resumption of shipping flows through the Strait of Hormuz (chart 1). We acknowledge that this major pullback will certainly be welcome to policymakers across the region and beyond. Previously elevated energy prices had added to the fiscal burdens of governments and sharpened the dilemma facing central banks (chart 2). That dilemma pits the need to rein in inflation against the risk of choking off economic growth. That said, while one source of inflationary pressure seems to be ebbing, another looks to be emerging on the horizon. It stems from a potential "Super El Niño" event, which meteorologists have been warning about for some time now. Asia sits at the centre of such risks, as past strong El Niño events have directly and adversely affected crop production (chart 3). The impact is not limited to potential surges in headline inflation via food supply shocks, especially in Asia. It extends directly to growth as well (chart 4), given the nontrivial share of GDP that agriculture still commands in many Asian economies (chart 5). Should price pressures simply rotate from energy to food, government subsidies may follow suit (chart 6). Central bankers, for their part, may find themselves unable to ease off the tightening pedal just yet. Some Asian economies, however, would still manage to offset such a growth shock through other engines. Electronics and semiconductors, buoyed by the current AI upcycle, offer one such cushion for the more fortunate. For others, lacking such offsets, the agricultural hit may simply have to be borne in full.

The US-Iran conflict and oil prices The recent memorandum of understanding between the US and Iran, aimed at working towards a final deal, has already brought visible relief to crude oil markets (chart 1). This relief has held despite the renewed tensions that have followed the agreement, which markets seem to have largely looked past. The easing in prices should go a long way towards unwinding the inflation concerns that elevated oil prices had previously stoked. Much of the pullback reflects anticipation of the substantial supply now expected to return to global markets. Yet some shipping trackers, such as the IMF's, already point to a marked pickup in traffic through the Strait of Hormuz. Even so, those volumes still remain well below the levels seen before the conflict began in the region.

Chart 1: Brent crude oil price and Strait of Hormuz shipping volume

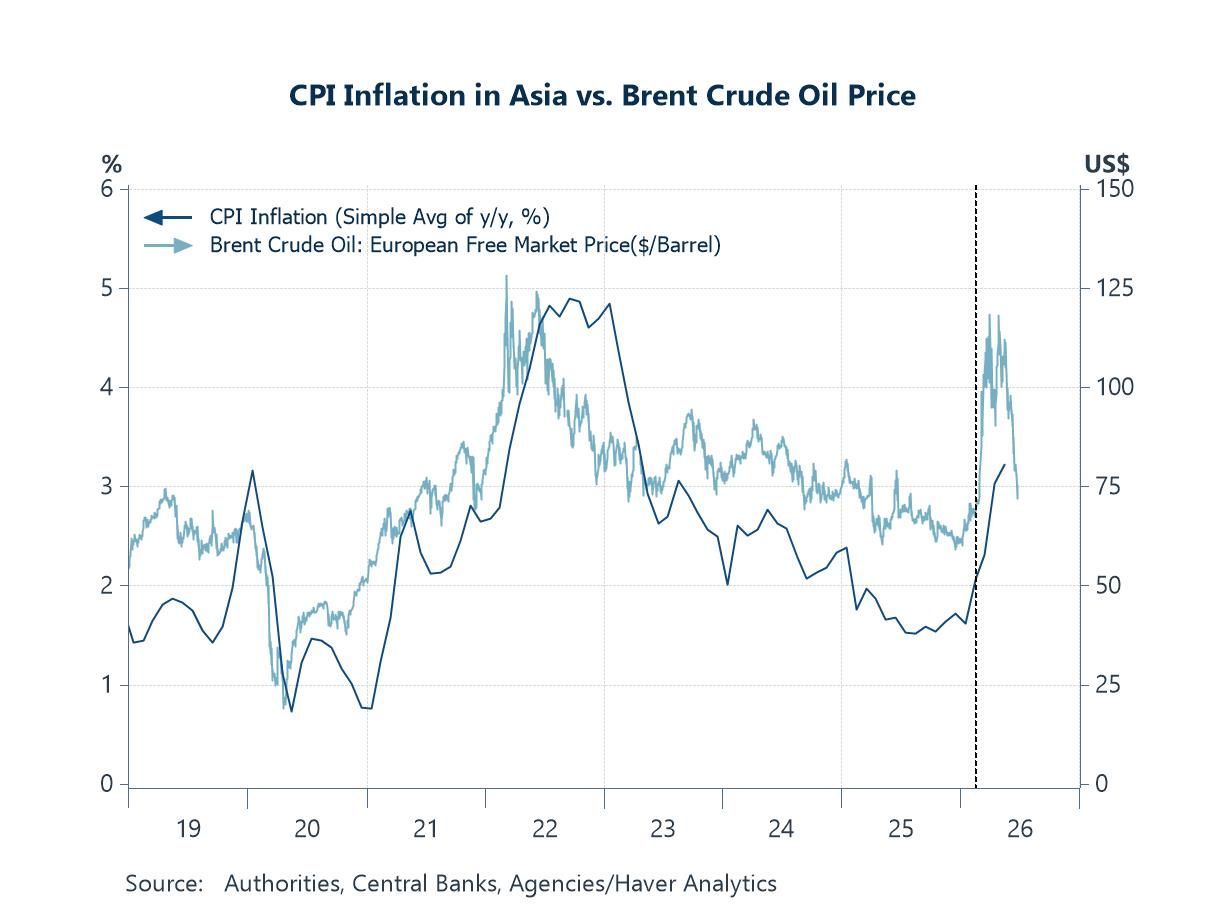

Oil prices and inflation in Asia Should this normalisation of shipping flows through the Strait of Hormuz persist, it would support a corresponding easing in oil prices and energy inflation. That moderation in energy costs would, in turn, help bring down broader headline inflation across the economy. As chart 2 shows, energy has been a large contributor to headline inflation in recent years, though other important forces have been at play too. Such an outcome, in which restored oil supply cools energy inflation, would be a welcome development for central bankers. They face the delicate task of reining in price pressures without tightening policy so far that growth stalls or tips into contraction. That said, while one driver of price pressures now seems to be ebbing, albeit not without the risk of renewed tensions, another source of inflation is building on the horizon.

Chart 2: Asia CPI inflation vs. Brent crude oil price

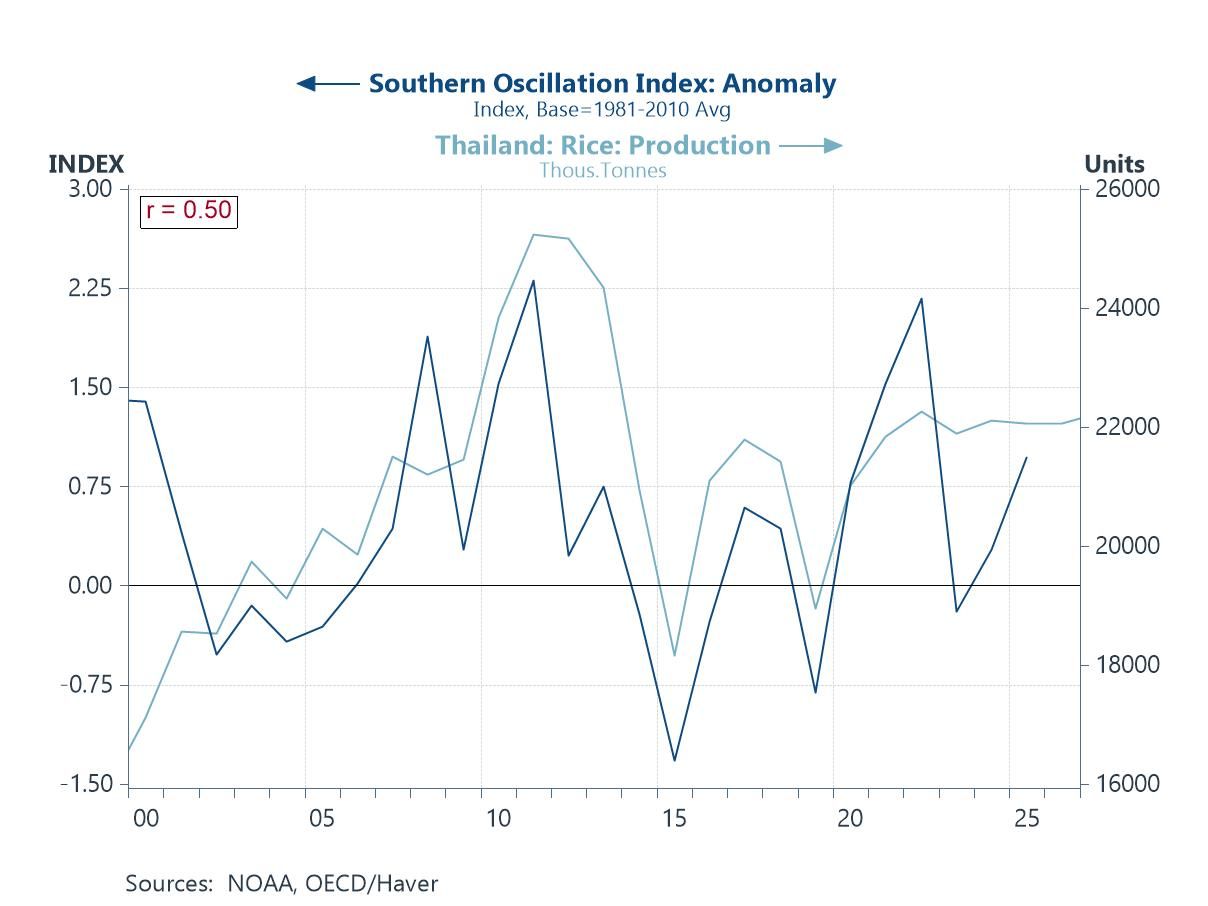

Risks of a “Super El Niño” As meteorological agencies have warned for some time, the world may be on the cusp of a Super El Niño. The probability of such an event has risen sharply in recent months. Were it to materialise, it would unleash a range of disruptions from the second half of this year, chief among them shifts in weather and climate patterns that can severely dent crop yields. Asian staples such as rice, wheat and palm oil are especially exposed, since strong El Niño events tend to bring drier conditions and reduced rainfall, in turn cutting output across affected economies in the region. Chart 3 illustrates just how tightly some crops are bound to these conditions: SOI readings correlate closely with certain economies' production, notably Thailand's rice harvest, underscoring how dependent such output remains on the weather. These supply shortfalls would then feed inflationary pressures through the food channel. So central bankers may not be able to rest entirely easy following the easing of tensions between the US and Iran, finding themselves wrestling with a fresh set of emerging inflation risks instead.

Chart 3: Southern Oscillation Index vs. Thailand rice production

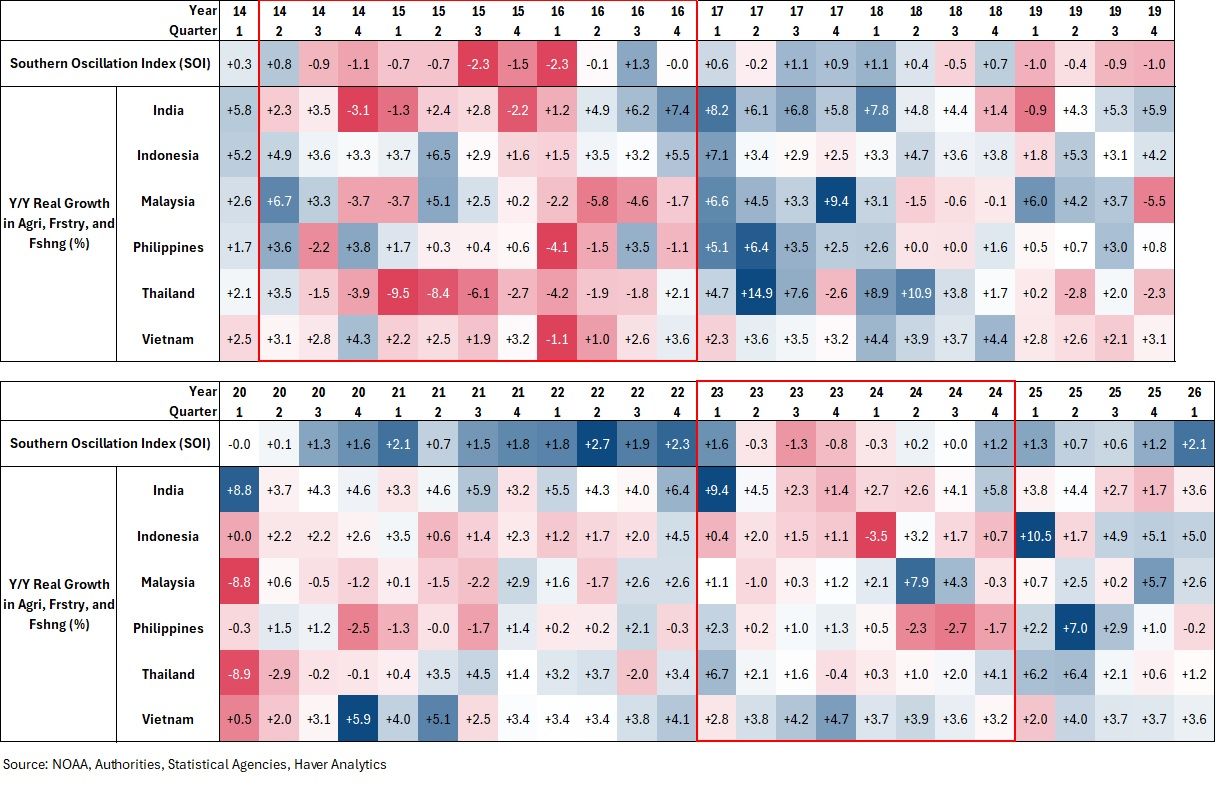

Delving deeper, an examination of recent strong El Niño episodes against the growth of Asian economies' agricultural sectors shows that extreme weather weighs not just on food prices but on economic growth itself. As chart 4 shows, previous major El Niño episodes—notably in 2014–16 and 2023–24—were associated with weaker agricultural growth across parts of Asia, with India and Thailand appearing particularly vulnerable. This is understandable, since these episodes coincided with reduced crop production and, in turn, lower crop revenue. Should these past episodes serve as a gauge and given that the coming event is potentially the worst on record, these economies stand to suffer once more should it hit as hard as feared.

Chart 4: Southern Oscillation Index and real agricultural sector growth in Asia

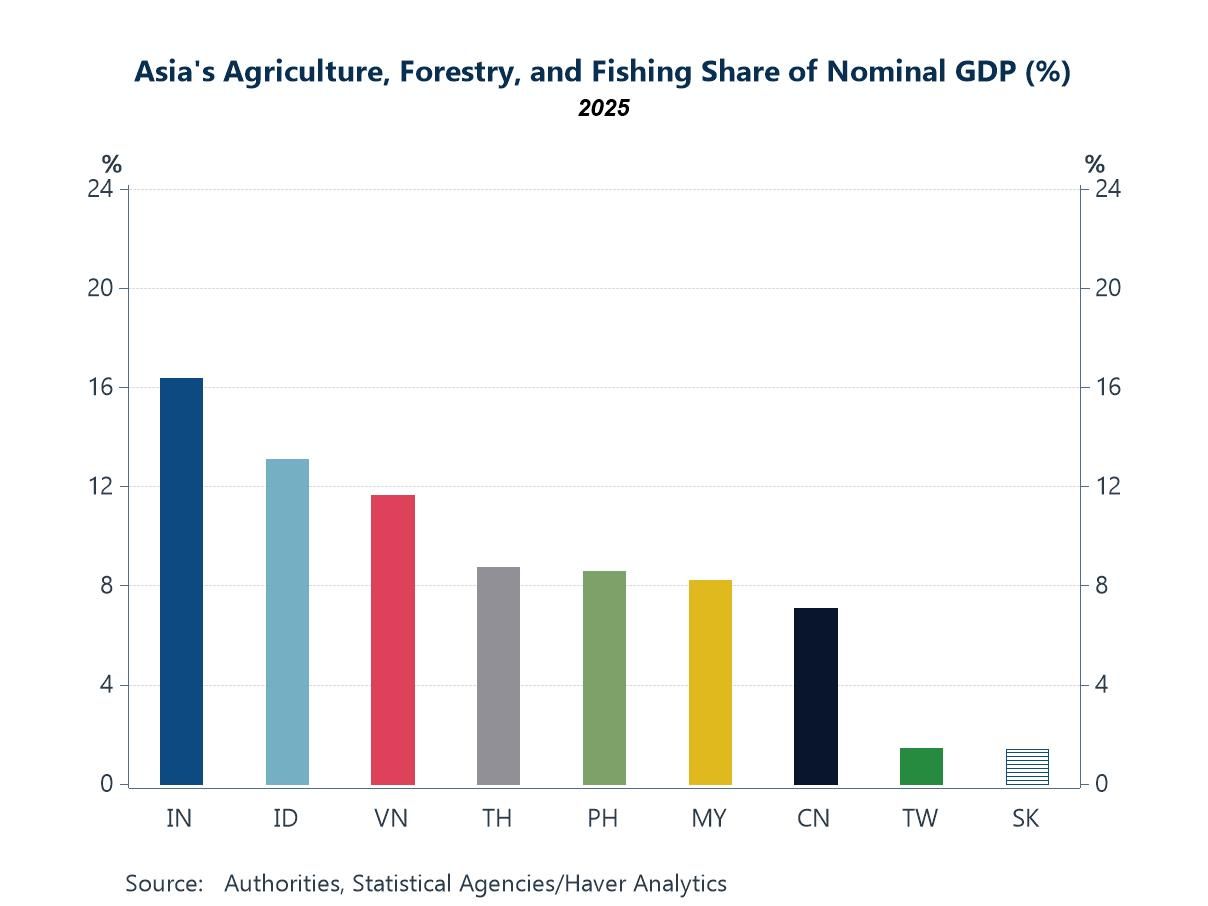

Beyond the sensitivity of individual economies to extreme El Niño events, vulnerability also depends on the size of the agricultural sector itself. Economies where agriculture accounts for a larger share of output are naturally more exposed to weather-related disruptions. As chart 5 shows, economies such as India, Indonesia and, to a lesser extent, Vietnam carry a comparatively higher share of agriculture in their GDP, which presents a further source of risk. That said, this dimension should not be read in isolation, since the eventual impact would turn on a combination of factors: the degree of exposure, the intensity of El Niño's effect on each economy's agricultural output, and the actual weather conditions that come to pass.

Chart 5: Asia’s agriculture share of nominal GDP

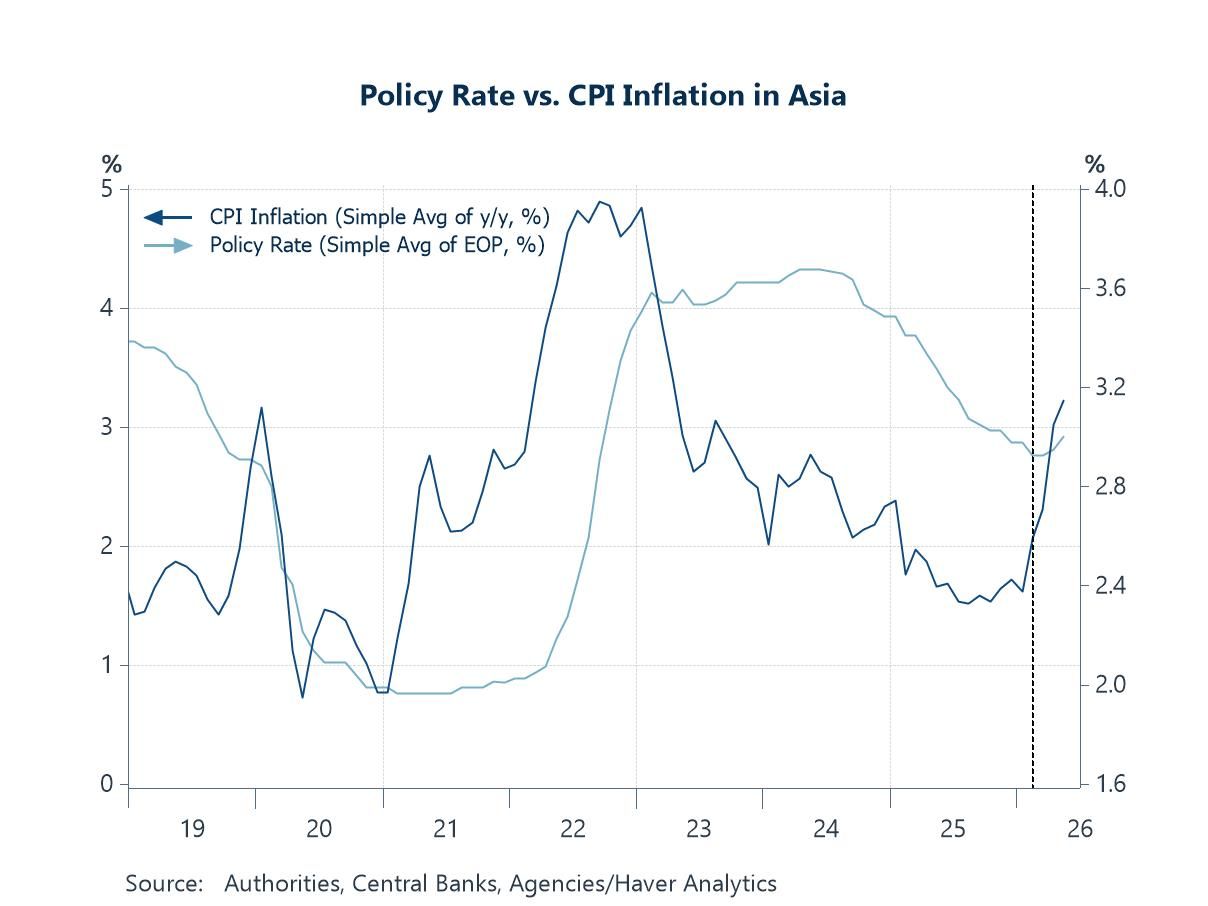

Bringing it all together, the recent de-escalation between the US and Iran and the early normalisation of flows through the Strait of Hormuz are certainly welcome news. Businesses, consumers and policymakers alike stand to benefit from the relief that lower energy prices would bring. Yet the formation of extreme El Niño conditions presents a looming inflation risk over the months ahead. It may displace energy as the dominant driver, shifting the pressure from the energy channel to the food channel. For Asia's central bankers, this could mean they are unable to ease off the tightening pedal just yet (chart 6). Food inflation may simply pick up where energy inflation leaves off, keeping price pressures elevated for longer. Regional governments, too, may have to redirect funds from energy subsidies to food subsidies should the supply shock play out. On growth, however, the picture may prove more uneven across the region than a single narrative suggests. Economies exposed to the current AI upcycle could keep leaning on those sectors for continued support. Those less exposed, by contrast, may simply have to absorb the hit to agriculture with little to offset it.

Chart 6: Asia average CPI inflation and policy rate

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief