Asia| Mar 30 2026

Asia| Mar 30 2026Economic Letter from Asia: Consumer Watch

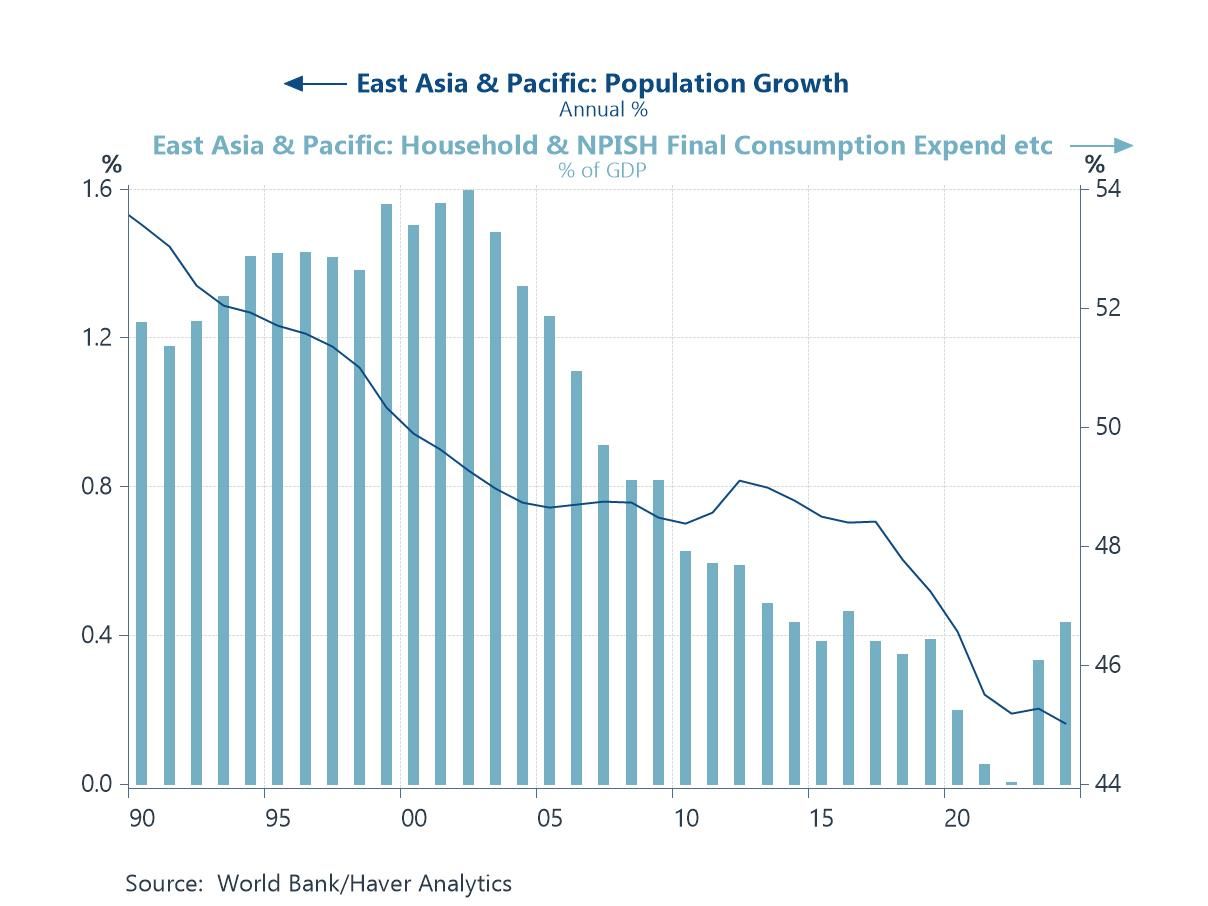

In this week’s Letter, we focus on the Asian consumer against the backdrop of recent global developments, alongside longer-running structural trends and economy-specific nuances. At a broad level, demographic headwinds are becoming more binding: as economies mature, population growth is slowing and ageing is accelerating, weighing on the expansion of the consumer base. At the same time, several economies are attempting to pivot toward more consumption-driven growth to help offset these forces (chart 1). More recently, while electoral outcomes in some countries have provided a boost to consumer sentiment, the renewed flare-up in the Middle East poses a near-term risk. Higher oil and energy prices threaten to squeeze household purchasing power, potentially weighing on sentiment and spending.

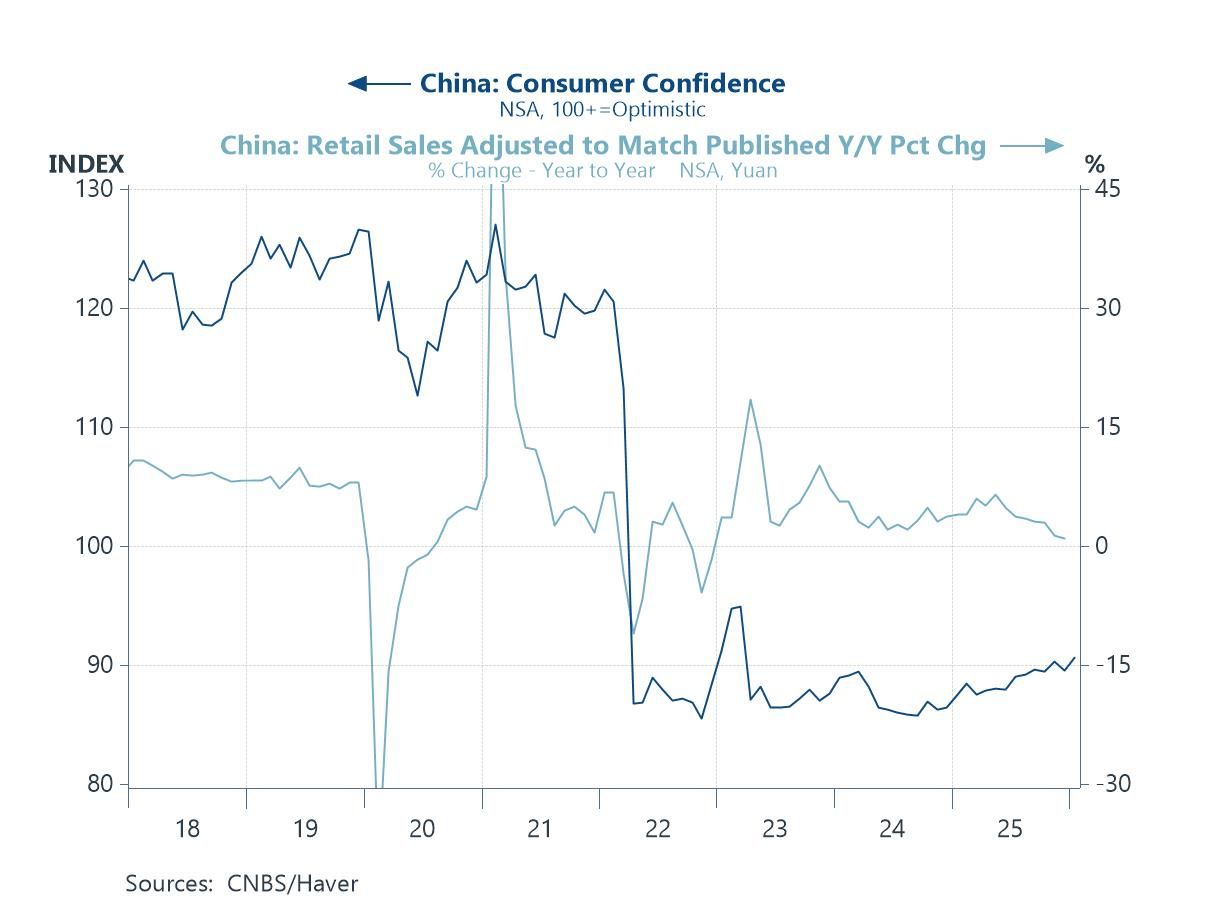

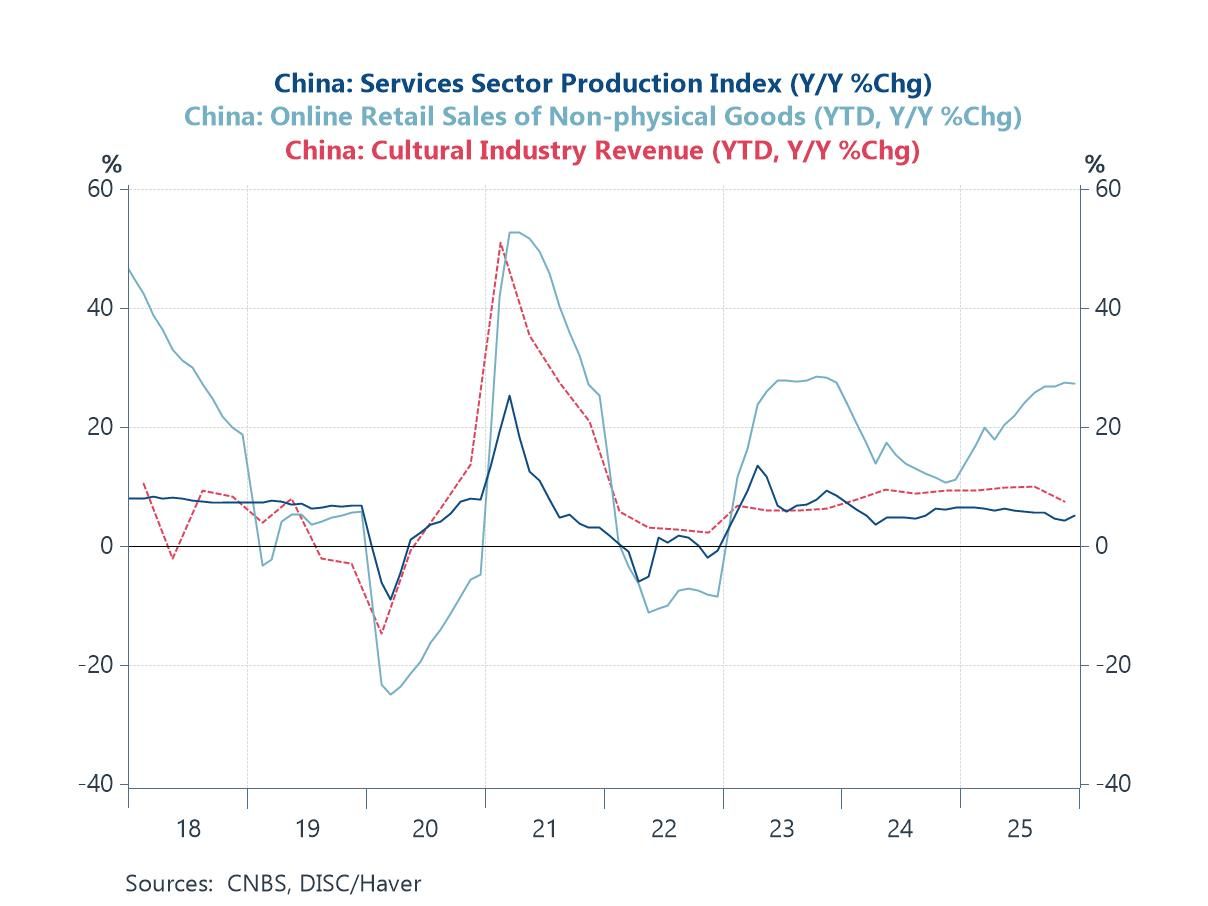

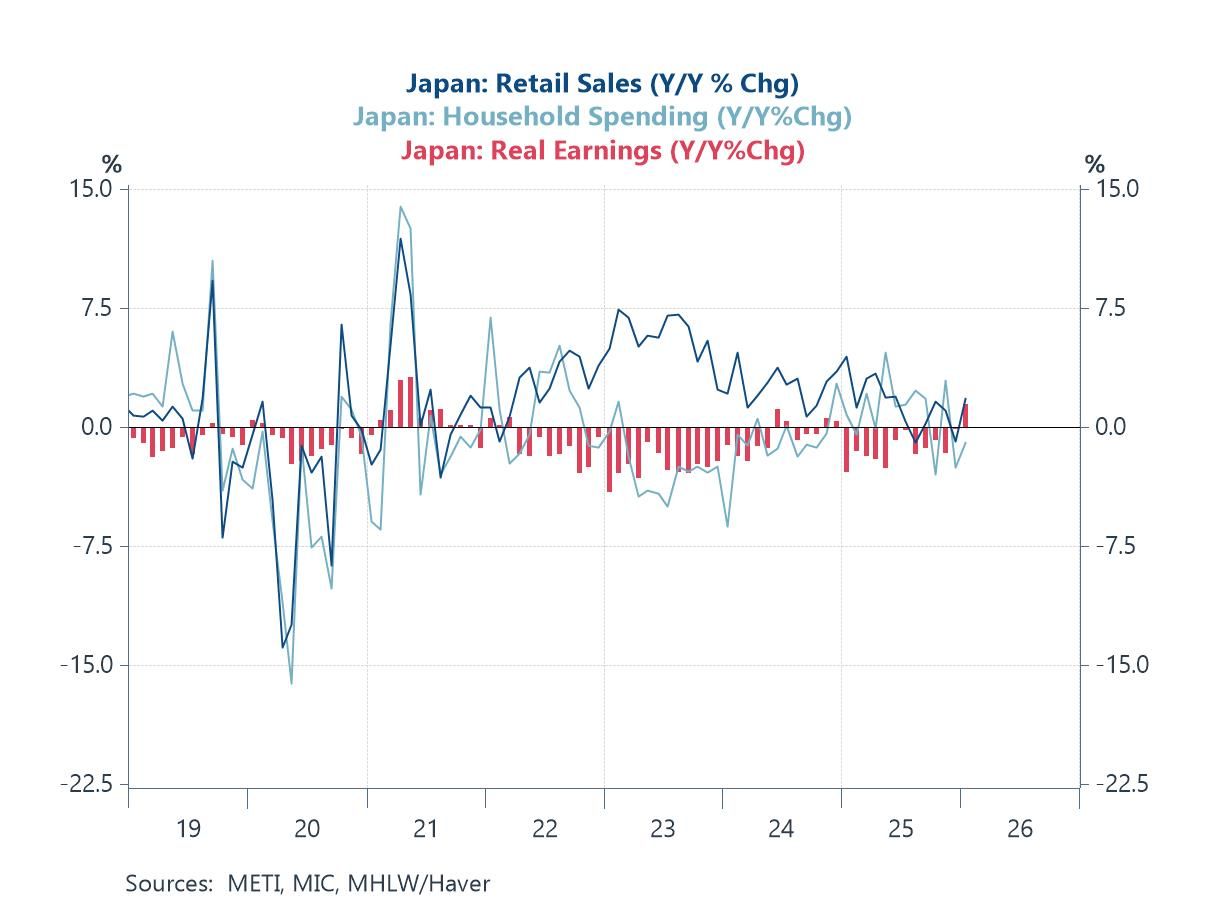

In China, policy efforts to raise the consumption share of GDP have delivered some early gains, reflected in firmer consumer sentiment and retail sales (chart 2). However, the impact of these measures may prove transitory if deeper structural constraints are not addressed. Encouragingly, authorities are increasingly looking to services as a new driver of consumption, given its relative underdevelopment compared to goods and manufacturing, and its potential for more sustained growth (chart 3). In Japan, post-election optimism surrounding Prime Minister Takaichi’s pro-growth agenda—including a proposed removal of the 8% consumption tax—has supported sentiment. However, rising oil prices risk reintroducing inflationary pressures, which could erode real wage gains and weigh on spending (chart 4).

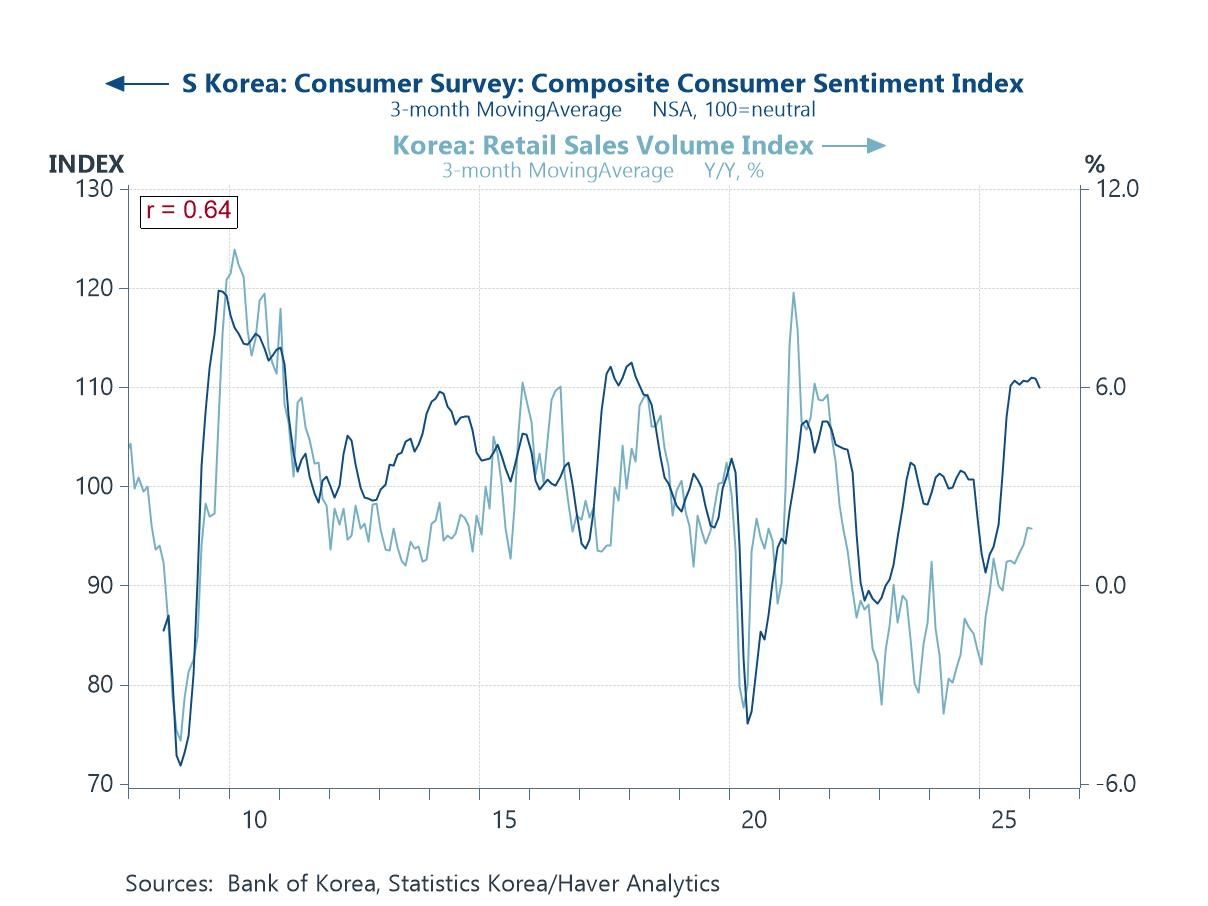

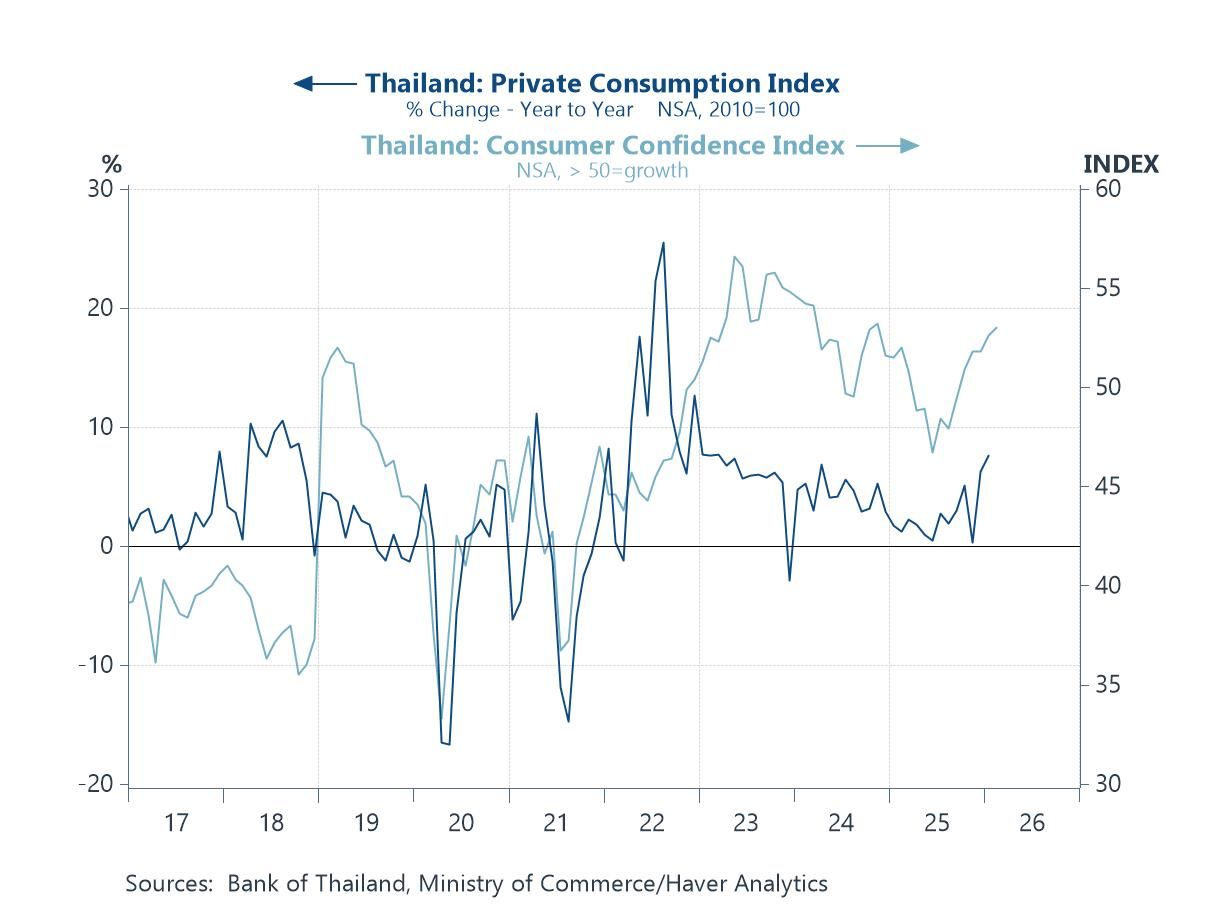

In South Korea, early signs of such pressures are already emerging (chart 5). Attention is also turning to consumer expectations, particularly around housing prices following recent cooling measures, as well as inflation expectations—especially if they begin to show signs of becoming unanchored. In Thailand, post-election optimism has similarly supported sentiment and consumption (chart 6). Nonetheless, headwinds persist, notably elevated household debt and higher oil prices. While the agreement between Thailand and Iran to allow vessels to transit the Strait of Hormuz is a positive development, it remains uncertain how much relief it will ultimately provide.

The Asian consumer Asia is at a crossroads. On the one hand, as is typical for maturing economies, the region is confronting slowing population growth and rapid ageing. This implies a more slowly expanding—and in some cases shrinking—consumer base, as already evident in economies such as China and Japan. At the same time, consumption patterns are shifting toward goods and services tied to ageing and retirement, as older cohorts account for a larger share of demand. On the other hand, Asia’s household consumption share of GDP has edged higher in recent years. Much of the remaining upside—relative to global averages—is concentrated in a handful of economies, most notably China, which we discuss later. A more decisive rebalancing toward consumption could unlock additional spending power across the region, partly offsetting demographic headwinds, though the net impact remains uncertain.

Chart 1: Asia population growth and household consumption share of GDP

China Based on nominal values, China’s residential consumption share of GDP has trended higher in recent years, reaching just under 40% in 2024. However, this remains well below levels seen in most other economies, particularly developed ones. As such, China still has some distance to go in pivoting away from its traditional reliance on exports and investment toward a more consumption-led growth model. To support this shift, authorities have rolled out a range of measures to boost consumption, including subsidies for consumer durable goods trade-ins. However, given the nature of durables, such policies tend to front-load demand, raising questions about the sustainability of any initial consumption boost once replacement cycles are largely exhausted. Indeed, while retail consumption has posted decent growth in recent years, the pace has been gradually moderating, suggesting some loss of momentum.

Chart 2: China consumer confidence and retail sales

At the same time, policymakers are increasingly focusing on services as a potential next driver of consumption growth. This shift is intuitive, given that the services sector remains relatively underdeveloped compared to the goods sector, where years of manufacturing expansion have led to substantial capacity and, in some areas, oversupply. In response, authorities have extended tax incentives and subsidies to selected service industries to stimulate demand. That said, beyond targeted incentives, a more durable rebalancing toward consumption will likely require deeper structural reforms. Economists have long pointed to the need for stronger social safety nets, improvements in healthcare and pension systems, and sustained wage growth to reduce precautionary savings and support household spending. In addition, addressing the prolonged weakness in the property sector could provide a meaningful boost to consumption via wealth effects.

Chart 3: China’s services and cultural sectors

Japan Turning to Japan, chart 4 suggests the consumer backdrop remains mixed. Growth in retail sales and household spending has struggled to stay consistently in positive territory, while real wage growth has been negative for much of recent years—albeit with a return to positive territory in January. That said, expectations are building around Prime Minister Takaichi’s pro-growth agenda to support consumption, including proposals such as eliminating Japan’s 8% consumption tax. However, questions remain over both the effectiveness of such measures and their fiscal implications More recently, external factors have also come into play. In particular, the inflationary impact of the ongoing Middle East conflict—via higher oil prices—poses a renewed risk. While this year’s Shunto spring wage negotiations have delivered strong nominal wage gains, sustained price pressures could erode real incomes, potentially reversing recent gains. This, in turn, may also prompt further monetary policy tightening, adding another headwind to consumption.

Chart 4: Japan retail sales, household spending, and real earnings

South Korea Turning to South Korea, retail sales volumes have shown some encouraging growth in recent months. However, as with many Asian economies—particularly oil importers—this momentum risks being undermined by the recent surge in energy prices following the Middle East conflict. Early signs of a softening consumer outlook are already evident. South Korea’s latest consumer survey readings have fallen to a 10-month low, pointing to a deterioration in sentiment. A closer look suggests that domestic factors are also at play. Notably, expectations for housing prices have weakened following recent policy measures aimed at curbing property prices and household debt. At the same time, inflation expectations have edged higher, albeit modestly. Should these expectations become unanchored and rise more sharply, this could increase the likelihood of further monetary policy tightening—adding another potential headwind to consumption.

Chart 5: South Korea consumer sentiment and retail sales volume

Thailand Lastly, we turn to Thailand, where the consumer backdrop has improved in recent months (chart 6), with both sentiment and growth in the central bank’s private consumption measure picking up. This likely reflects, in part, post-election optimism following Prime Minister Anutin’s victory, alongside expectations of supportive stimulus measures and a reduction in prior political uncertainty. That said, headwinds remain. Thai households continue to face elevated, though not identical, indebtedness challenges relative to peers such as South Korea, with household debt-to-disposable income still just above 150% as of Q3 2025. While such levels have been sustained for some time, risks may crystallise further out if households become less able to service their debt burden. More recently, external pressures have also re-emerged via the Middle East conflict and higher oil prices. Although Thailand and Iran have reportedly reached an agreement allowing oil vessels to transit the Strait of Hormuz—an encouraging development—price risks persist amid broader supply constraints that continue to keep energy markets tight.

Chart 6: Thailand private consumption and consumer confidence

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief