Manufacturing IP in EMU Slogs Ahead

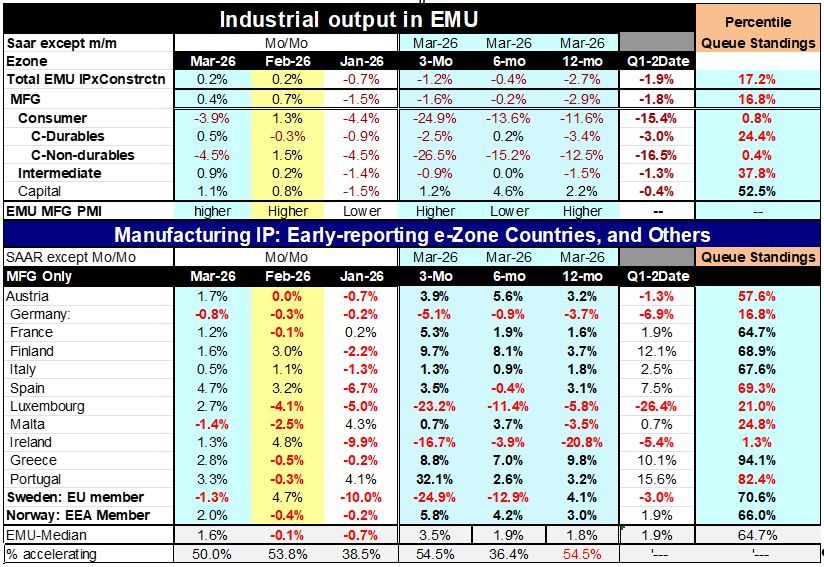

Industrial production in the European monetary area in March rose by 0.2%. Manufacturing output rose by 0.4%, marking two-months in a row of output increases. Output is still falling overall and in manufacturing over three months. Over three-months total manufacturing output excluding construction falls 2.7% annualized, over 6-months, it falls at a 0.4% annual rate, and over three-months the pace of decline steps back up again to -1.2% at an annual rate. The declines in manufacturing are more or less along the same lines.

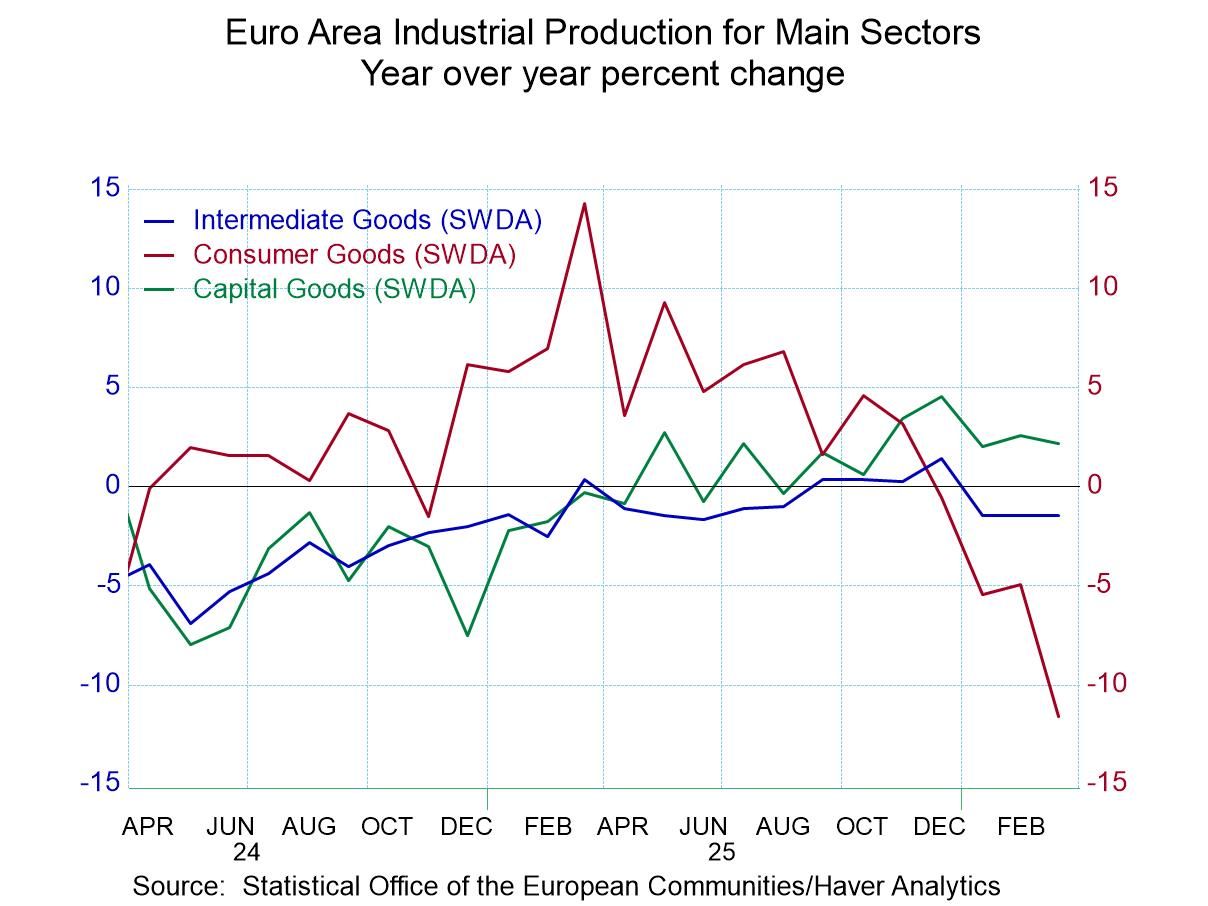

Sectors Output of consumer goods fell in March, driven by a decline in the output of nondurable goods that fell 4.5% month-to-month. Intermediate goods output rose by 0.9% in the month, increasing for the second month in a row. Capital goods output rose 1.1% after rising 0.8% in February.

Sequential growth However sequential growth rates find headline growth negative over 12-months, six-months, and three-months- the same as for manufacturing. Consumer goods output declines at an accelerating pace dropping 11.6% over 12-months, at a 13.6% annual rate over six-months and at a 24.9% annual-rate over three-months. Those declines are led by reduction in consumer nondurables output. Intermediate goods output is mostly weak over the horizon, falling by 1.5% over 12-months and by 0.9% over 3 months annualized. The exception is capital goods sector where output rises by 2.2% over 12 months and accelerates to 4.6% over 6-months but then tails back, trimming growth to a 1.2% annual rate over three-months.

Country Performance On a country basis declines occur in only two early-reporting members; those are Malta and Germany in March. Over three months output declines in the monetary area occurs in Ireland and Luxembourg and in Germany- with increases elsewhere. Output declines over 12-months, six-months, and three-months in the monetary area only for Germany, Luxembourg, and Ireland. There are consistent output increases in the monetary union in Austria, France, Finland, Italy, Greece, and Portugal. For most countries, increasing output is the rule despite the weak headlines, indicating that large economies are faring worse than smaller economies.

Q1 Growth In the completed first quarter, we have manufacturing output falling by 1.8% at an annual rate and overall output falling at a 1.9% annual rate. Output declines in the quarter and in all major sectors. As for country reporters output falls in the quarter for Austria, Germany, Luxembourg, and Ireland.

Growth rate rankings So, the percentile queue standings presented in the right-hand column are rankings of industrial production growth rates over 12-months. Compared to recent history, overall output has a 17-percentile standing which is relatively weak, in the lower one-fifth of its ranked results over the period (back to 2006). Only capital goods output at 52.5% has a standing above the 50% level which places it above its median result for the period. Among reporting countries seven have percentile standings above 50%, above their respective medians. The countries where output does not grow at a pace in excess of its median are Germany, Luxembourg, Malta, and Ireland.

On balance the smaller countries seem to be faring better in the European monetary union. The last two months have been relatively good months for output across the union; however, January had been so weak that the two months have not been able to recover from the weakness experienced in January. And the March data hardly reflect the hardships that are going to be visiting these economies because of the rise in oil prices and concerns about the situation in Iran and the strait of Hormuz. The future is unlikely to get better.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global