Asia| Feb 23 2026

Asia| Feb 23 2026Economic Letter from Asia: Asia and AI

In our Letter this week, we delve deeper into AI, with a focus on Asia and, where relevant, comparisons with the US. The global economy remains firmly in the buildout phase of AI, where much of the near-term economic benefit is derived from investment in hardware and enabling infrastructure—such as AI chips, memory, and data centres. At the same time, though still at a relatively early stage, firms are beginning to adopt advanced AI capabilities and integrate them into workflows in pursuit of productivity gains. So far, labour productivity improvements have been evident in parts of Asia (chart 1), largely driven by stronger exports (chart 2) and capital deepening—similar to trends observed in the US (chart 3) and, within Asia, in economies such as Malaysia (chart 4). However, these gains have yet to translate into a clear and sustained acceleration in total factor productivity (TFP), which accounts for the combined use of labour, capital, and other inputs—though TFP is admittedly a challenging metric to estimate, as illustrated by the US case (chart 5). This raises an important question: what happens when the AI buildout phase begins to moderate, and the associated investment-led tailwinds fade? At that point, further AI-related gains will depend more heavily on the successful embedding and diffusion of AI across sectors. On this front, Asian economies remain at very different stages of readiness to adopt AI (chart 6), suggesting that the next phase of productivity gains may be uneven across the region.

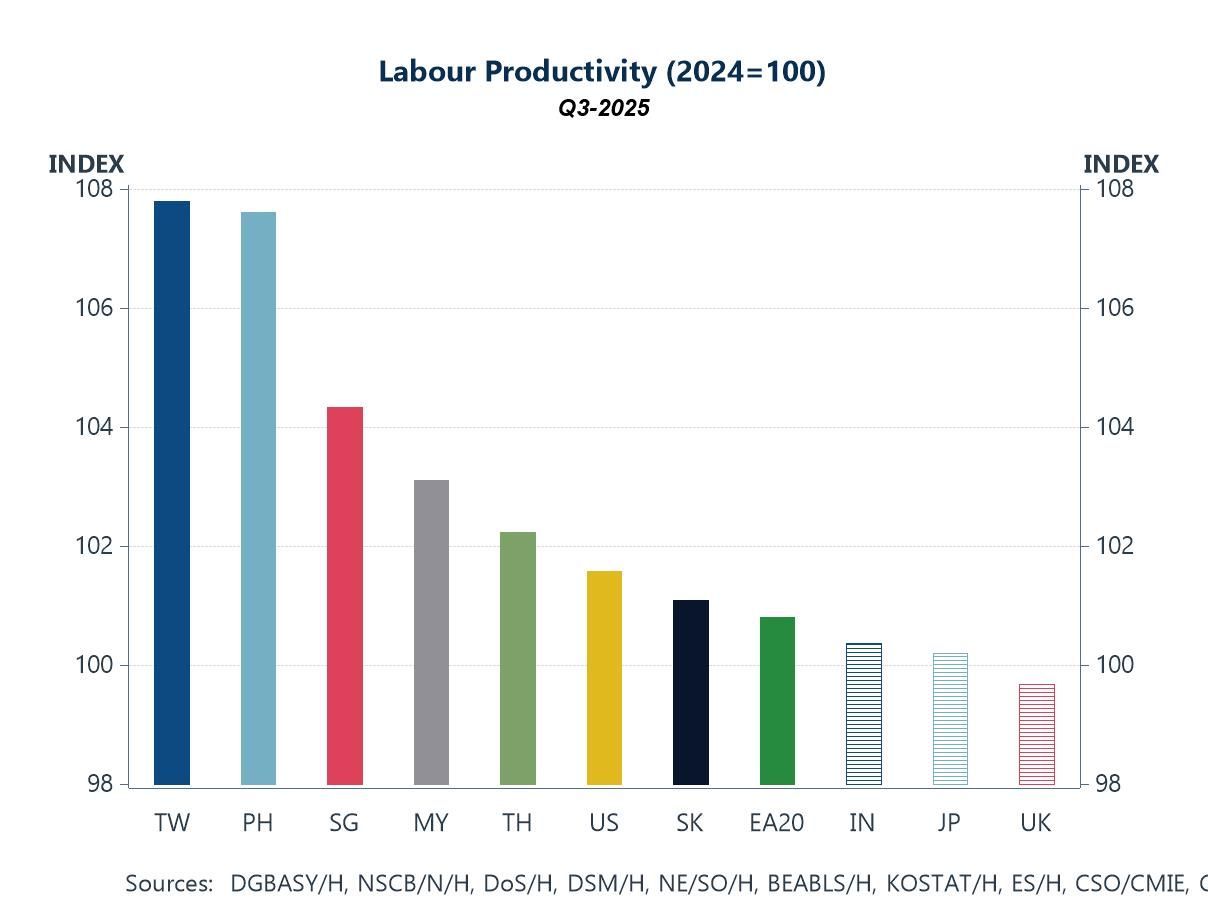

The productivity story Several Asian economies have already recorded substantial productivity gains in recent years, even before the narrative around AI-driven productivity boosts gained traction last year. As shown in chart 1, measured by labour productivity—simply defined as output per employed person—economies such as Taiwan and several in Southeast Asia stand out for their strong performance. However, these gains cannot be attributed solely to the promise of AI. By definition, labour productivity rises whenever output (the numerator) grows faster than employment (the denominator). Such an outcome can stem from a range of factors—cyclical recoveries, capital deepening, sectoral shifts, or efficiency improvements—and does not necessarily reflect widespread AI adoption.

Chart 1: Labour productivity

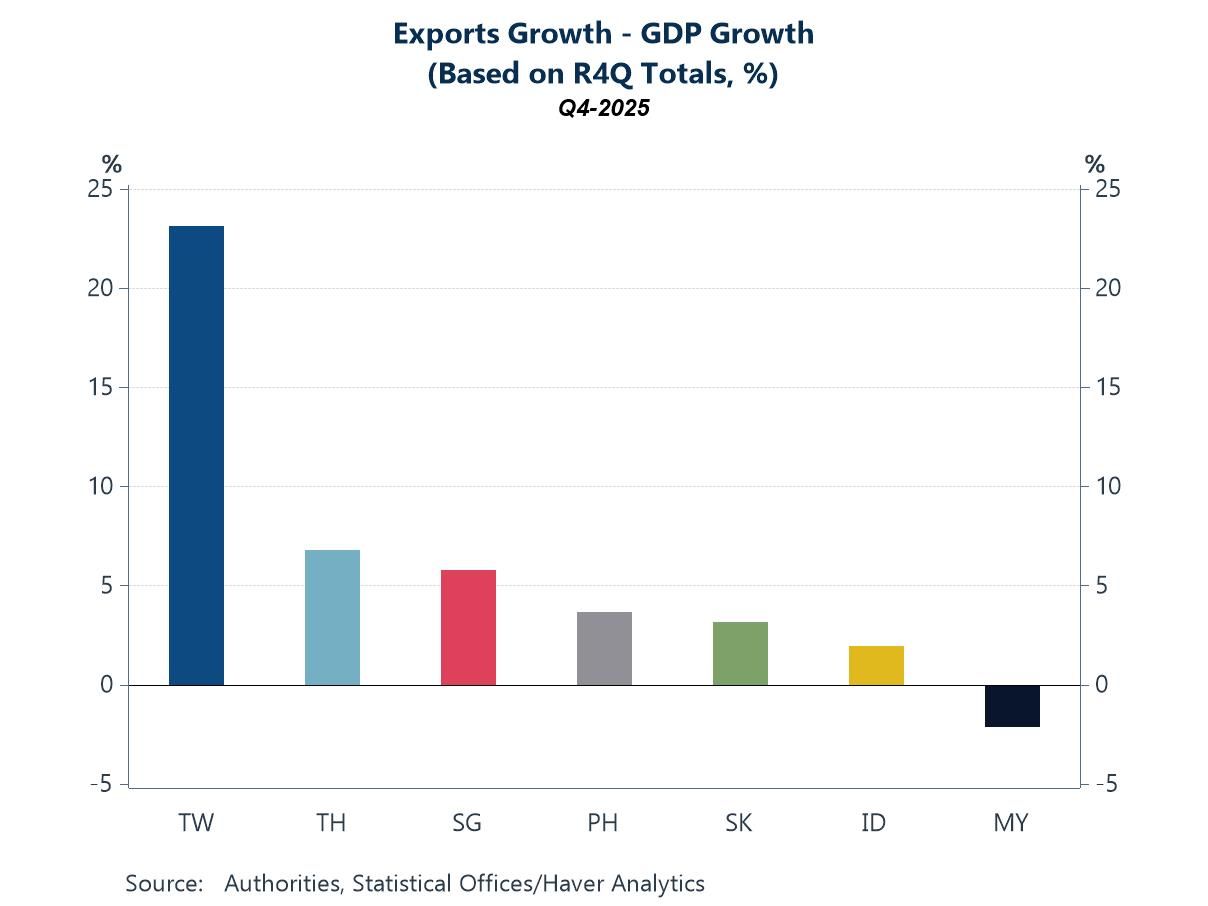

Digging deeper, however, it would be equally misleading to suggest that Asian economies have not benefited from AI-related productivity gains. As shown in chart 2, exports have been a key driver of growth across several economies in recent years. In particular, Taiwan and South Korea—both major producers of AI-related hardware—have benefited from strong global demand for advanced chips and memory used in AI infrastructure. Taiwan stands out: its Q4 real GDP growth surged to 12.7% y/y, with net exports accounting for nearly all of that expansion. Notably, integrated circuits—often comprising around a third of total exports—have played a central role in this performance. Thus, while many Asian economies may not yet be at the forefront of deploying cutting-edge AI models domestically, they are significant beneficiaries of the current AI infrastructure buildout. By supplying the semiconductors and components underpinning this expansion, parts of the region are already capturing meaningful gains from the AI cycle.

Chart 2: Asian economies’ spread between exports and GDP growth

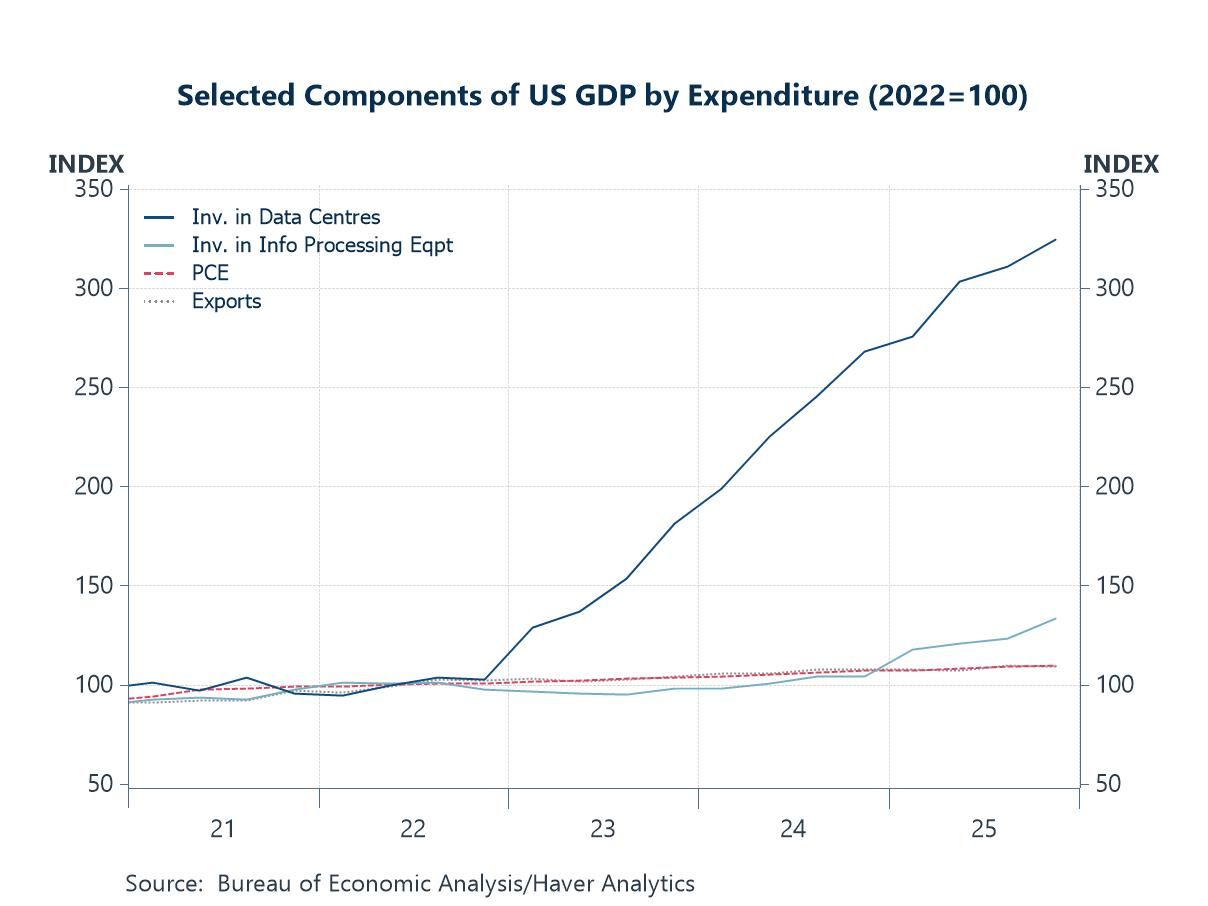

Capital deepening Another key channel through which labour productivity can be achieved—aside from reducing the denominator (employment)—is capital deepening, or an increase in capital per worker. On this front, some advanced economies, including the US, have already moved in this direction as firms ramp up investment in AI-related infrastructure and equipment. In recent years, growth in investment in information processing equipment and data centres has outpaced other demand components, such as consumption and exports, reflecting in part the ongoing AI-related buildout (chart 3).

Chart 3: Components of US GDP by expenditure

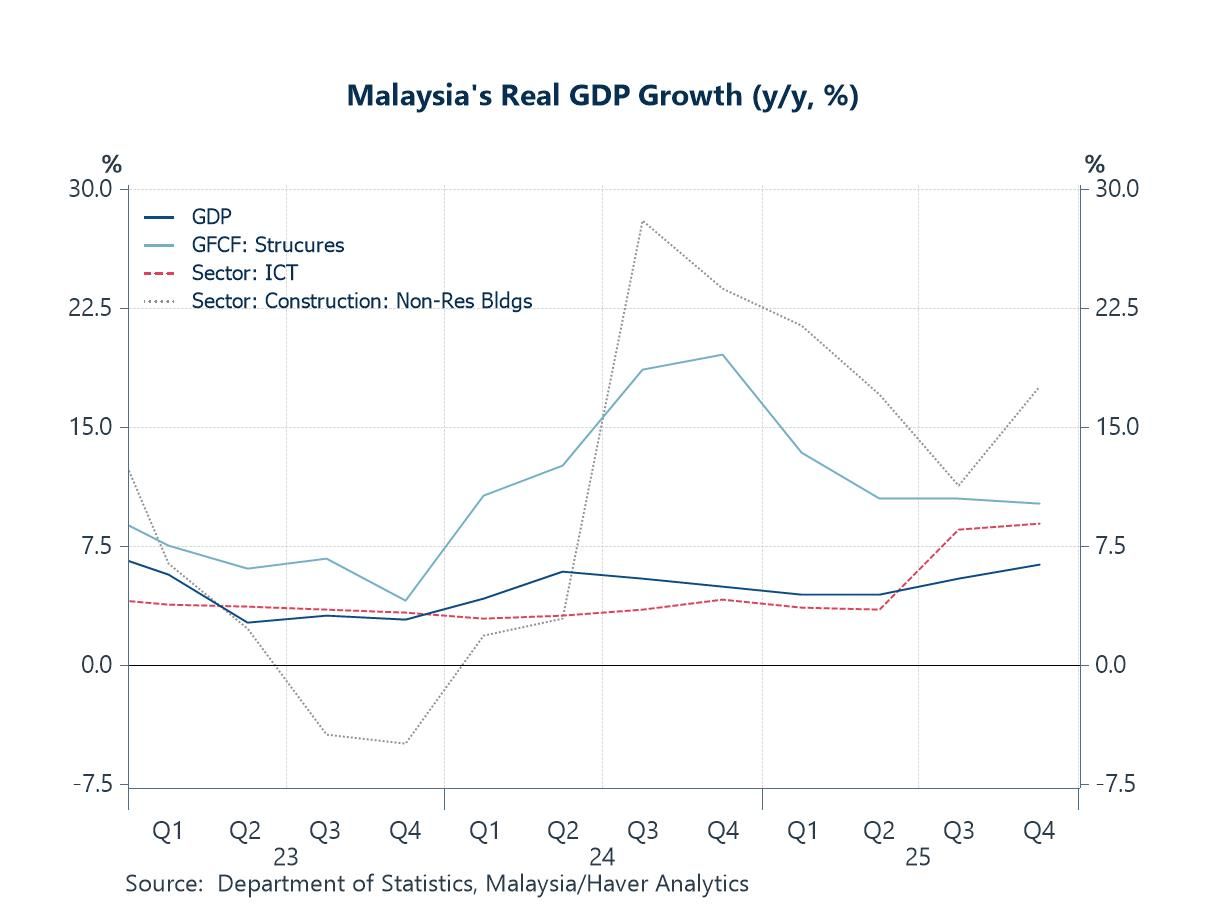

The growth-enhancing—and by extension productivity-supporting—effects of such AI-related capital deepening are also evident in parts of Asia. In Malaysia, for example, the rapid expansion of its data centre industry has spurred strong gains in investment and construction activity, alongside spillovers to related sectors (chart 4). Importantly, these AI-related, investment-led gains are not limited to data centre development. Capital outlays to expand production capacity for AI-related goods—such as semiconductor fabrication and advanced chip manufacturing—operate through the same channel, increasing the capital stock and, over time, lifting output per worker.

Chart 4: Malaysia’s real GDP growth

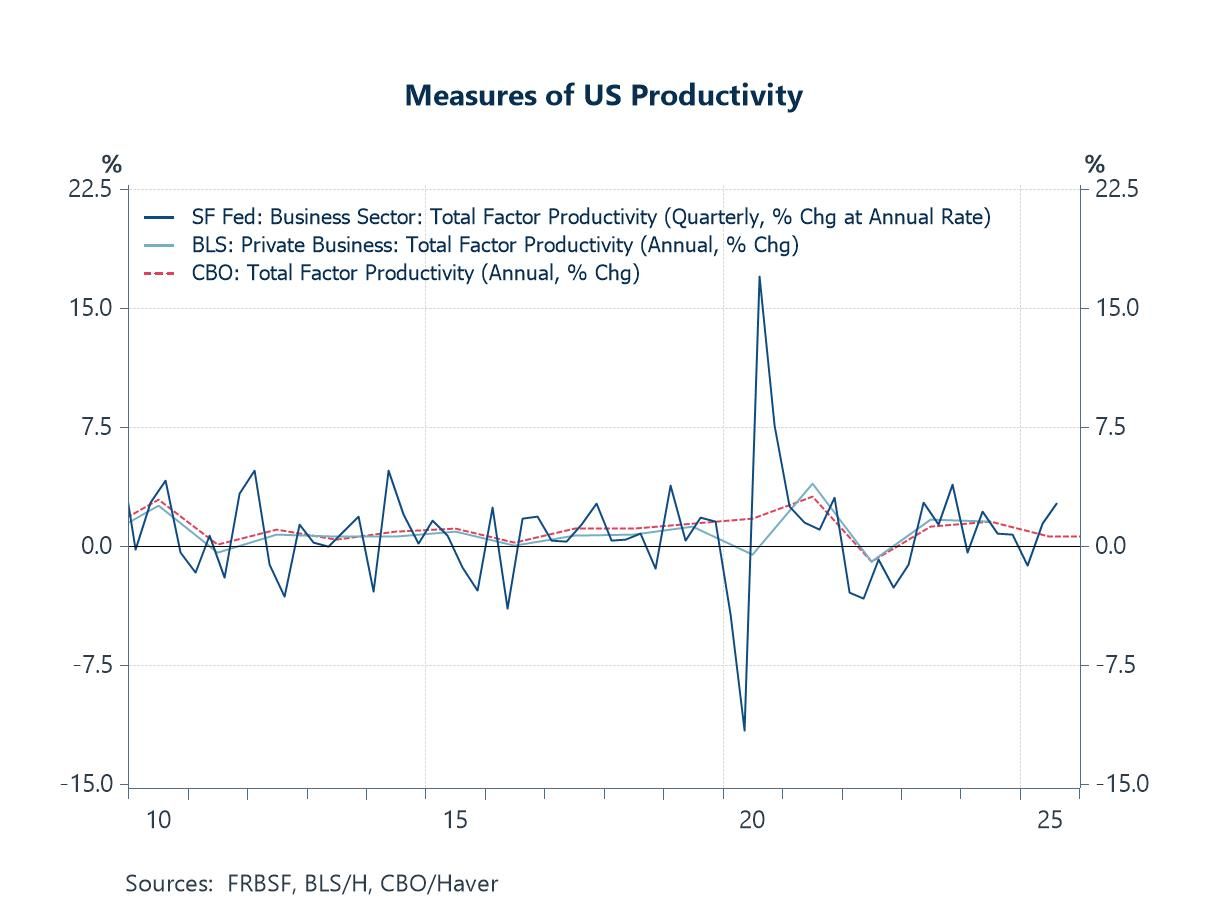

Beyond the AI buildout So far, the discussion has centred on productivity in terms of labour productivity—output per employed person. That metric can be lifted relatively easily by increasing the numerator, whether through stronger exports or higher investment, as outlined in the previous sections. But what about gains in total factor productivity (TFP), rather than just labour productivity? TFP takes into account inputs beyond labour, including capital and other factors. An increase in TFP therefore implies higher output generated from the same combination of labour, capital, and other inputs. It is arguably this type of efficiency gain that investors hope will materialise from the adoption of AI. That said, TFP is notoriously difficult to measure. In the US, for instance (see chart 5), estimates of TFP growth can vary depending on the data source and methodology used. Even so, higher-frequency measures of US TFP have yet to show an outsized acceleration, suggesting that AI-related optimism has not—at least for now—translated into a discernible surge in measured productivity.

Chart 5: Measures of US Total Factor Productivity

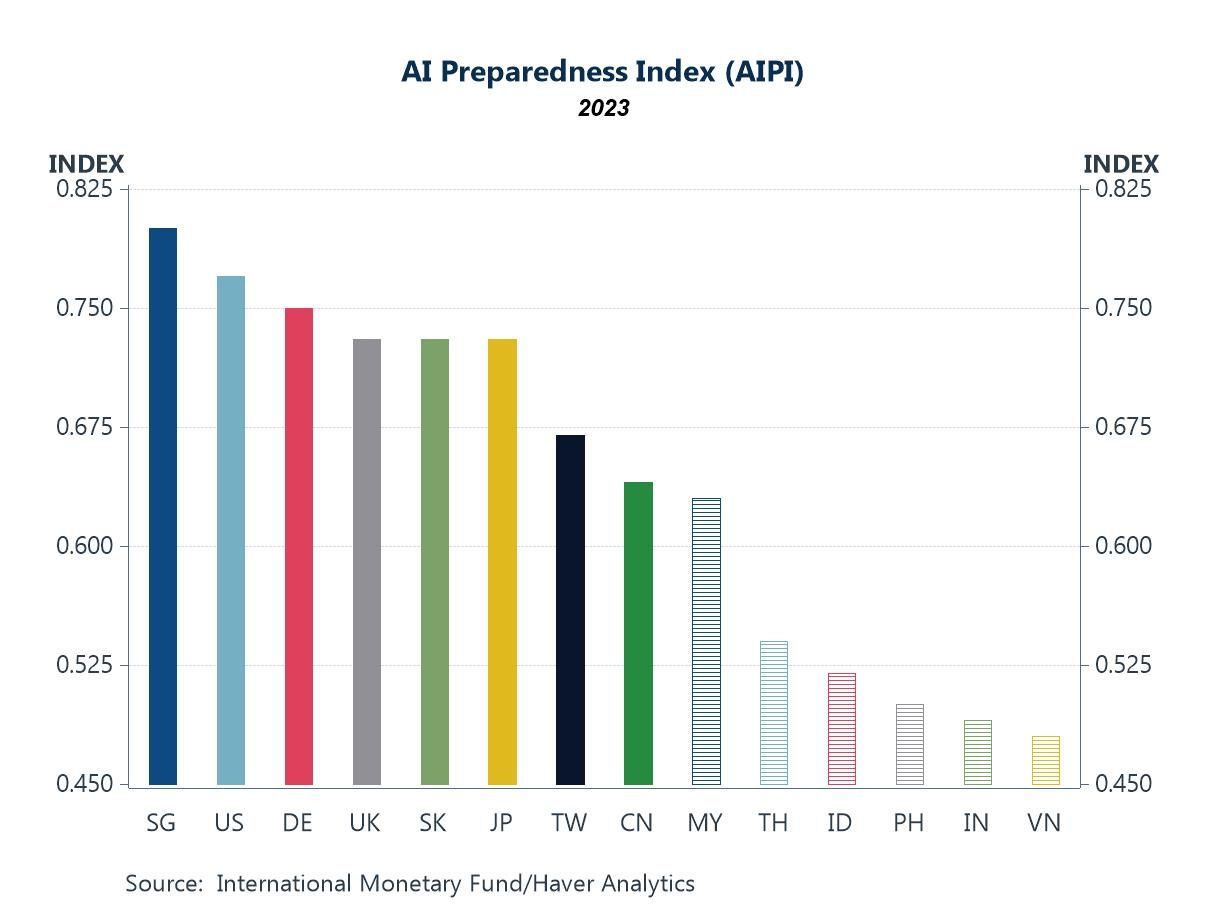

Another key dimension to monitor is how prepared Asian economies are to embrace AI and embed it effectively in order to capture its anticipated productivity gains. While many economies in the region are currently benefiting from labour productivity gains—driven by stronger manufacturing activity and exports of AI-related goods and infrastructure—such gains may eventually moderate, particularly once the initial buildout phase peaks. At that stage, the more durable benefits will need to come from a different channel: the total factor productivity gains associated with the actual adoption and diffusion of AI across industries. On this front, Asian economies differ markedly in their readiness. As shown in chart 6, an IMF index—incorporating factors such as digital infrastructure, innovation capacity, human capital, and regulatory frameworks—highlights this divergence. More advanced economies, including Singapore, South Korea, and Japan, rank highly, while others such as Vietnam, India, and the Philippines lag behind. That said, the concerted efforts by several developing Asian governments in recent years to strengthen digital infrastructure, upgrade skills, and refine regulatory frameworks suggest that this gap could narrow over time.

Chart 6: AI preparedness index

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief