Big Four Inflation in EMU 2025-Final

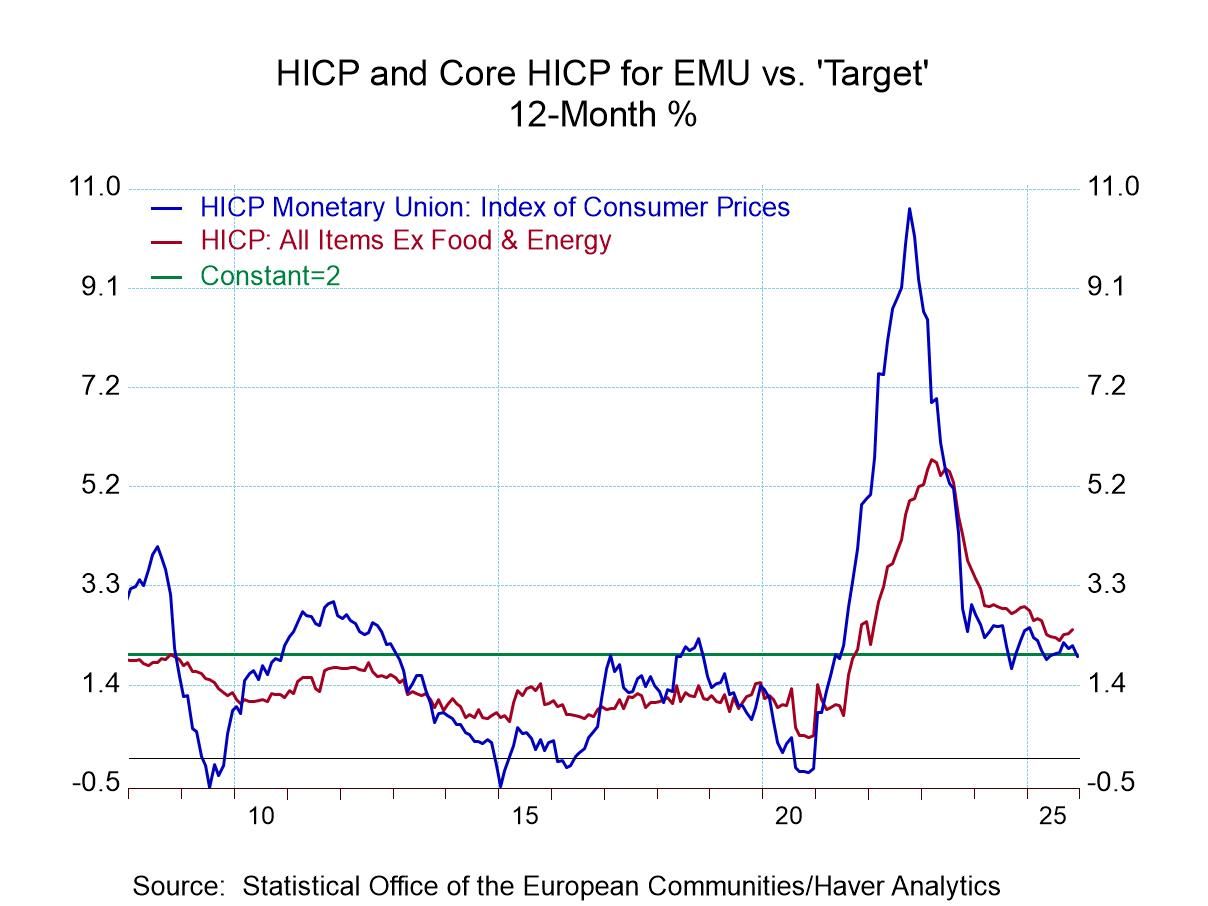

The European Monetary Union has concluded a year of weak-to-moderate growth with inflation largely toeing the line. As always, the inflation picture is more complicated than a simple statement. When we look at inflation, we look at the headline, we look at the core, to make sure that the volatile food & energy elements aren't dominating the index, and then we look across some of the main participants to see if the trend for inflation is shared broadly across the largest countries in the Monetary Union. When we apply those kinds of standards, the grading for the year is reduced. However, based on the headline alone, it was an excellent year for the ECB.

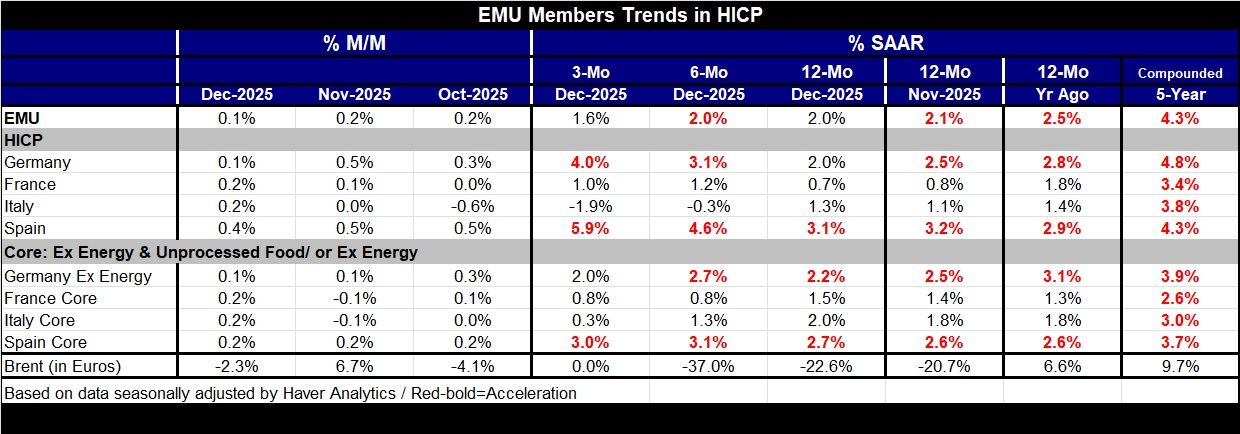

Headline Inflation in 2025 Headline inflation in 2025 rose by 2%, exactly on the target of the European Central Bank. It rose over six months at a 2% annual rate and then concluded the year over the last three months, rising at a 1.6% annual rate with some margin below the target set by the central bank itself.

Country Headline Inflation Trends On a country basis, the performance is not nearly as good. While year-on-year results look pretty good, with Germany at 2%, France at 0.7% and Italy at 1.3%, Spain comes in at 3.1%. So the three largest monetary union economies come in at or below 2% with Spain as a rogue observation. When we look further at the sequence of inflation within the year, we see Germany at 2% over 12 months, rising to 3.1% over 6 months, rising further to 4% over 3 months. Inflation is accelerating at the end of the year even as Germany hits the target! This is something to keep an eye on. For France, the inflation rate also accelerates slightly but stays below the bar of 2% over three months, six months, and 12 months. For Italy, inflation is decelerating from 1.3% over 12 months to -0.3% over six months, and then inflation in Italy is contracting at a 1.9% annual rate over three months. Spanish inflation shows clear trouble with a 3.1% 12-month pace, rising to 4.6% at an annual rate over six months, and rising further to 5.9% at an annual rate over three months.

Core Inflation For core inflation, the Monetary Union’s consolidated numbers are not yet compiled. However, for the four largest economies, we do have core or ex-energy inflation. For Germany, it's inflation excluding energy. On that basis, German inflation is 2.2% over 12 months, it rises to 2.7% over six months, then falls back to a 2% annual pace over three months All-in-all not a bad performance. For France, core inflation is below 2% over 12 months, six months, and three months. In Italy, once again, we see inflation decelerating: Italian inflation is 2% over 12 months - right on the ECB target. It falls to a 1.3% annual rate over six months and then falls further to a 0.3% annual rate over three months. For Spain, the core has another very difficult story for the Monetary Union. Inflation is 2.7% over 12 months, it rises to 3.1% over six months and stays at an annual rate of about 3% over three months. This is too high and it looks stubborn, particularly because it is the core.

Across the Big Four On balance, what we see is that the ECB grades-out well, based on headline inflation and based on its sequential performance for the European economic union as a whole. But large countries, show headline inflation building some steam particularly in the largest economy, Germany, and in Spain, the smallest of the BIG-4 economies. Inflation is once again mixed in the Monetary Union with German and Spanish inflation too high and with French and Italian inflation running either at or below the 2% mark and with Italy showing a tendency towards weaker prices for both the headline and the core. The change in prices over these various periods shows inflation gets the most help from oil prices over 12 months where Brent, measured in euros, falls by 22.6%; over six months Brent prices fall by 37% at an annual rate; and over three months Brent oil prices are unchanged, so that the headline isn't getting help at all from oil prices except through lagged effects.

Summing Up Meanwhile, there are some signs of stronger growth taking root in Europe, especially in Germany with better industrial production being logged and with German industrial production looking significantly stronger than the PMI data, suggesting that perhaps PMI data are missing something about the rebound that is developing. Nonetheless, it was a good year for inflation and the ECB; however, it doesn't exactly end the year in the catbird’s seat. On the other hand, it does not end the year behind the curve. There are scattered pressures and needs among member countries which always makes monetary policy difficult. When some countries need higher interest rates and others need lower interest rates, the ECB is in a difficult spot. Clearly, Spain and Germany are experiencing different phenomenon than France and Italy. That could be the policy challenge for the year ahead.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

Global

Global