Global| Apr 16 2019

Global| Apr 16 2019ZEW Optimism Steps Up A Bit

Summary

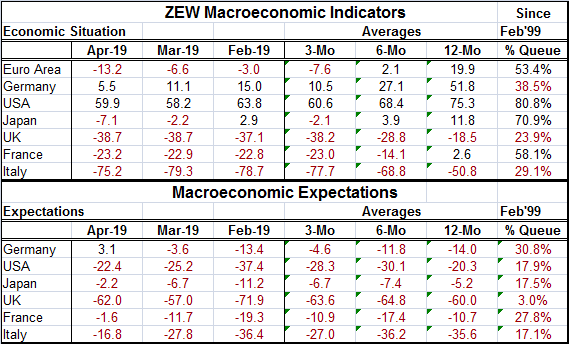

The ZEW financial experts see largely weaker conditions prevailing in April 2019, but they have lifted expectations for all countries in the table except the United Kingdom. The queue (or rank) standings for current conditions are [...]

The ZEW financial experts see largely weaker conditions prevailing in April 2019, but they have lifted expectations for all countries in the table except the United Kingdom. The queue (or rank) standings for current conditions are below their respective medians (below the 50% mark) for Germany, the U.S., and Italy. The EMU and France have values slightly above their respective median while the U.S. and Japan show strength.

The ZEW financial experts see largely weaker conditions prevailing in April 2019, but they have lifted expectations for all countries in the table except the United Kingdom. The queue (or rank) standings for current conditions are below their respective medians (below the 50% mark) for Germany, the U.S., and Italy. The EMU and France have values slightly above their respective median while the U.S. and Japan show strength.

Macroeconomic expectations find Germany as the only country with a positive expectation reading at 3.1. All expectations are below their respective medians (below 50%). The highest percentile readings are for Germany and France around the 30th percentile mark with the U.S., Japan and Italy at a 17th percentile mark and the U.K. at a near bottom 3rd percentile standing.

When I calculated these numbers, to be frank I went back to double-check my spread sheet because the results were not what I had expected. The IMF meeting concluded by cutting the global outlook especially for Germany, but ZEW experts are contrary to this with weaker current conditions admitted but improved expectations. ZEW experts also see weaker oil prices despite the fact that oil prices have been moving higher.

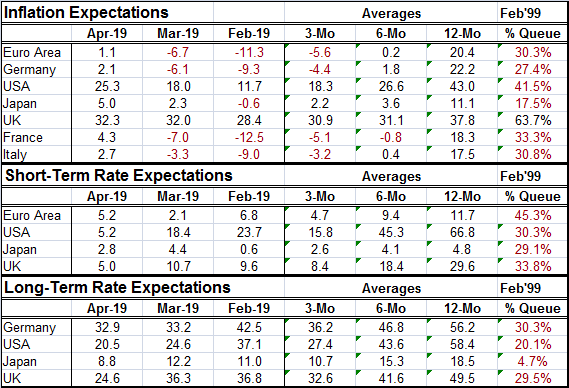

Inflation expectations that hit their lows around December have been gradually creeping higher. In April, they moved up again. Still, inflation expectations remain below their median everywhere except in the U.K. where Brexit is in play and exchange rate weakness threatens.

Interest rate expectations for the U.S. are shifting during the period very sharply. U.S. short-term rate expectations fell to 5.2 in April from 18.4 in March as the Fed pronounced its new policy of patience. That seems to be responsible for the heightened inflation expectations for the U.S. Those heightened expectations do not square with expectations from the University of Michigan survey or even with those extracted from TIPS spreads and inflation forecasts implicit in the yield curve. The ZEW results are mechanistic and seem to reject the trends and performance of the economy itself.

Fed policy seems to be working on the ZEW experts just the way the Fed wants it to work for the market overall (except it isn't). The Fed's pausing operation is raising ZEW inflation expectations by a lot and improving growth expectations. The Fed wants to raise inflation expectations and inflation so it can reach its target for inflation, but it has been unable to accomplish that. The ZEW experts seem to have the same model in mind as the Fed, but that doesn't mean that the world will work that way. And so far, it does not work that way.

ZEW experts' expectations show that conditions are not expected to be as dire as they had anticipated a few short months ago. However, by and large the conditions have not changed that much for the current assessment, to macroeconomic expectations to inflation expectations. The ZEW experts project a good deal of change stemming from the Fed's recent policy shift, mostly on the inflation and interest rate front, But conditions overall still are not much different from what they have been. ZEW members have things changing in a process that is slow-moving except for interest rate expectations in the wake of the new Fed policy path and some fiddling by the European Central bank.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief