U.S. JOLTS—Openings and Hiring Slid in June

by:Sandy Batten

|in:Economy in Brief

Summary

- Job openings fell 275,000 in June after having risen in each of the previous two months.

- Hiring fell 261,000, the largest monthly decline since June 2024.

- Separations fell 153,000, led by a 128,000 decline in quits.

- Layoffs edged down 7,000, the third monthly decline in the past four months.

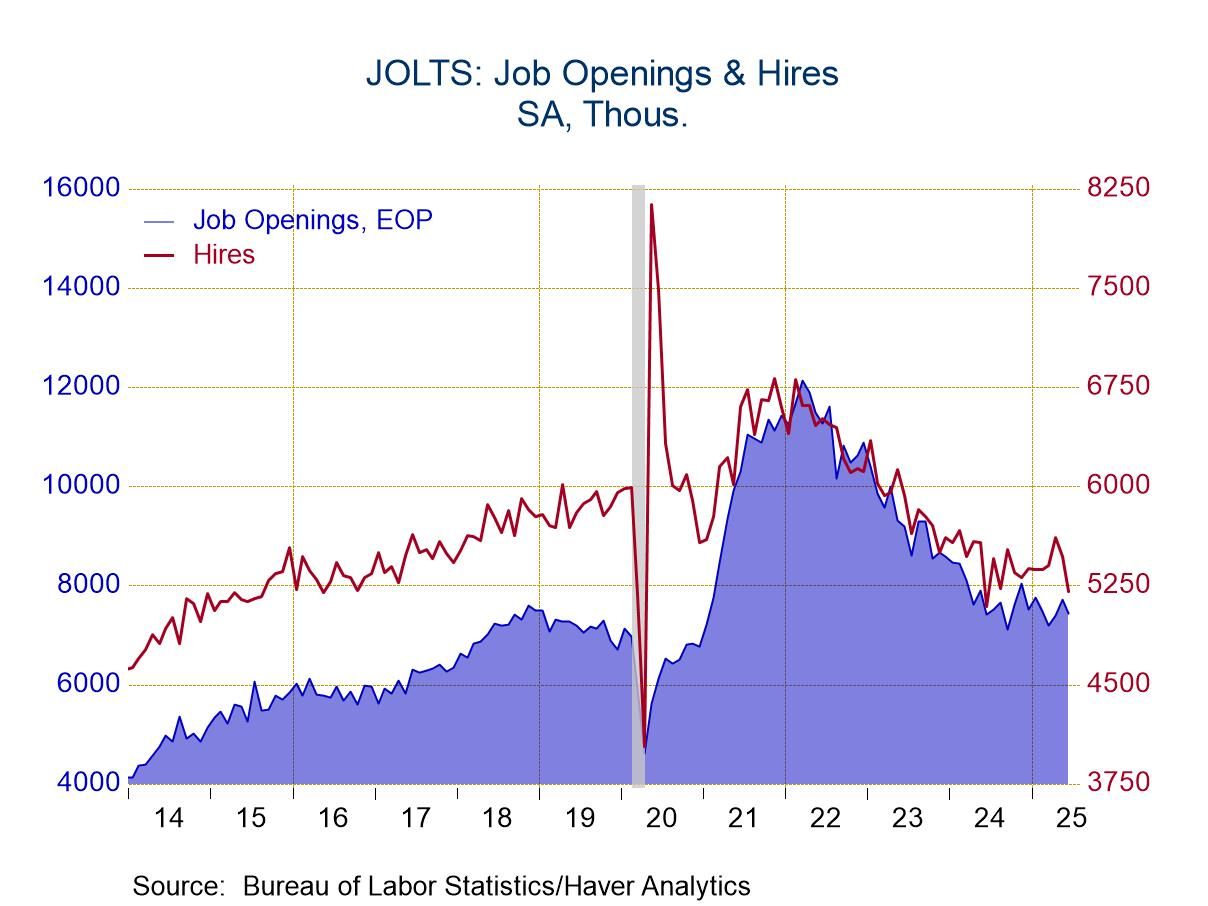

Job openings fell 275,000 (+0.3% y/y) in June to 7.437 million according to the Job Openings and Labor Turnover Survey. This was the first monthly decline in three months. The June fall was in line with market expectations. The May figure was revised down slightly to 7.712 million from the previously reported 7.769 million. The job openings rate fell to 4.4% in June from 4.6% in May. This rate has fluctuated between 4.3% and 4.8% over the past year. The record high for this rate was 7.4% reached in March 2022. This rate is calculated as the ratio of job openings to total nonfarm employment plus openings. The number of openings in June was 422,000 higher than the number of people unemployed, an increase from 475,000 in May and well below the 1.0-1.2 million gap that existed just prior to the pandemic, pointing to generally softer labor-market conditions.

Private sector openings decreased 325,000 (+1.5% y/y) in June to 6.551 million from 6.876 million in May. This was only the second y/y increase since July 2022. The private openings rate fell to 4.6% in June from 4.8% in May. The number of job openings decreased in accommodation and food services (-308,000), health care and social assistance (-244,000), and finance and insurance (-142,000). The number of job openings increased in retail trade (+190,000), information (+67,000), and state and local government education (+61,000).

Total hiring fell 261,000 (+2.3% y/y) to 5.204 million in June from 5.465 million in May. The hiring rate slipped to 3.3% from 3.4%. The June reading for the rate was the second lowest since the pandemic. Private sector hiring fell 246,000 in June on top of a 150,000 decline in May. The slide in hiring was led by a 133,000 decline in professional and business services hiring and a 148,000 drop in leisure and hospitality hiring. Government hiring fell 14,000, the fifth monthly decline in the past six months.

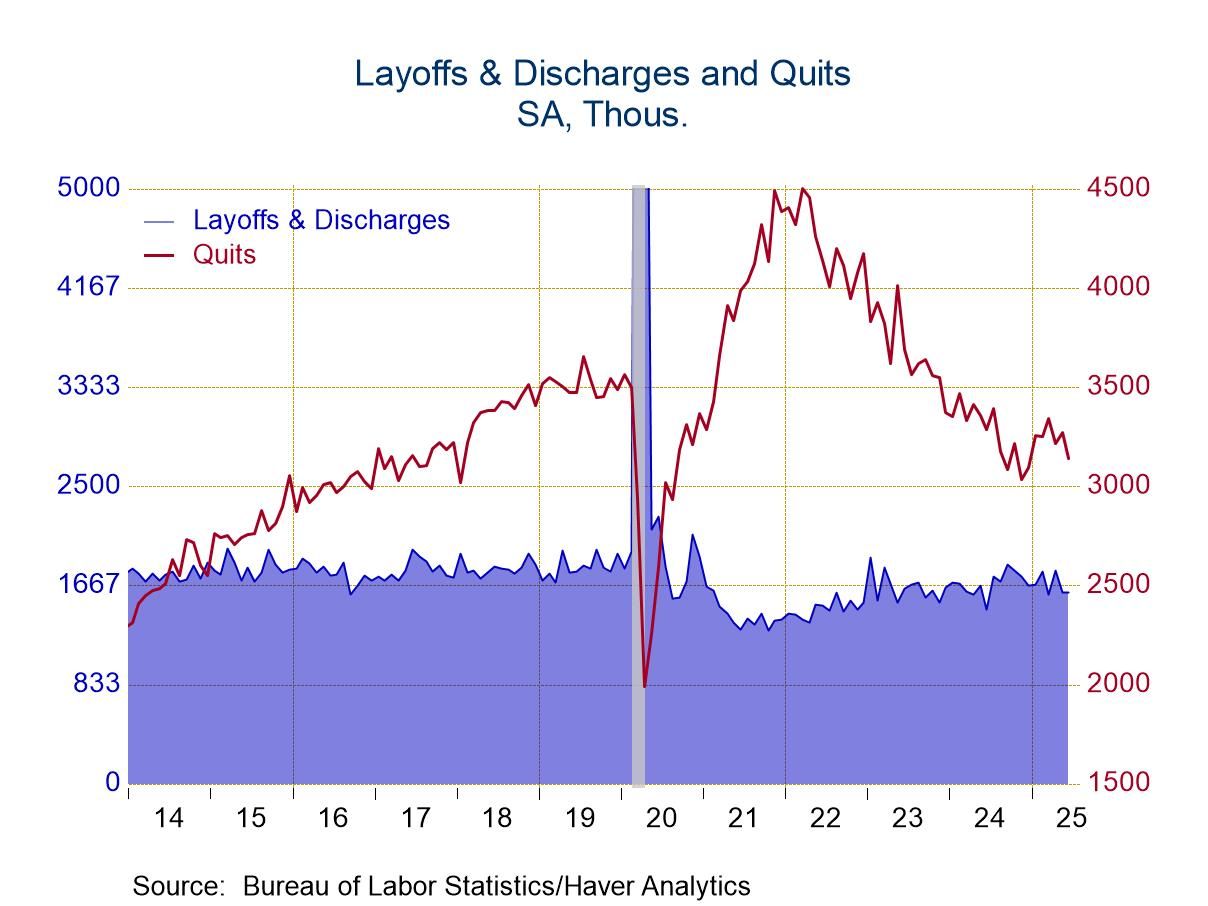

Total separations declined 153,000 (-0.1% y/y) to 5.060 million in June, the lowest level since August 2020 and the third monthly decline in the past four months. The separation rate slipped to 3.2%, tying the lowest rate in more than a decade, from 3.3% in May. Private separations fell 76,000 while government separations dropped 77,000, the largest monthly decline since July 2022. Total quits fell 128,000 (-4.3% y/y) to 3.142 million in June, the second monthly decline in the past three months, with the quits rate unchanged at 2.0%. Private sector quits decreased 102,000 in June. Quits are generally voluntary separations initiated by the employee. Therefore, the quits rate can serve as a measure of workers’ willingness or ability to leave jobs. In contrast, layoffs and discharges are involuntary separations initiated by the employer. Layoffs and discharges edged down 7,000 to 1.604 million in June with private layoffs increasing 22,000 while government layoffs declined 29,000.

The Job Openings and Labor Turnover Survey (JOLTS) data are available in Haver’s USECON database.

Sandy Batten

AuthorMore in Author Profile »Sandy Batten has more than 30 years of experience analyzing industrial economies and financial markets and a wide range of experience across the financial services sector, government, and academia. Before joining Haver Analytics, Sandy was a Vice President and Senior Economist at Citibank; Senior Credit Market Analyst at CDC Investment Management, Managing Director at Bear Stearns, and Executive Director at JPMorgan. In 2008, Sandy was named the most accurate US forecaster by the National Association for Business Economics. He is a member of the New York Forecasters Club, NABE, and the American Economic Association. Prior to his time in the financial services sector, Sandy was a Research Officer at the Federal Reserve Bank of St. Louis, Senior Staff Economist on the President’s Council of Economic Advisors, Deputy Assistant Secretary for Economic Policy at the US Treasury, and Economist at the International Monetary Fund. Sandy has taught economics at St. Louis University, Denison University, and Muskingun College. He has published numerous peer-reviewed articles in a wide range of academic publications. He has a B.A. in economics from the University of Richmond and a M.A. and Ph.D. in economics from The Ohio State University.

More Economy in Brief

Global

Global