Global| Jul 18 2017

Global| Jul 18 2017ZEW Financial Experts Show Few Significant Changes in Their View

Summary

The ZEW index in July continues to point to very strong prevailing current conditions in Germany against a minor step back for German expectations. However, the current assessment for the euro area is up solidly in July, rising to [...]

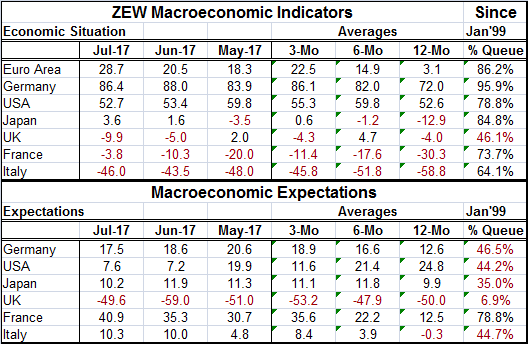

The ZEW index in July continues to point to very strong prevailing current conditions in Germany against a minor step back for German expectations. However, the current assessment for the euro area is up solidly in July, rising to 28.7 from June's 20.5 to an 86.2 percentile standing (on data since January 1999). The current assessment of the U.S., Japan and Italy has hardly changed in July. France logs a small improvement while the U.K. shows a small deterioration. Only the U.K. has a reading whose queue standing is below the 50% mark (the location of the median). The euro area, Germany and Japan have relatively elevated current ZEW readings above or about their respective top 15th percentiles. The U.S. and France have readings standing in their 70th percentile ranges; Italy has a 64th percentile standing. Since May the U.S. reading has weakened while the EMU reading has gotten considerably stronger. German and Italy are flat while France has been improving and the U.K. has been slipping. Clearly, momentum as well as strength is mixed. There is no sense of a global business cycle taking root.

The ZEW index in July continues to point to very strong prevailing current conditions in Germany against a minor step back for German expectations. However, the current assessment for the euro area is up solidly in July, rising to 28.7 from June's 20.5 to an 86.2 percentile standing (on data since January 1999). The current assessment of the U.S., Japan and Italy has hardly changed in July. France logs a small improvement while the U.K. shows a small deterioration. Only the U.K. has a reading whose queue standing is below the 50% mark (the location of the median). The euro area, Germany and Japan have relatively elevated current ZEW readings above or about their respective top 15th percentiles. The U.S. and France have readings standing in their 70th percentile ranges; Italy has a 64th percentile standing. Since May the U.S. reading has weakened while the EMU reading has gotten considerably stronger. German and Italy are flat while France has been improving and the U.K. has been slipping. Clearly, momentum as well as strength is mixed. There is no sense of a global business cycle taking root.

ZEW expectations find all outlook metrics below their respective 50th percentiles except in France where there is a firm 78.8 percentile standing. The U.K. has a very low 6.9 percentile standing with Germany, the U.S. and Italy clustered around standings at the 44th percentile to the 46th percentile and with Japan a bit weaker at a 35th percentile standing. Since May the U.S. and German outlooks have weakened while Japan and the U.K. are nearly unchanged as France and Italy have logged some degree of improvement. There is no sense of any watershed change or of any strong improving situation with the possible exception of France. Although globally manufacturing PMI gauges have been gathering strength, this is not being generalized.

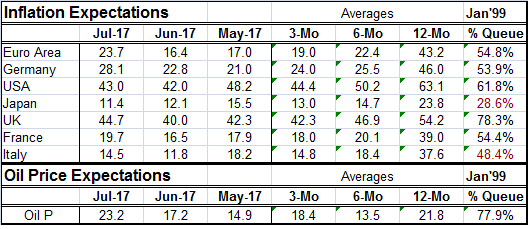

Inflation expectations are tempered. While only two countries show below 50th percentile readings (Japan and Italy). Only the U.K., with weak-sterling inspired inflation, shows a reading in the 70th percentile or higher (at 78.3%). And the U.K. inflation data reported out today showed a break in the uptrend for inflation there. Moreover, there has not been evidence of a spreading of imported inflation in the U.K. to domestic prices. The U.S. has the second highest percentile standing at its 61st percentile, but that raw score has been steadily falling and recent U.S. inflation news has surprised to the downside. Euro area, German and French readings are clustered around readings registering very modest standings in their 54th percentile. The inflation expectations across countries have remained modest in their rank standings, even as the reading for oil has moved up solidly since May and now has a 77.9 percentile standing.

On balance, the ZEW experts are not building a fear of inflation despite seeing oil on a path (apparently) to normalization. The growth splits that ZEW experts have seen among these countries remain largely in force, but within the euro area growth is seen as becoming stronger. Raw expectations are mostly tempered. However, since May ZEW members expectations for inflation have been creeping upward everywhere except for the U.S., Italy and Japan. Apparently, ZEW members see the situation in the EMU leaning in a way that monetary policy could soon be switched to a less accommodative mode. ZEW short-term interest rate expectations for the euro area are firming slightly. For the U.S., they are slightly easier but still highly anticipatory of further Fed rate hikes. In Japan, expectations for rate hikes are low and hardly changed in recent months. For the U.K., rate hike expectations are palpable with a 65th percentile standing. These expectations moved higher in July in the wake of the Bank of England's reported split vote on policy. But with today's better-than-expected inflation news and Brexit talks in train, it is still far from clear that the BOE is going to pull the trigger on higher rates anytime soon.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief