Global| Dec 31 2008

Global| Dec 31 2008Various Money Supplies are Showing the Impact of Stimulus

Summary

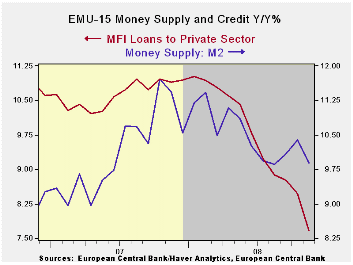

European money supply trends show that Yr/Yr money supply growth is steady or slowing slightly on a Yr/Yr basis (chart). Over other time horizons (see table) some stimulus is indicated. Inflation adjusted “real balances’ show a bit [...]

European money supply trends show that Yr/Yr money supply growth is steady or slowing slightly on a Yr/Yr basis (chart). Over other time horizons (see table) some stimulus is indicated. Inflation adjusted “real balances’ show a bit more stimulus. But credit growth in EMU is clearly slowing. If the objective of monetary stimulus has been to get credit growth higher, it is not working.

Across other select G-7 countries the same trends with money hold forth – Japan is an exception of sorts. The US and the UK show sharply escalating money growth rates over more recent periods. Japan shows nominal money growth is decelerating. But in terms of real balances US, UK and Japan real balance growth is expanding.

Still, the lesson in the Euro Area is telling. For all the monetary stimulus that is in train, there is little evidence that credit growth is being rekindled.

| Look at Global and Euro Liquidity Trends | |||||||

|---|---|---|---|---|---|---|---|

| Saar-all | Euro Measures (EA 15): Money & Credit | G-10 Major Markets: Money | Memo | ||||

| €€-Supply M2 | Credit:Resid | Loans | $US M2 | ££UK M4 | ¥¥Jpn M2+Cds | OIL:WTI | |

| 3-MO | 11.9% | 2.9% | 4.7% | 14.5% | 25.6% | 0.0% | -94.0% |

| 6-MO | 10.0% | 5.9% | 5.4% | 7.8% | 21.8% | 1.5% | -78.6% |

| 12-MO | 9.9% | 8.4% | 7.6% | 7.6% | 16.6% | 1.8% | -39.1% |

| 2Yr | 10.7% | 10.3% | 9.2% | 6.7% | 13.9% | 1.9% | -1.3% |

| 3Yr | 10.0% | 10.7% | 9.8% | 6.2% | 13.6% | 1.4% | -0.3% |

| Real Balances: deflated by Own CPI. Oil deflated by US CPI | |||||||

| 3-MO | 12.8% | 3.7% | 5.4% | 27.6% | 24.2% | 2.8% | -93.3% |

| 6-MO | 9.2% | 5.1% | 4.6% | 9.9% | 17.7% | 0.9% | -78.1% |

| 12-MO | 7.6% | 6.2% | 5.4% | 6.5% | 12.0% | 0.8% | -39.7% |

| 2Yr | 7.9% | 7.5% | 6.5% | 3.9% | 10.5% | 1.1% | -3.9% |

| 3Yr | 7.5% | 8.2% | 7.3% | 3.6% | 10.3% | 0.8% | -2.6% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief