Global| Jan 31 2007

Global| Jan 31 2007US 4Q GDP Growth Firmer Than Expected

by:Tom Moeller

|in:Economy in Brief

Summary

U.S. real GDP grew 3.5% (AR) last quarter. It was both the fastest growth since 1Q06 and beat Consensus expectations for a 3.0% rise. The yearend figure raised growth for the full year to 3.4%, slightly ahead of 3.2% during 2005. A [...]

U.S. real GDP grew 3.5% (AR) last quarter. It was both the fastest growth since 1Q06 and beat Consensus expectations for a 3.0% rise. The yearend figure raised growth for the full year to 3.4%, slightly ahead of 3.2% during 2005.

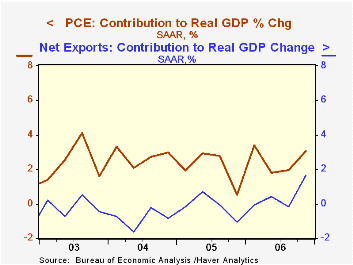

A 1.6 percentage point contribution to growth from an improved net export deficit was the largest contribution from foreign trade in ten years. It came due to a 2.4% (9.2% y/y) gain in exports while imports fell 3.2% (+3.1% y/y). Final sales to domestic purchasers managed a respectable 2.4% gain despite a 19.2% (-12.6% y/y) drop in residential investment. That was the largest shortfall since early 1991. Personal consumption expenditures grew 4.4% (3.7% y/y) as spending on furniture & household equipment soared 15.1% (11.7% y/y).

Nonresidential fixed investment fell 0.4% (6.8% y/y) after a 10.% gain the prior quarter. Spending in each sector fell except for information processing equipment which rose a slight 1.8% (7.8% y/y) after a 10.0% jump during 3Q.

Final sales to domestic purchasers managed a respectable 2.4% gain despite a 19.2% (-12.6% y/y) drop in residential investment. That was the largest shortfall since early 1991. Personal consumption expenditures grew 4.4% (3.7% y/y) as spending on furniture & household equipment soared 15.1% (11.7% y/y).

Nonresidential fixed investment fell 0.4% (6.8% y/y) after a 10.% gain the prior quarter. Spending in each sector fell except for information processing equipment which rose a slight 1.8% (7.8% y/y) after a 10.0% jump during 3Q.

Reduced inventory accumulation subtracted 0.7 percentage points to 4Q GDP after positive contributions during the prior two quarters.

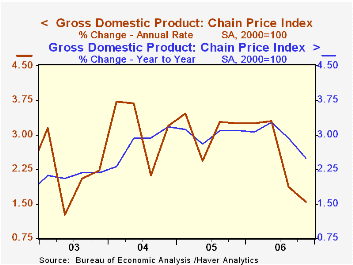

The GDP chain price index rose just 1.5%, its weakest quarterly advance since early 2003. The gain was restrained by a decline (-0.8%, +1.9% y/y) in the PCE chain price index which fell not only because of lower energy prices but lower durable goods prices as well. The services chain price index rose 3.4% (3.15 y/y), its fastest gain in a year. Less food & energy the PCE chain price index grew 2.1% (2.3% y/y).

Milton Friedman on Inflation from the Federal Reserve Bank of St. Louis is available here.

| Chained 2000$, % AR | 4Q '06 | 3Q '06 | Y/Y | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|

| GDP | 3.5% | 2.0% | 3.4% | 3.4% | 3.2% | 3.9% |

| Inventory Effect | -0.7% | 0.1% | -0.1% | 0.3% | -0.3% | 0.4% |

| Final Sales | 4.2% | 1.9% | 3.5% | 3.1% | 3.5% | 3.5% |

| Foreign Trade Effect | 1.6% | -0.2% | 0.7% | 0.1% | -0.1% | -0.5% |

| Domestic Final Demand | 2.4% | 2.0% | 2.8% | 3.0% | 3.6% | 4.0% |

| Chained GDP Price Index | 1.5% | 1.9% | 2.5% | 2.9% | 3.0% | 2.8% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.