Global| Aug 19 2009

Global| Aug 19 2009UK's CBI Orders Continue To Lag

by:Tom Moeller

|in:Economy in Brief

Summary

The Confederation of British Industry continues to see very weak orders in both its domestic and export surveys. Both total and export orders are in the lower ten percentile of their historic range of values. Stocks of goods with a [...]

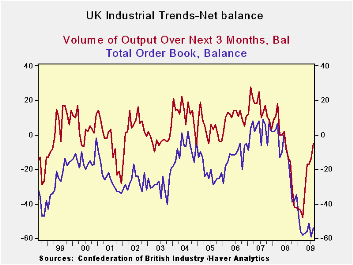

The Confederation of British Industry continues to see very

weak orders in both its domestic and export surveys. Both total and

export orders are in the lower ten percentile of their historic range

of values. Stocks of goods with a diffusion reading that fell to +13

from +20 are now near their range mid range (standing at their 45th

percentile) and are well below their 12-monhth average, showing

inventory progress has been made. In contrast orders are weaker than

their 12-month averages. What ever is getting better it does not seem

to be boosting orders despite the gain in August.

To compare with that finding we have the contrary result that

although orders are very weak output volume over the next three months

is expected to do much better. The survey measure rose to -5 in August

from -14 in July, thrusting output volume expectations into the 57th

percentile of their range, far better than the reading for orders. The

average price expected has however slipped in August to -17 from -6 in

June. That is on the lower 6 percentile of its range. These readings

contrast with the UK MFG readings from NTC which at 50.84 is indicating

expansion and stands in the 74th percentile of its range. (The NTC

survey is also a diffusion survey but it presents its statistics as

dose the US ISM rather than as an ‘up’ minus ‘down’ diffusion index as

the one used by the CBI. For the CBI, zero is neutral; for the NTC

index, 50 is the neutral mark. Also the NTC index is for manufacturing

not all of industry, as is the CBI report.)

The outlook portion of the CBI index is relatively more

positive, but still is not as upbeat as the Markit/NTC index. And the

orders assessment from the CBI is downright depressing as its

improvement in July still leaves the index lower over three months and

longer. The picture of the UK MFG industry is curiously mixed. The

differences are not simply those between different surveys but among

somewhat related measures in the same survey.

| UK Industrial volume data CBI Survey | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Reported: | Aug 09 |

Jul 09 |

Jun 09 |

May 09 |

Apr 09 |

12MO Avg | Pcntle | Max | Min | Range |

| Total Orders | -54 | -59 | -51 | -56 | -57 | -43 | 7% | 9 | -59 | 68 |

| Export Orders | -48 | -45 | -52 | -46 | -34 | -36 | 7% | 3 | -52 | 55 |

| Stocks: FinGds | 13 | 20 | 22 | 30 | 28 | 25 | 45% | 31 | -2 | 33 |

| Looking ahead | ||||||||||

| Output Volume: Nxt 3M | -5 | -14 | -17 | -17 | -32 | -31 | 57% | 28 | -48 | 76 |

| Avg Prices 4Nxt 3m | -17 | -6 | -13 | -20 | -10 | -1 | 6% | 34 | -20 | 54 |

| From end 2000 | ||||||||||

| Compare to NTC MFG | ||||||||||

| Jul 09 |

Jun 09 |

May 09 |

Apr 09 |

12MO Avg | Pcntle | Max | Min | Range | ||

| UK MFG | 50.84 | 47.36 | 45.40 | 43.13 | 41.22 | 74% | 56.32 | 34.93 | 21 | |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief