Global| Jan 17 2014

Global| Jan 17 2014UK Retail Sales Surge in Holiday Season

Summary

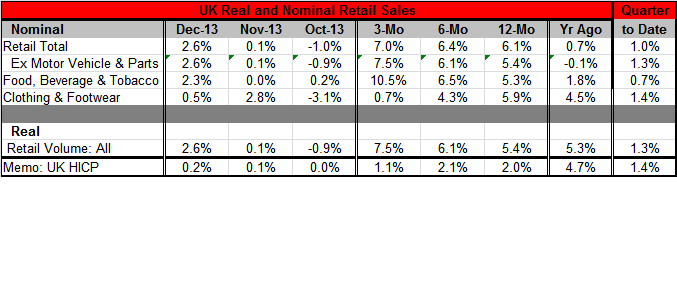

UK retail volumes had been strong all year long but in December sales really jumped. Retail sales rose by 2.6% in December alone. That offset two weak months and propelled sales up over three-months at a 7% annual rate. Sales have [...]

UK retail volumes had been strong all year long but in December sales really jumped. Retail sales rose by 2.6% in December alone. That offset two weak months and propelled sales up over three-months at a 7% annual rate. Sales have gradually accelerated in both real and nominal terms over 12-months, to 6-months, to 3-months.

UK retail volumes had been strong all year long but in December sales really jumped. Retail sales rose by 2.6% in December alone. That offset two weak months and propelled sales up over three-months at a 7% annual rate. Sales have gradually accelerated in both real and nominal terms over 12-months, to 6-months, to 3-months.

While the UK sales results are impressive, there are identifiable weaknesses. In the current quarter, just completed retail sales growth has slowed to 1% in nominal terms and 1.3% in real terms despite the strong December gain. While food and ex-motor vehicle sales categories both have accelerated throughout the year, clothing and footwear sales lag and disappoint. Clothing and footwear sales have persistently slowed from a 5.9% pace over 12-months to a 4.3% pace over 6-months to a weak 0.7% pace over 3-months.

The UK construction sector and manufacturing sector, led by the auto sector, have punched out strong numbers all year long. But construction has now lost some momentum. At the same time the Bank of England has finally gotten its inflation numbers to fall into line. 2013 has been a very constructive year for the UK economy. It is clearly doing better than the euro area and better than just about any country in Europe save Germany where the juggernaut of moderation plows ahead. But of course, UK autos sales growth far outstripped Germany's in 2013.

The UK has been a model of recovery, but can it be sustained? The UK has logged a strong increase in its manufacturing PMIs and also is the top country in the EU in terms of the strength of its services sector. But this sort of growth comes at a cost, and the UK external accounts have begun to deteriorate.

The UK is still caught in the middle of an EU imbroglio to impose a `Tobin Tax' on financial transactions. Since the UK leans heavily on its banking sector, it is opposed to this practice. That is only one of the things that the UK must mind as its banking sector is still struggling to recover from its financial crisis woes. The UK, too, will see its recovery affected by progress on the continent. It is not a participant in the common currency, but it is an EU member and its trade will depend on recovery in its export markets.

The UK is poised for good things as 2014 begins. It still is licking its wounds, but it has its key sectors, manufacturing and services on an upswing at the same time. Its construction sector is engaged in some retrograde motion; however, with the rest of the economy improving, that should turnaround in 2014.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.