Global| Feb 14 2007

Global| Feb 14 2007U.S. Retail Sales Eased After Firmed December

by:Tom Moeller

|in:Economy in Brief

Summary

In January, US retail sales slipped marginally after a December gain that was revised up to 1.2% from 0.9% reported initially. The figure for last month fell short of Consensus expectations for a modest 0.3% rise. Excluding autos, [...]

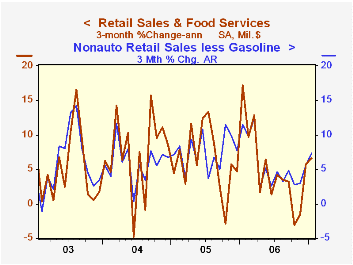

In January, US retail sales slipped marginally after a December gain that was revised up to 1.2% from 0.9% reported initially. The figure for last month fell short of Consensus expectations for a modest 0.3% rise.

Excluding autos, retail sales added 0.3% to an upwardly revised 1.3% December gain, revised from 1.0%.

Sales by motor vehicle & parts dealers reversed all of the December increase with a 1.3% (-1.7% y/y) decline, helped by a 0.1% slip in new unit vehicle sales.

Gasoline service station sales fell 0.7% after the 3.6% jump during December reflecting the 3.2% drop in gasoline prices to an average $2.24 per gallon.Nonauto retail sales less gasoline rose 0.5% (4.3% y/y) last month after an upwardly revised 1.0% spurt during December.

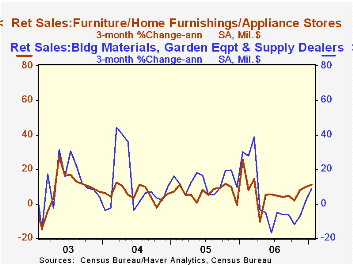

Sales of discretionary items were generally firm last month. Sales at general merchandise stores rose 1.3% (5.6% y/y) after an upwardly revised 1.2% December increase.Apparel store sales also were firm with a 1.0% (4.6% y/y) after a December spurt that was about doubled to 1.1%. Furniture, home furnishings & appliance stores, however, slipped after a December increase that was halved to 0.8%. The huge December gain in sales at electronics & appliance stores was lowered to 1.8% from 3.0%, then sales fell 1.2% last month.

Building material sales rose 0.8% (-3.1% y/y) after a very much upwardly revised 0.7% December increase. Sales of nonstore retailers (internet & catalogue) rose a moderate 0.5% (8.4% y/y) but restaurant and bar sales fell 0.7% (5.3% y/y) after a firm December gain that was upwardly revised a 3.1%.

Chairman Ben S. Bernanke's Senate Testimony, The Semiannual Monetary Policy Report to the Congress, can be found here.

| January | December | Y/Y | 2006 | 2005 | 2004 | |

|---|---|---|---|---|---|---|

| Retail Sales & Food Services | -0.0% | 1.2% | 2.3% | 6.3% | 7.2% | 6.2% |

| Excluding Autos | 0.3% | 1.3% | 3.4% | 7.5% | 8.3% | 7.2% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief