Global| Mar 28 2008

Global| Mar 28 2008U.S. Real DPI Up 0.3%, Real PCE Flat, Prices Easy

by:Tom Moeller

|in:Economy in Brief

Summary

Nominal personal income grew 0.5% last month and beat Consensus expectations for a 0.3% gain. The rise lifted the three-month growth in income to 4.8%, its best since September. Wage & salary income moderated a bit and rose 0.3% after [...]

Nominal personal income grew 0.5% last month and beat Consensus expectations for a 0.3% gain. The rise lifted the three-month growth in income to 4.8%, its best since September.

Wage & salary income moderated a bit and rose 0.3% after January's 0.5% increase. Factory sector wages rose 0.3% (+0.4% y/y) and wages & salaries in the private service-providing industries rose 0.3% (3.9% y/y). That y/y increase is much reduced from the 6.4% gain last year as well as from the 6.8% 2006 rise. Wages in the government sector rose a strong 0.5% (5.1% y/y) but here the story is one of acceleration after a 4.6% rise last year and a 4.1% 2006 increase.

Lower interest rates caused the fifth straight monthly decline

in interest income (+3.6% y/y). That y/y increase was less than one

third the rate of gain at the end of 2005. Dividend income rose another

firm 0.6% (11.5% y/y), a double digit rate of gain that is down

somewhat from its peak 16.3% in 2006.

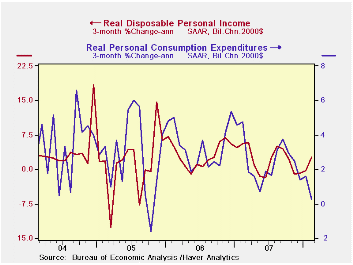

Disposable personal income growth improved last month to 0.5% which was its best increase since last August. The rise followed 0.4% gains during the prior two months. It raised the thee month growth rate to 5.5% (AR). Adjusted for prices, which moderated, real disposable income rose 0.3% and the three month growth rate picked up to 2.6%.

Personal consumption expenditures rose just the expected 0.1%. Real personal consumption expenditures were flat. That lowered the three-month growth rate to 0.3%, its worst since October 2005.

Real spending on discretionary items continued weak. Motor vehicle & parts purchases did rise 0.3% but three month growth fell to -7.4%. Real spending on household furniture & appliances also rose 0.3%, as it did in January, but three month growth fell to -2.1%. Real spending on apparel rose 1.4% however because of a sharp decline in December, three month growth improved only to -1.5%. These and other detailed spending figures are available in Haver's USNA database.

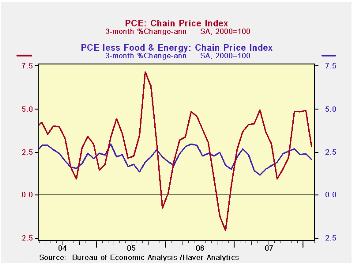

The PCE chain price index rose just 0.1% as energy prices fell 1.9%. The core PCE price index matched expectations and rose just 0.1%. The three month growth in prices fell to 2.1%, down from the three month gains of 2.7% registered last year.

The personal savings rate improved somewhat to all of 0.3% from the negative 0.1% during January.

Yesterday's speech by Fed GovernorFrederic S. Mishkin on

inflation titled Comfort Zones, Shmumfort Zones can

be found here.

| Disposition of Personal Income (%) | February | January | Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| Personal Income | 0.5 | 0.3 | 4.6 | 6.2 | 6.6 | 5.9 |

| Disposable Personal Income | 0.5 | 0.4 | 4.7 | 5.7 | 5.9 | 4.7 |

| Personal Consumption | 0.1 | 0.4 | 5.1% | 5.5 | 5.9 | 6.2 |

| Saving Rate | 0.3 | -0.1 | 0.9 (Feb. 07) | 0.4 | 0.4 | 0.5 |

| PCE Chain Price Index | 0.1 | 0.3 | 3.4 | 2.5 | 2.8 | 2.9 |

| Less food & energy | 0.1 | 0.2 | 2.0 | 2.1 | 2.2 | 2.2 |

by Tom Moeller March 28, 2008

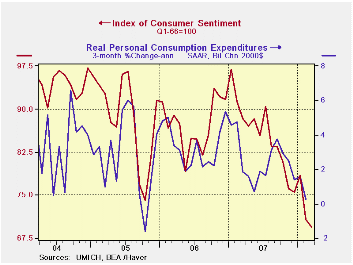

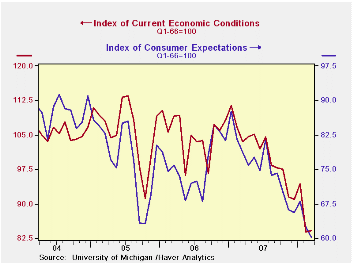

The University of Michigan's consumer sentiment index for all of March fell 1.8% m/m to 69.5. That was larger than the 0.4% decline in the preliminary reading and it was just slightly greater than Consensus expectations for a reading of 70.

The index of expected business conditions during the next year still accounted for all of the decline in March sentiment. The 3.7% decline followed an 8.4% February drop and left the index at its lowest since early 1992. Expectations for business conditions during the next year fell 14.8% (-51.6% y/y). hat m/m drop was double the decline in the preliminary report. And expectations for conditions over the next five years fell m/m rather than rose. Expectations for personal finances also were unchanged rather than posting a slight rise.

Opinions about government policy fell slightly m/m (-23.6%

y/y) following the sharp 11.5% drop during February. The percentage of

those surveyed who indicated that they thought government was doing a

good job rose somewhat but 44% had a poor opinion.

Expectations for inflation during the next twelve months surged to 4.6%, the highest level in nearly two years though inflation expectations during the next five to ten years fell slightly to 3.3%. That was the same expectation as in the preliminary reading.

The current conditions index fell 0.5% m/m after the 11.2% February plunge. The view of current conditions for buying large household goods improved slightly but the view of current personal finances fell for the fourth month in the last five (-16.2% y/y).

The University of Michigan survey is not seasonally adjusted.The reading is based on telephone interviews with about 500 households at month-end; the mid-month results are based on about 300 interviews. The summary indexes are in Haver's USECON database, with details in the proprietary UMSCA database.

| University of Michigan | March | March (Prelim) | Feb | Jan | March y/y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|---|---|

| Consumer Sentiment | 69.5 | 70.5 | 70.8 | 78.4 | -21.4% | 85.6 | 87.3 | 88.5 |

| Current Conditions | 84.2 | 84.6 | 83.8 | 94.4 | -18.6% | 101.2 | 105.1 | 105.9 |

| Expectations | 60.1 | 61.4 | 62.4 | 68.1 | -23.6% | 75.6 | 75.9 | 77.4 |

by Robert Brusca March 28, 2008

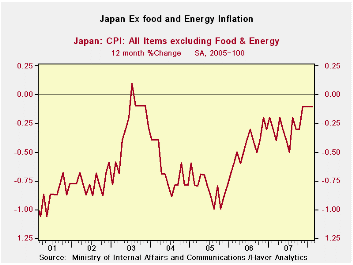

Japan has been gradually making progress toward ridding itself of its chronic deflation. Headline inflation now has turned positive year-over-year and is positive over three months as well as over the six-month horizon. The 12-month calculations are markedly different from the year ago calculations which refer to the previous 12-month period when the economy was more firmly in the grip of deflation. Still, core inflation (ex-food and energy) has not yet moved up above the zero mark.>

In the quarter to date, inflation also has a positive tone. Headline inflation is up at a 1% pace while the core is up at a 0.4% pace and ex-food prices are rising at a 2.3% rate. Most CPI components are rising in the first quarter of 2008 as well.

For Japan this mild inflation is a mark of success while other countries are suffering with true inflation risks. Japan is emerging from its battle with deflation, but it is still fighting to secure growth.

| Japan CPI Trends | ||||||||

|---|---|---|---|---|---|---|---|---|

| Feb-08 | Jan-08 | Dec-07 | 3-mo | 6-mo | 12-mo | Yr-Ago | Qtr-to-Date | |

| All items | 0.1% | 0.0% | 0.1% | 0.8% | 1.2% | 1.0% | -0.8% | 1.0% |

| All items less food and energy | -0.1% | 0.1% | -0.1% | -0.4% | 0.2% | -0.1% | -1.2% | 0.4% |

| All items except fresh food | 0.1% | 0.1% | 0.4% | 2.4% | 1.8% | 1.0% | -0.4% | 2.3% |

| seasonally adjusted BY Haver | ||||||||

| Food & Beverage | 0.2% | -0.2% | 0.1% | 0.4% | 0.0% | 1.2% | 0.4% | -0.5% |

| Housing | 0.0% | 0.0% | 0.1% | 0.4% | 0.2% | 0.0% | -1.2% | 0.3% |

| Clothing and Personal | -0.2% | 0.2% | 0.0% | 0.0% | -0.2% | 0.7% | 1.6% | 0.8% |

| Education | 0.1% | 0.1% | 0.0% | 0.8% | 0.8% | 0.7% | 3.2% | 0.9% |

| Medical care | -0.1% | 0.1% | 0.0% | 0.0% | -0.8% | 0.1% | -1.2% | 0.2% |

| Miscellaneous | -0.1% | 0.1% | 0.0% | 0.0% | 0.4% | 0.5% | 4.5% | 0.1% |

| Reading & Recreation | -0.3% | 0.1% | -0.3% | -2.0% | -0.8% | -0.9% | -4.4% | -1.2% |

| Transport & Communication | -0.1% | 0.2% | 1.0% | 4.4% | 5.0% | 3.1% | -1.6% | 5.7% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief