Global| Aug 31 2006

Global| Aug 31 2006U.S. Personal Income Again Up 0.6%, Core Price Inflation Eased

by:Tom Moeller

|in:Economy in Brief

Summary

Personal income increased 0.6% last month, the same as during June which was unrevised. The gain slightly outpaced Consensus expectations for a 0.5% rise. Wage & salary disbursements again were strong and rose 0.6% (7.9% y/y) for the [...]

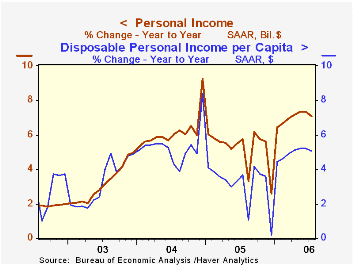

Personal income increased 0.6% last month, the same as during June which was unrevised. The gain slightly outpaced Consensus expectations for a 0.5% rise.

Wage & salary disbursements again were strong and rose 0.6% (7.9% y/y) for the second consecutive month. Wages in the private service-producing industries paced the increase with a 0.8% (8.6% y/y) while factory sector wages rose a lesser 0.3% (7.5% y/y) but the June increase was revised up to 0.5%.

Interest income fell 0.1% (9.6% y/y) after three months of greater than 1.0% increase and dividend income jumped another 1.0% (11.3% y/y).

Disposable personal income jumped 0.7% (6.0% y/y), up from the 0.5% average of this year's first six months. Personal taxes fell 0.3% (+14.9% y/y).

Adjusted for price inflation, disposable personal income rose 0.3% (2.5% y/y). Real disposable income per capita rose 0.3% (1.6% y/y), the same as the prior monthPersonal consumption jumped 0.8%, double the prior month's unrevised increase and matched Consensus expectations. Adjusted for price inflation spending posted the largest increase of the year with a 0.5% gain (2.4% y/y) led by a 1.6% (-1.7% y/y) rise in real durables spending.

The PCE chain price index rose a less than expected 0.3% and the prior month's gain was revised down. Less food & energy prices rose 0.1% (2.4% y/y), the smallest m/m increase this year. Expectations had been for a 0.2% rise.

The personal savings rate was again negative, but prior month's figures were revised less negative. Should the Decline in the Personal Saving Rate Be a Cause for Concern? from the Federal Reserve Bank of Kansas City is available here.

A Primer on Inflation (with Comments on Real Estate in the Metroplex), yesterday' speech by Dallas Federal Reserve Bank President Fisher can be found here.

| Disposition of Personal Income | July | June | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Personal Income | 0.6% | 0.6% | 7.1% | 5.2% | 6.2% | 3.2% |

| Personal Consumption | 0.8% | 0.4% | 5.9% | 6.5% | 6.6% | 4.8% |

| Savings Rate | -0.9% | -0.7% | -0.9% (July '05) | -0.4% | 2.0% | 2.1% |

| PCE Chain Price Index | 0.3% | 0.1% | 3.4% | 2.9% | 2.6% | 2.0% |

| Less food & energy | 0.1% | 0.2% | 2.4% | 2.1% | 2.0% | 1.4% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief