Global| Nov 03 2017

Global| Nov 03 2017U.S. ISM Nonmanufacturing Index Moves Even Higher; But Breadth Isn't Strength

Summary

The U.S. nonmanufacturing ISM index has moved even higher in October and this is one report that shows no impact whatsoever from hurricane damage. In fact, in September the nonmanufacturing index moved even more sharply higher from [...]

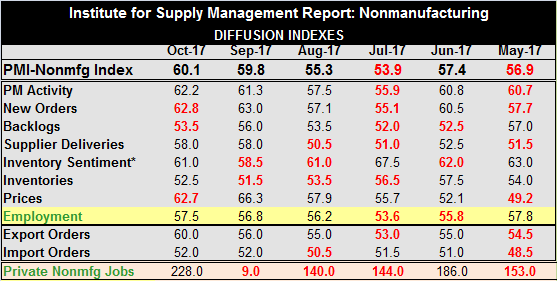

The U.S. nonmanufacturing ISM index has moved even higher in October and this is one report that shows no impact whatsoever from hurricane damage. In fact, in September the nonmanufacturing index moved even more sharply higher from its August reading. Only three components weakened month-to-month in October: new orders, order backlogs and prices. The price component fell relatively sharply month-to-month to 62.7 in October from 66.3 in September. Price tends to be a good cyclical indicator.

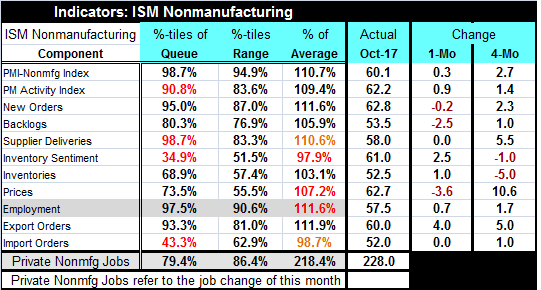

The table below generates several different schemes to rate or rank the overall ISM headline as well as the value of the components. I prefer to refer to the 'queue percentile' standings. That measure ranks each metric in October expressing its standing as a percentile positon in the historic queue of data. The 'range percentile' expresses the current month's standing as a percentile position between the high and low historic readings. The third data column in the table expresses each metric as a percentage of its own historic average. At the bottom of the table, private nonfarm jobs gains for October are similarly evaluated. The ISM headline, employment, orders, supplier deliveries and exports are exceptional on all the ranking schemes.

Several factors stick out in this report. Even though the month's job gain was distorted (up!) by rebounding from a weak hurricane-affected survey the month before, the percentile standing for actual private job gains in October at 79.4% is well below the 97.5 percentile standing reported in the ISM. Data on job growth show that year-on-year services sector and nonmanufacturing jobs growth is slipping; yet, the ISM jobs metric is holding to an extremely strong reading and pushing higher. That needs a reality check.

This is a reminder that the ISM measures breadth rather than strength. It appears that job growth is extremely broad and that it is much broader than it is strong.

In the same vein, we have extremely high ISM standings for the overall index, activity, new orders and export orders. Here too, let's keep in mind that the ISM is a report about breadth. What we have is evidence that improving trends are much more widespread than they normally are. However, even in the case of industrial output and the ISM manufacturing, the ISM manufacturing survey seems much stronger (output gains are broader than is manufacturing output strong) than its counterpart real-world data.

The chart shows nonmanufacturing import's raw diffusion value plotted against the headline ISM. That chart also shows a disconnect of sorts since if the economy is doing well we expect imports to be strong. What we see in the chart and confirmed in the table is that imports are not as strong as the headline and in fact are quite a bit weaker. Maybe nonmanufacturing imports are not the best barometer of the strength of the U.S. economy. But this is another gap in the credibility of this report. Yet, another gap is the difference in the readings for nonmanufacturing ISM from the services reading in Markit's survey for the U.S. The ISM is signaling something and I think it is telling us that the recovery is spreading more broadly. We already know that this early phase of recovery was centered on cities and that a lot of more rural America has been left on the side lines. So there is plenty of opportunity for a broadening to set it.

The chart shows nonmanufacturing import's raw diffusion value plotted against the headline ISM. That chart also shows a disconnect of sorts since if the economy is doing well we expect imports to be strong. What we see in the chart and confirmed in the table is that imports are not as strong as the headline and in fact are quite a bit weaker. Maybe nonmanufacturing imports are not the best barometer of the strength of the U.S. economy. But this is another gap in the credibility of this report. Yet, another gap is the difference in the readings for nonmanufacturing ISM from the services reading in Markit's survey for the U.S. The ISM is signaling something and I think it is telling us that the recovery is spreading more broadly. We already know that this early phase of recovery was centered on cities and that a lot of more rural America has been left on the side lines. So there is plenty of opportunity for a broadening to set it.

This nonmanufacturing ISM leaves us with a better feeling about the economy than do reports that are of an accounting nature, adding up output or job creation. The two concepts of breadth and strength are not the same and they appear to be decoupling. The best example is the comparison of jobs gains this month with the ISM employment component. Even with upward hurricane distortions the ranking this month's nonmanufacturing sector job gain is lower than the employment ranking in the nonmanufacturing survey itself over the same time period. We do have some disconnect here.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief