Global| Oct 29 2008

Global| Oct 29 2008U.S. Durable Goods Orders Ticked Up

by:Tom Moeller

|in:Economy in Brief

Summary

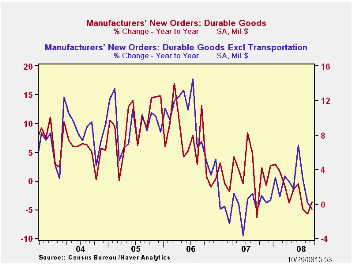

During September, new orders for durable goods ticked up 0.8% after falling 5.5% during August, a decline revised from the -4.5% figure reported initially. Though the September rise in orders beat Consensus expectations for a 1.0% [...]

During September, new orders for durable goods ticked up 0.8% after falling 5.5% during August, a decline revised from the -4.5% figure reported initially. Though the September rise in orders beat Consensus expectations for a 1.0% decline, there where few, if any, areas of strength. The gain mostly reflected a 21.8% (-16.6% y/y) jump in new orders for aircraft & parts that offset most of a decline during August. (Nondefense aircraft orders rose 29.7% (-34.1% y/y).

Highlighting the weakness in durable goods orders last month was a 1.1% decline in new orders less the transportation sector altogether. That followed a 4.1% drop during August, initially reported at down 3.0%. The September decline about matched Consensus expectations but during the last three months, orders less the transportation sector fell at a 19.0% annual rate.

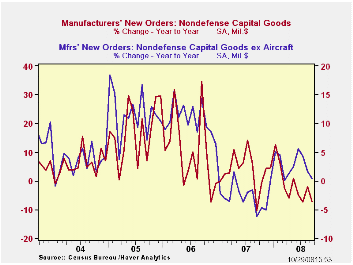

The rise in aircraft orders did lift overall orders for nondefense capital goods by 0.8%, but that followed a little-revised 7.7% plunge during August. Without aircraft, nondefense capital goods orders fell 1.4% after 2.2% drop during August. These declines lowered the three-month growth rate to -12.4%, the worst since early last year. During the last ten years there has been an 80% correlation between the y/y gain in nondefense capital goods orders and the rise in equipment & software spending in the GDP accounts. The correlation of the GDP figure with capital goods shipments is, as one would expect, a larger 92%.

The industry detail highlights the recent weakness in factory

orders. Orders for machinery ticked up just 0.5% after a 6.4% drop

during August. That left the three-month growth rate at -9.5%.Primary

metals orders fell sharply for the second consecutive month with a 4.5%

(+1.6% y/y) drop which followed a downwardly revised 12.5% August

plunge. New orders for electrical equipment increased 1.5% (1.1% y/y)

after a 3.5% August decline. On a three-month basis these orders were

down at a 35.0% annual rate.

New orders for computers & electronic products continued on their weaker trend-line with a 1.4% drop last month. On a three-month basis these orders fell at a 15.0% annual rate after their 2.1% decline during all of last year. Orders for just computers & related products fell 2.8% and on a three-month basis they were off at a 47.9% annual rate. New orders for communications equipment also have been quite weak and they fell 14.6% last month. Three-month growth was -36.6% (AR) after last year's 7.5% decline.

Reflecting past weakness in new orders was a 0.2% rise in overall shipments of durable goods which made up little of a 4.2% August fall. During the last three months growth was a negative 7.6% (AR) after last year's negligible 0.1% uptick. For comparison, industrial production of durable goods during the last three months fell at a 13.5%. During the last ten years there has been a 62% correlation between the three-month change in shipments of durable goods and the change in durables industrial production. Less transportation, shipments of durable goods fell 0.4% following a 2.9% August drop. Three-month growth fell to -4.8% (AR).

Inventories of durable goods rose just 0.4% (8.1% y/y), the weakest monthly increase since last October. Three-month growth eased slightly to a still strong 8.8%. Less transportation, inventories rose a weaker 0.5% and the three-month growth rate eased slightly to 9.4% (AR) after the 1.4% rise during 2007.

Addressing the Credit Crisis is a speech given earlier this month by Dallas Fed President Richard W. Fisher and it can be found here.

| NAICS Classification (%) | September | August | Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| Durable Goods Orders | 0.8 | -5.5 | -3.6 | 1.4 | 6.2 | 10.2 |

| Excluding Transportation | -1.1 | -4.1 | -0.6 | -0.3 | 9.1 | 9.1 |

| Nondefense Capital Goods | 0.8 | -7.7 | -7.2 | 3.5 | 9.4 | 17.3 |

| Excluding Aircraft | -1.4 | -2.2 | 0.5 | -2.7 | 10.7 | 11.6 |

by Tom Moeller October 29, 2008

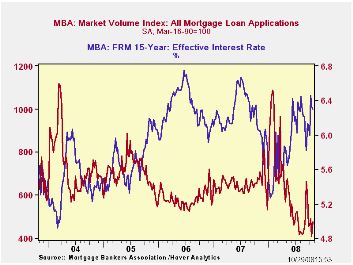

The total number of mortgage applications rose 28.5% last week and that recovered all of the prior period's decline, according to the Mortgage Bankers Association. Nevertheless, the October average fell 20.0% from September and applications were two-thirds below their peak reached this past January.

Last week, applications for a mortgage to purchase a home made up most of the prior week's decline with an 8.5% rise. For October so far, however, purchase applications reversed most of the prior month's gain with a 13.3% decline. During the latest week purchase applications were down 43% from their 2005 peak.

During the last ten years there has been a 61% correlation between the y/y change in purchase applications and the change in new plus existing single family home sales. Figures covering sales of existing single-family home will be available this Friday while single-family home sales will be published early next week.

Applications to refinance a home mortgage recovered most of

the prior week's decline with a 28.5% increase but applications in

October overall remained 20% below September. During September,

applications to refinance had risen 61.9% from August as 15-year

mortgage rates fell briefly to 5.54%.

The effective interest rate on a conventional 15-year mortgage slipped last week to 6.30% following an average of 6.01% last month. For a 30-year mortgage, rates slipped w/w to 6.48%. Interest rates on 15 and 30 year mortgages are closely correlated (>90%) with the rate on 10-year Treasury securities. For an adjustable rate 1-Year mortgage the rate also slipped w/w to 6.95% after having averaged 6.70% last month.

During the last ten years there has been a (negative) 79% correlation between the level of applications for purchase and the effective interest rate on a 30-year mortgage.

The Mortgage Bankers Association surveys between 20 to 35 of the top lenders in the U.S. housing industry to derive its refinance, purchase and market indexes. The weekly survey covers roughly 50% of all U.S. residential mortgage applications processed each week by mortgage banks, commercial banks and thrifts. Visit the Mortgage Bankers Association site here.

The figures for weekly mortgage applications are available in Haver's SURVEYW database.

| MBA Mortgage Applications (3/16/90=100) | 10/24/08 | 10/17/08 | Y/Y | 2007 | 2006 | 2005 |

|---|---|---|---|---|---|---|

| Total Market Index | 476.7 | 408.1 | -30.1% | 652.6 | 584.2 | 708.6 |

| Purchase | 303.1 | 279.3 | -26.6% | 424.9 | 406.9 | 470.9 |

| Refinancing | 1,489.4 | 1,158.8 | -33.8% | 1,997.9 | 1,634.0 | 2,092.3 |

by Tom Moeller October 29, 2008

The Federal Open Market Committee today cut the Federal funds rate, as expected, to 1.00% from 1.50%. The discount rate also was cut to 1.25%. The latest Fed funds rate was its lowest since 2004.

The Fed indicated three specific reasons for lowering interest rates today. 1) A slowdown in U.S. economic growth due to slower consumer spending and weaker business investment spending 2) Financial market turmoil and 3) an expectation for moderation in inflation due to lower energy and other commodity prices as well as slower economic growth.

Credit market conditions were expected by the Fed to improve

due to interest rate cuts around the world, "extraordinary liquidity

measures" and actions to strengthen financial systems.

The decision was unanimous amongst FOMC voters.

For the complete text of the Fed's latest press release please follow this link.

How Economic News Moves Markets from the

Federal Reserve Bank of New York can be found here.

| Current | Last | September | 2007 | 2006 | 2005 | |

|---|---|---|---|---|---|---|

| Federal Funds Rate, % (Target) | 1.00 | 1.50 | 2.00 | 5.05 | 4.96 | 3.19 |

| Discount Rate, % | 1.25 | 1.75 | 2.25 | 5.86 | 5.96 | 4.19 |

by Robert Brusca October 29, 2008

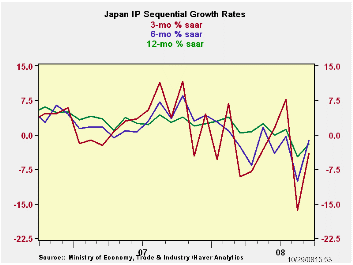

Japan’s IP fell sharply by 3.5% in August, but it has made a substantial rebound in September. Still the trends for IP all are lower, as the sequential growth rates in the table below show. The rebounds by sector in September are only about one-third of the drop made in August.

Year-over-year, Japan’s IP is still rising at a 2.7% pace. Consumer goods output is up by a strong 3.9% while investment goods output is up by 0.5% at an annual rate. The investment goods side is slowing down faster than the consumer goods side.

That trend is in place for the quarter as well. With the September figures just in to complete the quarter, Q3 reveals that overall IP is falling at a 5% pace in MFG. Investment goods output is dropping at a sizeable 13.2% pace while the output of consumer goods is still up at a 4.1% pace. Since consumers are showing weakness around the world in terms of lower confidence and reduced spending and since Japan is a strong exporter of consumer goods this sector is due to get hit much harder.

| Japan Industrial Production Trends | ||||||||

|---|---|---|---|---|---|---|---|---|

| m/m % | Saar % | Yr/Yr | Qtr-to-Date | |||||

| seas adjusted | Sep-08 | Aug-08 | Jul-08 | 3-mo | 6-mo | 12-mo | Yr-Ago | % AR |

| Mining & Mfg | 1.2% | -3.5% | 1.3% | -4.1% | -1.3% | -1.9% | 2.7% | -4.8% |

| Total Industry | 1.1% | -3.6% | 1.5% | -4.1% | -1.3% | -2.1% | 3.0% | -4.5% |

| MFG | 1.1% | -3.5% | 1.2% | -4.8% | -1.7% | -2.1% | 2.8% | -5.0% |

| Textiles | -1.4% | -0.2% | -2.9% | -16.6% | -13.7% | -10.6% | -6.8% | -16.2% |

| T-port | 4.4% | -9.8% | 4.0% | -7.9% | -1.2% | -1.3% | 10.4% | -7.4% |

| Product Group | ||||||||

| Consumer Goods | 0.9% | -3.3% | 3.6% | 4.5% | 4.3% | 0.6% | 3.9% | 4.1% |

| Intermediate Goods | 0.5% | -2.3% | -0.2% | -7.8% | -3.6% | -1.8% | 3.4% | -5.6% |

| Investment Goods | 4.7% | -5.2% | -0.5% | -5.1% | -2.4% | -4.9% | 0.5% | -13.2% |

| Mining | -4.4% | 1.6% | 4.2% | 4.7% | 2.5% | -1.4% | 1.8% | 12.4% |

| Electricity & Gas | 2.0% | -7.6% | 6.3% | 0.4% | -0.8% | -3.9% | 8.8% | -1.8% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief