Global| Apr 24 2007

Global| Apr 24 2007U.S. Consumer Confidence, Present Situation Drop Off Peak

Summary

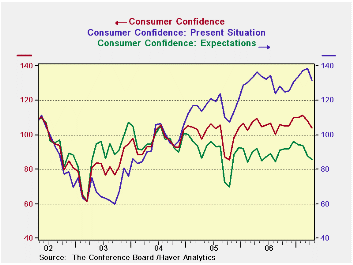

The story of consumer confidence is that the index is now just one month off its peak reading for this expansion cyclenot exactly the kind of thing to get worried about. The present situation sub-index is also one-month off its peak [...]

The story of consumer confidence is that the index is now just one month off its peak reading for this expansion cycle—not exactly the kind of thing to get worried about. The present situation sub-index is also one-month off its peak of the cycle. The expectations sub-index is sliding more persistently. That index reached its peak back in late 2003. Weakness in this series as the expansion grinds on is to be expected. Sharp drops in expectations are to be worried about. What we have here is a steady erosion in expectations.

The table below presents the various components of the present situation and expectations indexess showing them as DIFFUSION values. Present situation readings for businesses and for employment are solid with diffusion readings at 55.8 for business and 53.7 for employment. For expectations things get a bit more frayed. Business conditions are still expected to be positive as the diffusion reading for 6-months ahead is 51.7. The employment outlook, however, is a contractionary 48.6. Income expectations at 54.1 are still solid. However, in looking at the responses we find that the prevalent expectation is for NO CHANGE. Since late 2003 we have the greatest number of respondents saying ‘no change’ for business conditions that we have seen in this period. For employment and income expectations we are also looking at near record ‘no change’ readings for the period. Economic agents seem to be confused about what to expect.

Buying plans are weak. Although plans to buy a new car are still above what has been normal. Plans to buy a house are very low. I’m just guessing here but I’ll bet that plans to buy a new home with a sub-prime mortgage are even lower…

| Raw Indices | Apr-07 | Mar-07 | Feb-07 | Jan-07 | Dec-06 | Nov-06 | Oct-06 |

| Confidence Index | 104.0 | 108.2 | 111.2 | 110.2 | 110.0 | 105.3 | 105.1 |

| Present Situation: | 131.3 | 138.5 | 137.1 | 133.9 | 130.5 | 125.4 | 125.1 |

| Expectations | 85.8 | 87.9 | 93.8 | 94.4 | 96.3 | 91.9 | 91.9 |

| Present Situation Responses: Diffusion Indices | |||||||

| Business Conditions | 55.8 | 57.1 | 57.0 | 55.9 | 56.3 | 55.7 | 55.6 |

| Employment | 53.7 | 55.7 | 55.0 | 55.0 | 53.2 | 51.8 | 51.9 |

| Expectations(6-mo): Diffusion Indices | |||||||

| Business Conditions | 51.7 | 52.4 | 53.9 | 54.2 | 54.5 | 53.8 | 54.3 |

| Employment | 48.6 | 48.4 | 49.6 | 49.1 | 49.2 | 48.6 | 48.6 |

| Income | 54.1 | 55.0 | 55.5 | 56.2 | 57.1 | 56.5 | 55.8 |

| Buying Plans: Raw Responses and Weighted Indices | |||||||

| Automobile | Apr-07 | Mar-07 | Feb-07 | Jan-07 | Dec-06 | Nov-06 | Oct-06 |

| Yes: Auto | 6 | 5.4 | 5.5 | 6.3 | 5.4 | 5.2 | 6.2 |

| New: Auto | 3.2 | 2.7 | 2.4 | 3 | 2.6 | 2.3 | 2.9 |

| House | Apr-07 | Mar-07 | Feb-07 | Jan-07 | Dec-06 | Nov-06 | Oct-06 |

| Yes: House | 2.7 | 3.2 | 3.4 | 3.3 | 2.9 | 3.2 | 3.1 |

| New: House | 0.7 | 0.8 | 1.1 | 1.2 | 0.5 | 1.1 | 0.6 |

| Major Appliance | 30.3 | 32.7 | 32.1 | 29.6 | 27.8 | 29.8 | 28.5 |

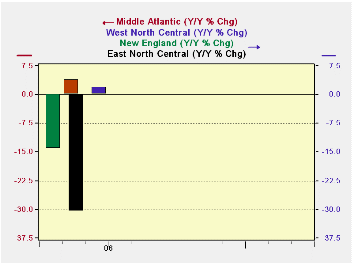

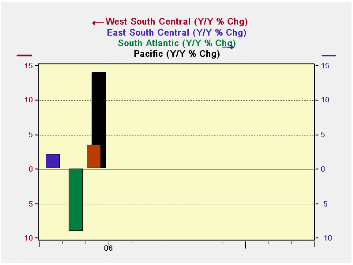

Current conditions are very erratic across the country. The charts below the spotty and irregular performance in Yr/Yr current conditions across regions. Only three are lower Yr/Yr but the E. North Central region is down hard and both the New England and South Atlantic regions are off significantly. On the upside the Pacific region is up strongly but most of the other regions are up only modestly.

Placed in the perspective of the recent economic recovery since late 2003, the NE Central is not just weak but on a new low for this part of the cycle while its current conditions reading stands only in its 12th percentile, the bottom 12% of all readings. Generally the regions out West are going better.

| · On balance, we find there is still exists a lot of uneven conditions around the nation. This month, consumer confidence and the present situation eroded in each major region month to month except for a sizeable increase in the present conditions index in the Pacific region. While the overall index of consumer confidence is not far off peak we must wonder if this sort of broad-based weakness is a new feeling of malaise or actual encroaching weakness or simply the result of pretty odd weather/calendar patterns. This is another of the indexes we will want to keep close tabs on (actually the whole family of consumer attitude indexes). There is no sense of there being any fluke in this survey since both the weekly ABC/Washington Post index and the monthly U of M index of consumer sentiment have been weakening. In this month’s report we also saw inflation expectations rise. · It was not an upbeat report for April. But then again, based on where the various indexes stand in historic context, it was not too bad either. It’s about the way things have been going. There is no evidence of a break out here in either direction. |

|---|

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief