Global| Sep 01 2017

Global| Sep 01 2017U.S. Construction Spending Erodes in July

Summary

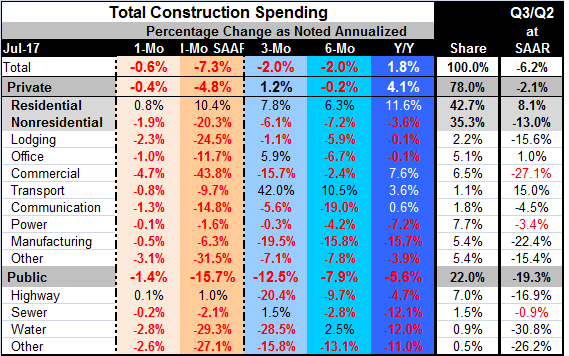

Construction spending fell 0.6% in July with private spending falling 0.4% and public spending dropping 1.4%. Within the private sector, residential spending continued to expand, gaining 0.8% in the month while nonresidential spending [...]

Construction spending fell 0.6% in July with private spending falling 0.4% and public spending dropping 1.4%. Within the private sector, residential spending continued to expand, gaining 0.8% in the month while nonresidential spending fell 1.9%.

Construction spending fell 0.6% in July with private spending falling 0.4% and public spending dropping 1.4%. Within the private sector, residential spending continued to expand, gaining 0.8% in the month while nonresidential spending fell 1.9%.

Trends are depicted by the sequential growth rates in the table from year/year to six-month to three-month. On that timeline, overall construction spending decelerated from a 1.8% pace over 12 months to contract at a 2% pace over six months and it continued to contract at a 2% pace over three months. Private spending grew over 12 months, declined over six months and advanced again over three months ending this phase with a weak 1.2% rate of growth over three months.

Within private spending, residential trends remain positive. Spending growth is at an 11.6% pace over 12 months then cools to a 6.3% pace over six months and remains in the lower trajectory with a 7.8% pace over three months.

Conversely, private nonresidential spending is simply contracting at different speeds. The pace of contraction is -3.6% over 12 months, but that steps up to -7.2% over six months and stays at -6.1% over three months. The nonresidential sector is still stressed.

Public trends are declining at a 5.6% pace over 12 months and that contraction simply intensifies over six months and intensifies further over three months as spending falls at a 12.5% annualized pace over three months.

Despite low mortgage rates and a mature economic expansion with a still-growing economy, the construction sector is challenged. The residential market is holding up the best as low mortgage rates underpin it and have kept homes affordable despite a run-up in prices. House prices, in fact, continue to rise nationally; some very expensive local markets having been created.

We are only one month into Q3 with this report, but the level of spending in July relative to the Q2 average shows spending is declining at a 6.2% pace in the new quarter as residential spending continues to grow and continues to be swamped by larger negative effects in the nonresidential sector. Public spending is falling very rapidly at a 19% annual rate as the fiscal situation in Washington has put all nonessential Federal spending on hold.

In the wake of the day's multiple reports, including the employment report, the manufacturing ISM and construction spending, the Atlanta Fed has trimmed its GDP-Now estimate for Q3 growth to 3.2% from 3.3%. The estimate which started out at a 4% pace continues to be trimmed bit by bit as new data roll in.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief