Asia| Oct 27 2025

Asia| Oct 27 2025Economic Letter from Asia: To the Summit!

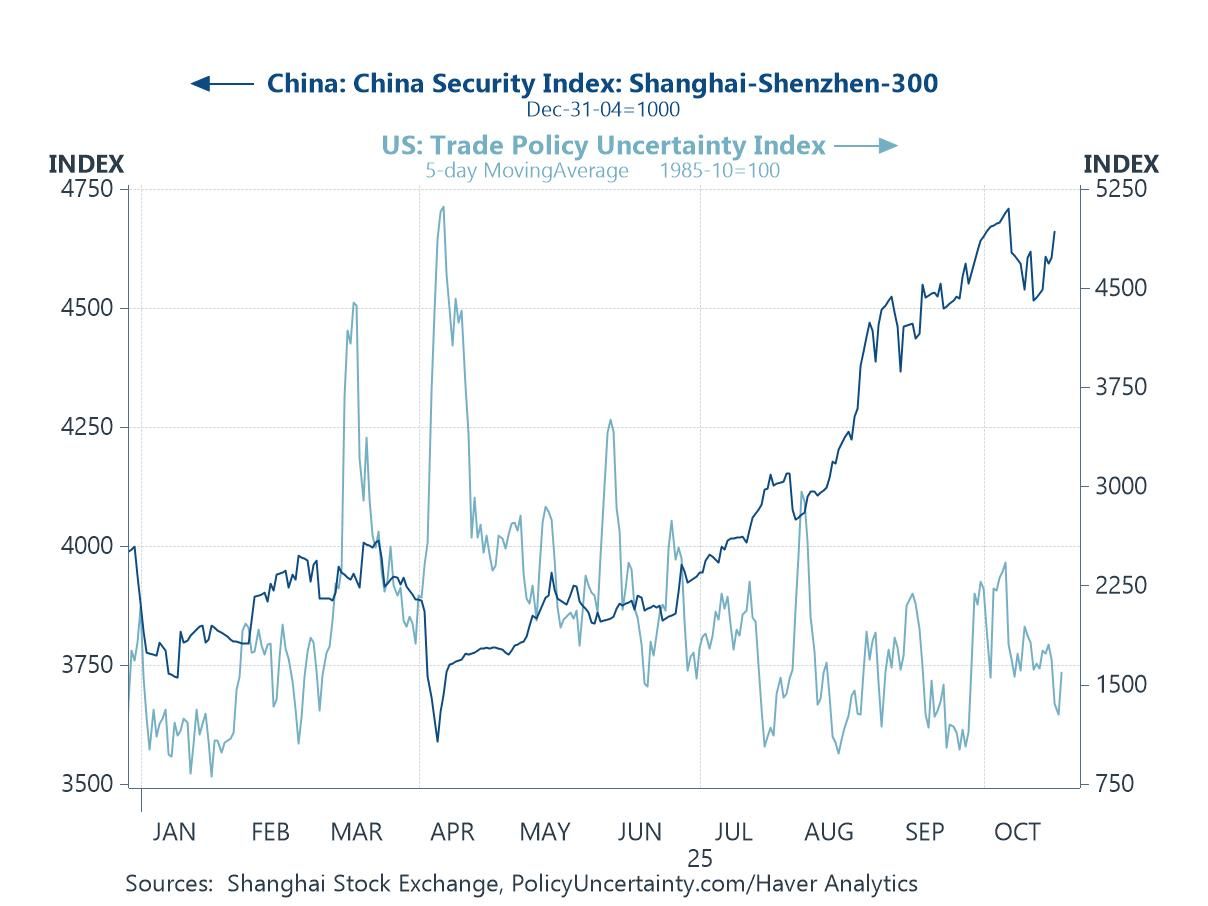

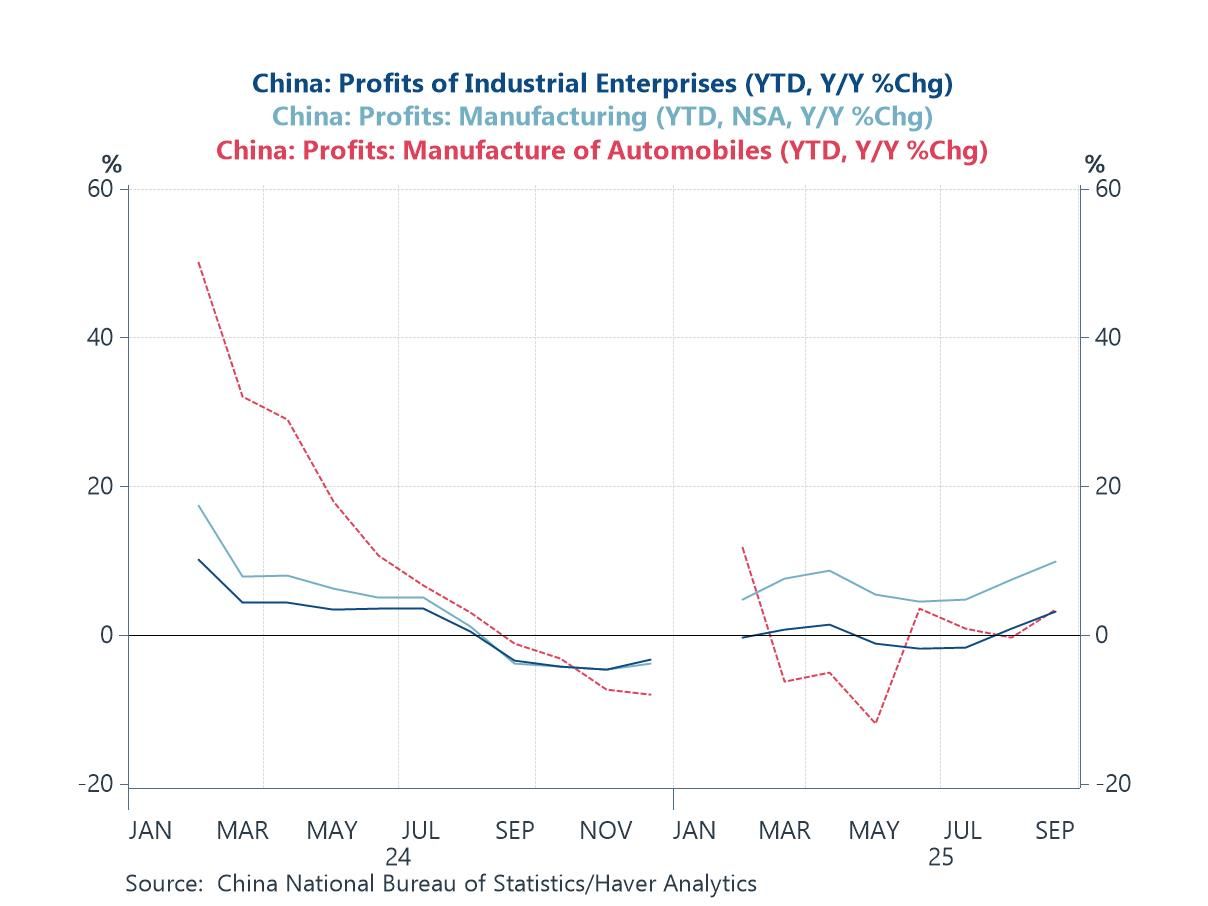

This week, attention remains on developments in Asia as US President Trump continues his regional tour. Over the weekend, his visit to Malaysia for the ASEAN–US summit saw a peace deal secured between Thailand and Cambodia, along with several trade agreements with ASEAN economies. Focus now shifts to Trump’s upcoming interactions with Japan’s new Prime Minister Takaichi and China’s President Xi in Japan and South Korea, respectively. A US–China trade deal is highly anticipated, which, if achieved, could boost market sentiment and reduce uncertainty (chart 1). Leading up to these meetings, encouraging Chinese data has emerged, including a significant improvement in industrial profits, suggesting that efforts to curb race-to-the-bottom price competition are beginning to show results (chart 2).

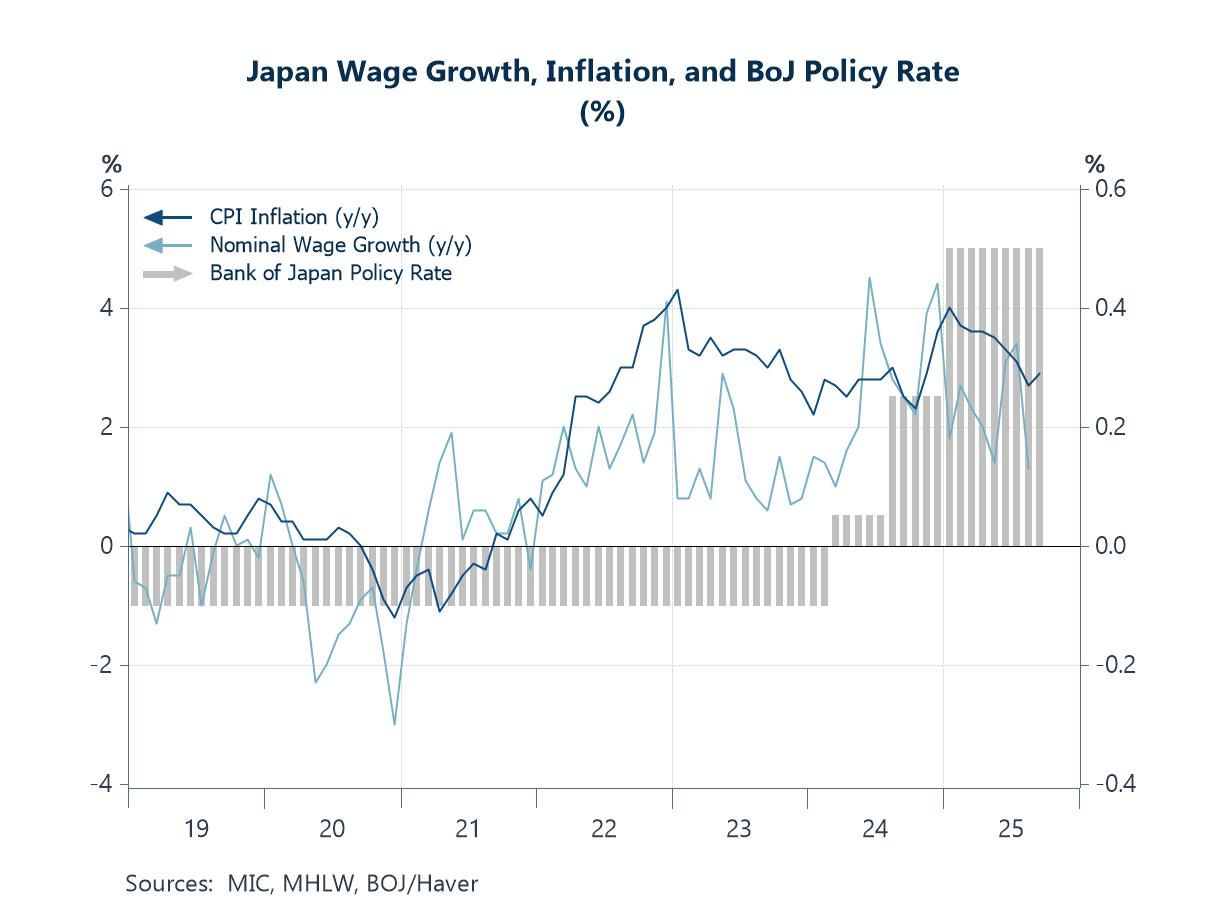

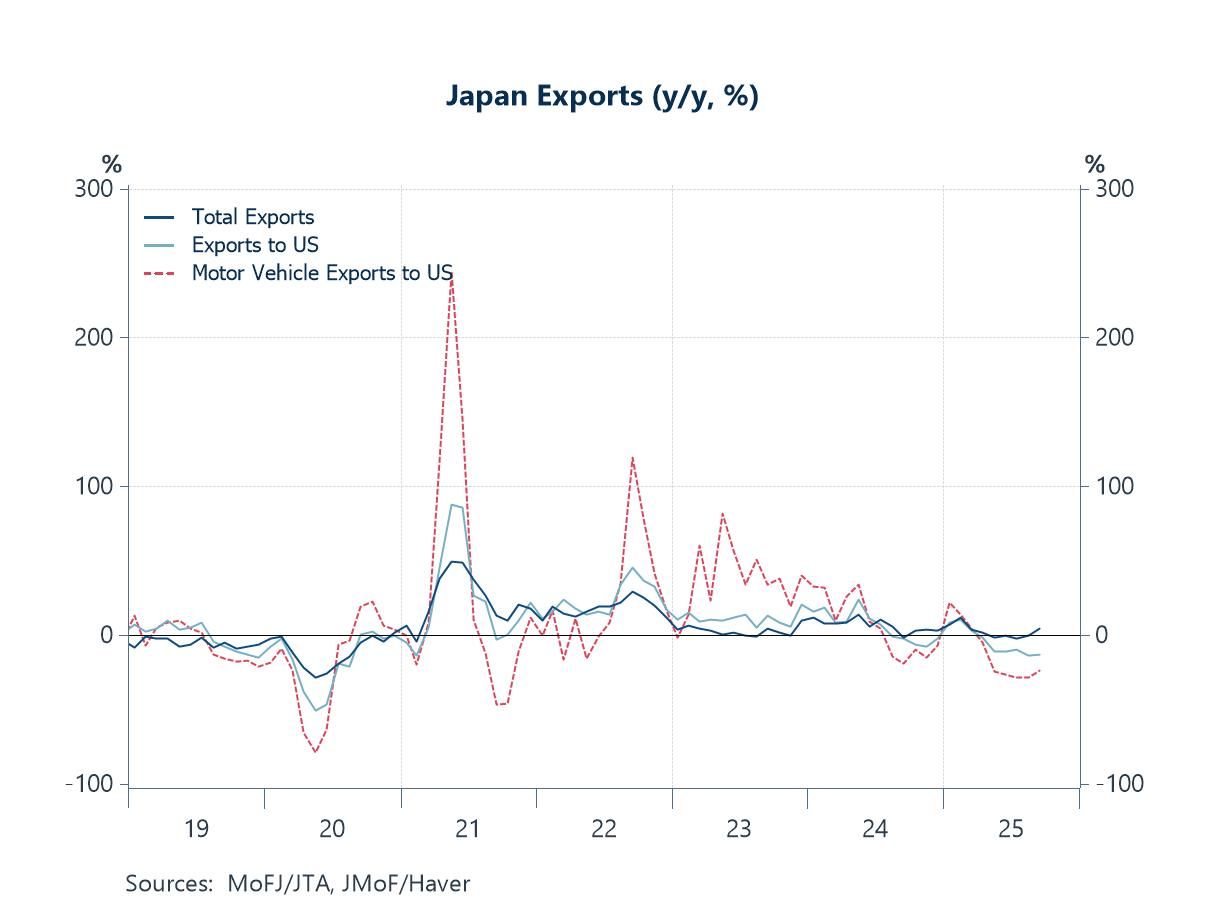

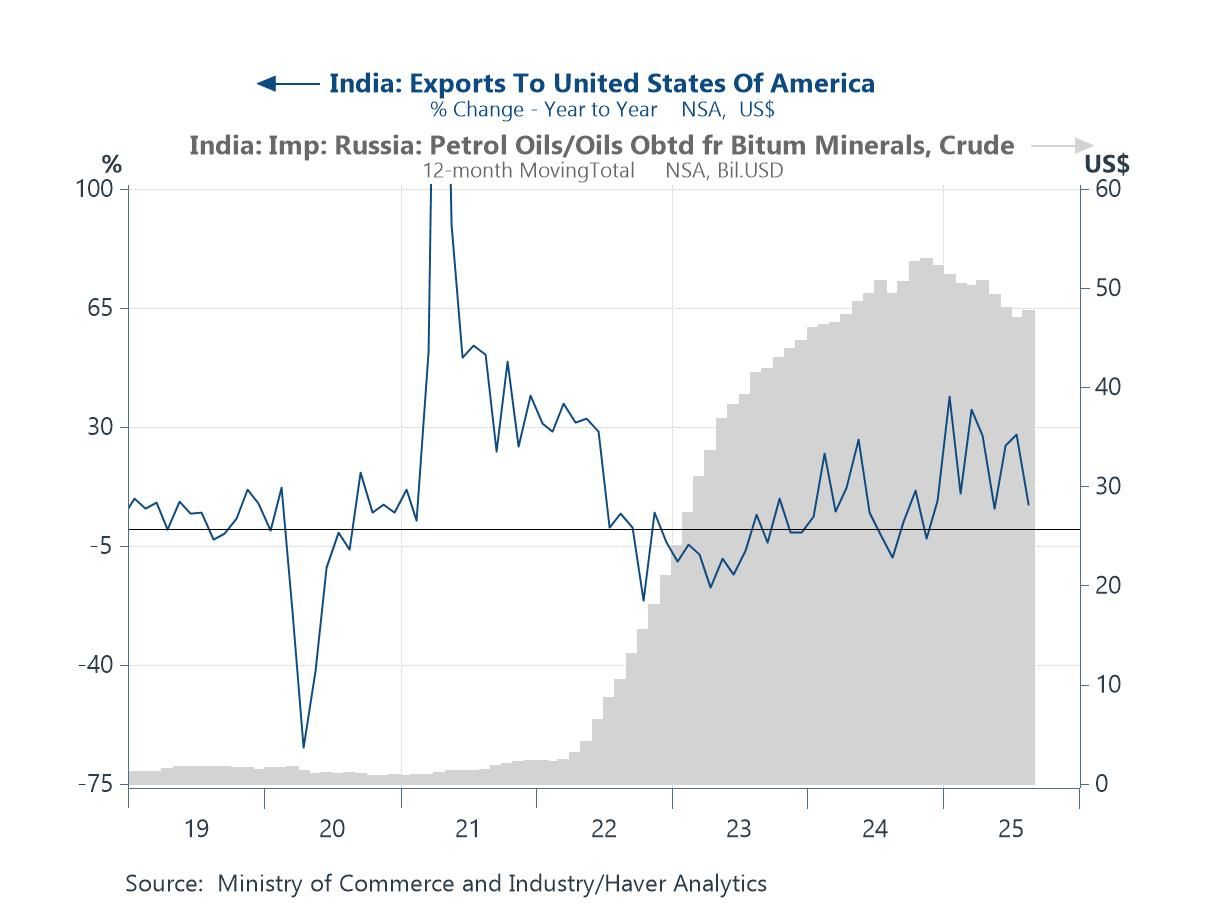

In Japan, apart from the Trump–Takaichi meeting, markets will closely watch the Bank of Japan’s October monetary policy decision (chart 3). While no change in policy rates is expected, the Bank’s updated forecasts will be scrutinized. Japan’s September trade numbers were encouraging (chart 4), but much depends on the US–Japan trade relationship. Still, Japan’s stronger shipments to other economies, if sustained, could help offset potential US-related headwinds. US–India trade talks also remain in focus, with India reportedly planning to reduce purchases of Russian crude oil—a recurring point of contention (chart 5). At the same time, while India has faced reduced imports from the US due to tariffs, increased shipments to other trading partners, particularly in Asia, highlight a broader trend of trade diversification. Finally, while the ongoing AI boom continues to support exports growth across several Asian economies, the risk of overreliance on semiconductor exports deserves emphasis. Some economies would not have recorded year-to-date export growth without the current AI-driven upcycle (chart 6).

The ASEAN and APEC summits Over the weekend, US President Trump arrived in Kuala Lumpur for the ASEAN–US Summit, where he oversaw the signing of a peace deal between Thailand and Cambodia. He also signed several trade agreements, including commitments by four ASEAN members to remove most—or in some cases all—tariffs on US imports, as well as deals with some members on critical minerals cooperation. While these developments are notable for ASEAN watchers, investor attention now turns to Trump’s next stops in Japan and South Korea. In Japan, focus will be on Prime Minister Takaichi’s first meeting with the US President, while in South Korea, markets will watch whether a long-anticipated US–China trade deal can take shape during the APEC summit. Recent signs of easing tensions—namely the likely suspension of Trump’s 100% tariff threats and China’s possible delay of rare earth export restrictions—could help temper regional uncertainty. This, in turn, may lift market sentiment, marking a welcome reversal from the caution seen in prior weeks (chart 1).

Chart 1: Chinese equities and US trade policy uncertainty

China economic data While awaiting key outcomes on a potential US–China trade deal, the latest Chinese data already show encouraging signs. Industrial profits for September, released earlier today, surged to 3.2% year-to-date y/y, up from August’s 0.9%, marking a continued break from the previous multi-month streak of losses (chart 2). The improvement was supported by accelerating growth in the manufacturing sector, including automobiles, suggesting that authorities’ recent clampdowns on price wars—particularly among carmakers—are beginning to bear fruit. Continued easing of such “race-to-the-bottom” pricing could also help address broader overcapacity issues in China. Looking ahead, investors are now focused on the official PMI readings scheduled for release later this week.

Chart 2: China industrial profits

The Bank of Japan, Japan’s new Prime Minister Turning to Japan, attention will focus this week on the Bank of Japan’s policy decision, with markets widely expecting the central bank to keep its policy rate unchanged. Looking ahead, the path toward additional monetary tightening may become more challenging following the election of Prime Minister Takaichi, whose pro-growth stance favours accommodative policy and a shift toward inflation driven not only by cost-push but also by demand-pull factors, such as stronger wage growth. The Bank’s updated economic forecasts in its Outlook Report will also be closely watched. Beyond monetary policy, investors will look to Takaichi’s first meeting with US President Trump as Japan’s new Prime Minister, which could offer early signals on the tone of the renewed US–Japan relationship. While trade may not dominate this initial engagement, Japan’s pledged USD 550 billion investment in the US—agreed under a previous tariff deal—remains a key uncertainty. Takaichi will need to consider financing this commitment, likely through significant private-sector participation, even as she pursues fiscal expansion to support her pro-growth agenda.

Chart 3: Japan wage growth, inflation, and the BoJ policy rate

Japan trade Touching further on trade, the Japanese economy recorded its first y/y export growth in months, with a 4.2% increase in September. This came despite continued declines in exports to the US, which fell 13.3% y/y—slightly less than August’s 13.7% drop (chart 4). Motor vehicle exports to the US also slowed their pace of decline, though they remained substantial at 24.2%, compared to 28.4% in August. The improvement in Japan’s overall export growth was driven by stronger shipments to other regions, including Europe and parts of Asia. By goods category, the September boost was supported by higher exports of raw materials and mineral fuels. Robust semiconductor demand, mirroring trends seen in other advanced Asian economies, also contributed to the uptick, albeit to a lesser extent. While the September headline export figure is encouraging, Japan is far from out of the woods, as the US-Japan trade relationship may still face renewed discussions, as mentioned earlier.

Chart 4: Japan’s exports

India Turning to India, early estimates for September suggest that exports to the US fell by around 12% y/y. This was the first full month reflecting the impact of the new 50% US tariff on Indian imports, highlighting the sharp initial effects of the higher rate. Given that the US remains India’s largest export destination, the magnitude of this policy shift is particularly significant. A key issue in ongoing US–India trade discussions continues to be India’s purchases of Russian crude oil, which President Trump has repeatedly said India had pledged to halt or substantially reduce. Despite this, India’s overall exports still grew a robust 6.8% y/y, supported by stronger shipments to other major partners such as the UAE, China, the UK, and Germany. This illustrates the dual impact of the US tariffs: while they underscore Washington’s leverage as a critical export market, they also appear to be encouraging a reorientation and diversification of India’s trade flows away from the US.

Chart 5: India exports to the US and imports of Russian crude

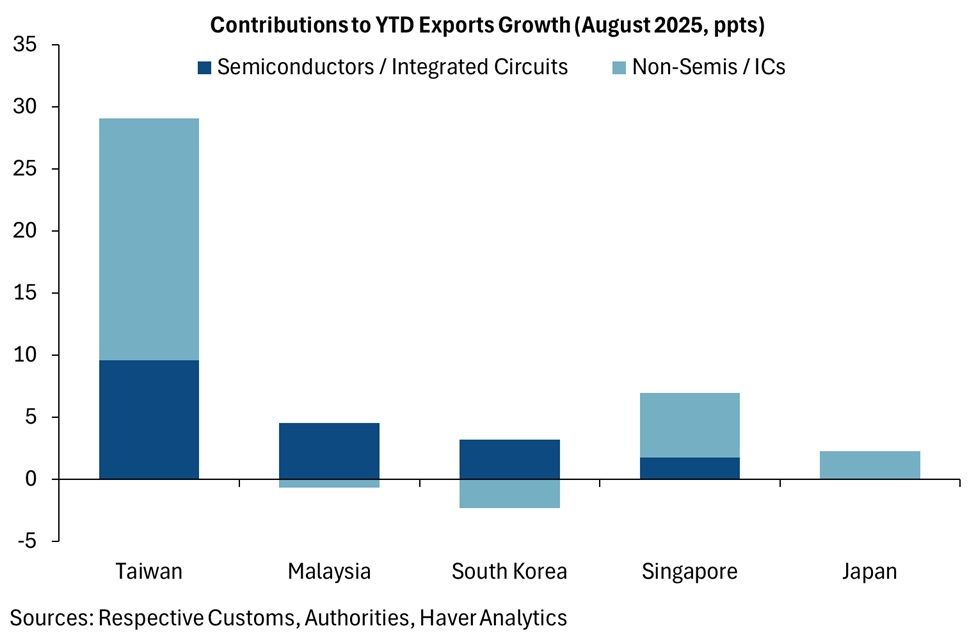

Semiconductors Lastly, on semiconductors, robust AI demand and strong sales have continued to support growth across advanced Asian economies, but caution is warranted. The global trade environment remains fragile, and many of these economies have relied heavily—sometimes almost exclusively—on this sector for export growth. This is particularly evident in Malaysia and South Korea, where year-to-date exports would have declined without the semiconductor boost (chart 6). By contrast, Taiwan, while benefiting significantly from the semiconductor boom, has also gained from a broader electronics upcycle. Japan, too, has seen a semiconductor-driven uplift, but its more diversified export base has supported growth across a wider range of categories. While riding the semiconductor upcycle can bring substantial gains, an overconcentration in the sector—without secondary or tertiary sources of growth—poses a material risk if semiconductor demand were to weaken.

Chart 6: Semiconductor contributions to year-to-date exports growth

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief