Global| Dec 23 2015

Global| Dec 23 2015U.K. Q3 GDP Rise Is Cut to 0.4% from 0.5%

Summary

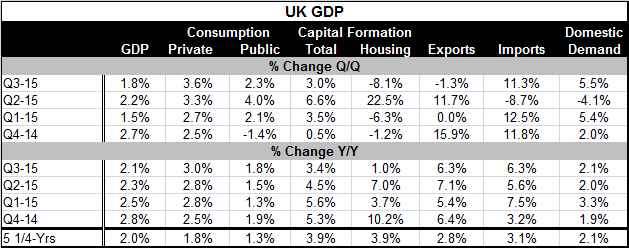

U.K. GDP growth has been cut to 0.4% in Q3 2015 from what had previously been estimated at 0.5%. Growth also is steadily slipping with its annual rate dropping from 2.8% in Q4 2014 to 2.5% in Q1 2015, and to 2.3% in Q2 and now to 2.1% [...]

U.K. GDP growth has been cut to 0.4% in Q3 2015 from what had previously been estimated at 0.5%. Growth also is steadily slipping with its annual rate dropping from 2.8% in Q4 2014 to 2.5% in Q1 2015, and to 2.3% in Q2 and now to 2.1% in Q3 2015. Decaying trends in capital formation are mostly to blame for the growth slowdown. The year-over-year growth in total capital formation has dropped from 5.3% in Q4 2014 to 3.4% in Q3 2015. Housing in particular has slipped from a year-over-year pace of 10.2% in Q4 2014 to a slim 1% pace in Q3 2015.

U.K. GDP growth has been cut to 0.4% in Q3 2015 from what had previously been estimated at 0.5%. Growth also is steadily slipping with its annual rate dropping from 2.8% in Q4 2014 to 2.5% in Q1 2015, and to 2.3% in Q2 and now to 2.1% in Q3 2015. Decaying trends in capital formation are mostly to blame for the growth slowdown. The year-over-year growth in total capital formation has dropped from 5.3% in Q4 2014 to 3.4% in Q3 2015. Housing in particular has slipped from a year-over-year pace of 10.2% in Q4 2014 to a slim 1% pace in Q3 2015.

Private consumption, the bulk of GDP, has sped up slightly from its pace of late-2014 and early-2015 to grow at a year-over-year pace of 3% in Q3 2015. The annualized quarterly growth rates for mid- and late-2015 are even stronger.

As for recent trends in capital formation, there is a lot of variability in both housing and in overall spending, but there is also a tilt to weaker performance.

Exports and imports do not reveal any clear trends. There has been some volatility in both flows, but in Q3 2015, both exports and imports are up by 6.3% year-over-year. Of course, the quarterly data are simply a mess with some extreme volatility in both exports and imports. Imports seem a little better underpinned than exports as there are three of the last four quarters with double digit growth rates with a quarter of extreme weakness sandwiched in between.

The U.K. economy has also been hit by the fallout from the overly strong dollar and weak energy prices. The strong dollar has helped to weaken commodity prices and pressure firms in that industry. The energy sector has been in such turbulence than investment in the sector has been cut sharply.

The Bank of England was on the cusp of following the Fed on path to a rate hike. But the recent weakening in the U.K. economy has stopped that movement flat in its tracks. Of course, the U.K. is also affected by the weakness on the continent. To that extent, the U.K is hoping that the new round of stimulus by the ECB is successful.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief