Global| Apr 08 2016

Global| Apr 08 2016U.K. IP Shows Some Very Weak Trends

Summary

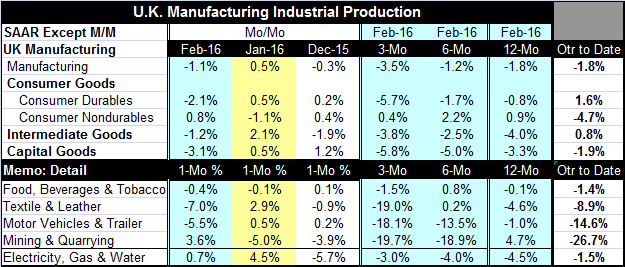

The U.K. shows poor, and many worsening, short-term trends U.K. industrial production fell by 1.1% in February; it is showing sequential declines in output from 12-month to six-month to three-month, but it is not consistently getting [...]

The U.K. shows poor, and many worsening, short-term trends

The U.K. shows poor, and many worsening, short-term trends

U.K. industrial production fell by 1.1% in February; it is showing sequential declines in output from 12-month to six-month to three-month, but it is not consistently getting even worse - that's something. However, consumer durable goods output shows sequential declines and sequential worsening; capital goods output shows sequential declines and sequential worsening. These are two important sectors that are both showing declines and where the declines are worsening. Intermediate goods show output's consistent deterioration but not quite sequential worsening. Only nondurable consumer goods output shows output increasing on all horizons, but the three-month growth rate has snaked down below the 12-month rate which itself is less than 1%. These are not great or reassuring trends for U.K. industry in any sector.

The quarter-to-date shows output is declining

In the quarter-to-date, IP is falling at a 1.8% annualized rate. Nondurable consumer goods output is declining on this horizon at a 4.7% pace and capital goods output is falling at a 1.9% pace. Consumer durable goods output and intermediate goods output each are expanding weakly in the two-thirds-complete quarter.

Year-on-year trends have showed decline for quite some time

U.K. year-on-year IP growth rates have been declining since July 2015 consecutively and declined in 9 of the last 10 months as well. There has been substantial downward pressure on the U.K. manufacturing sector.

Select industry trends are more uniformly poor

The detail on U.K. output by industry is not very reassuring either. Of the five industries listed in the bottom of the table, three show outright declines in February and all of them show output declines over three months and all them show a weaker three-month result than their respective six-month results. However, only motor vehicles and mining show sequential worsening. But all five of these industries show declining output in the quarter-to-date. None of this is reassuring. You can see the impact of weak energy on mining and quarrying where output is still falling at a 26.7% annualized rate in the quarter-to-date. The energy sector hit is still going full throttle in Q1.

Other risks

In addition to all this, there are concerns about Brexit. And David Cameron has been embroiled in the Panama Papers imbroglio as his father's name (a trust he says) is linked to some offshore accounts.

BOE: neutral on Brexit

Meanwhile the Bank of England has warned of the possibility of distress if Brexit should occur. The BOE has taken no official position on the pro-vs-con vote. But Governor Carney made it clear that he thought that including the U.K. in the arrangement had helped the U.K. become more competitive. It was a sort of sneaky way to register a personal opinion then to declare the bank's official view as neutral.

Summing up

On balance, U.K industrial trends are negative. This is in keeping with the global economy where many industrial trends continue to show the sector under pressure. The U.K. trade data for February, also released today, show positive three-month export growth although they reveal declining exports over 12 months. Imports suggest that domestic demand is still in gear as they are rising at a robust 7% annual rate pace over three months but are up by just 2% year-on-year. U.K. vehicle imports continue to be strong and overall imports show life. But the output side of the U.K. economy seems to be considerably weaker and that could become source of vulnerability. The U.K. shares inflation trends with Europe with very weak year-on-year consumer prices and sharply falling producer prices. Inflation is still not in gear and well below the Bank of England's target rate.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief