Global| Aug 09 2019

Global| Aug 09 2019U.K. GDP Contracts as Brexit Beckons

Summary

As the date for Brexit approaches, the impact from the collision has preceded its arrival! GDP, unexpectedly, has fallen in Q2. Newly minted PM Boris Johnson has said that preparing for a hard Brexit is his top priority. Preparation [...]

As the date for Brexit approaches, the impact from the collision has preceded its arrival! GDP, unexpectedly, has fallen in Q2. Newly minted PM Boris Johnson has said that preparing for a hard Brexit is his top priority. Preparation is important. But the event will be nonetheless difficult. It is called ‘hard Brexit’ for a reason.

As the date for Brexit approaches, the impact from the collision has preceded its arrival! GDP, unexpectedly, has fallen in Q2. Newly minted PM Boris Johnson has said that preparing for a hard Brexit is his top priority. Preparation is important. But the event will be nonetheless difficult. It is called ‘hard Brexit’ for a reason.

Already trade patterns are shifting. The U.S. has just overtaken Germany as the country from which the U.K. attracts the most imports. Brexit is in train, change is in the air and flux is the new normal for the U.K. economy. The chart sketches a clear longer-term slowing growth rate for the U.K. economy.

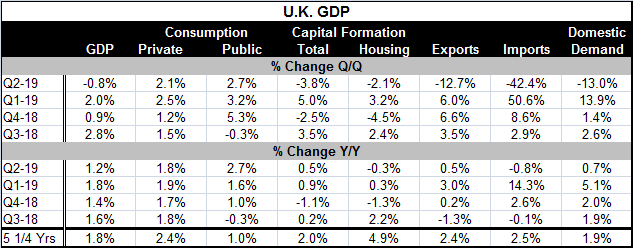

Capital formation has been hit hard. And that is probably the most understandable of all results. The uncertainty about Brexit, its timing, and what the new rules will be, have left businesses handcuffed unwilling to commit new funds for a future they cannot yet grasp. Capital spending fell at a 3.8% annualized rate in Q2 compared to Q1. Year-on-year capital spending is at a 0.5% annual rate.

Housing also contracted in Q2. Weakness in the housing sector has been in train for a while. Real spending on housing is down by 0.3% year-on-year as well as being weak in the quarter and falling at a 2.1% annualized pace.

However, it is exports and imports and domestic demand that are being clobbered in this quarterly report. Some of this is the result of leads and lags behavior as importers and exporters have tried to anticipate the actual occurrence of Brexit and take special action to push exports out or to compile a larger stock of goods beyond what is normally imported to deal with potential deadline and transition issues.

Imports are falling at a 42.4% annual rate in Q2, but only after rising at a 50.6% annual rate the previous quarter. Year-on year-imports are falling at a much milder -0.8% pace.

Exports fall at a 12.7% annual rate in Q2 after logging two quarters of growth at a 6% pace. Exports are creeping along at a 0.5% annual rate over four quarters.

Domestic demand that ramped up at a 13.9% annual rate in Q1 has reversed to fall at a 13% pace in Q2. They will eventually fall into a more stable path as post Brexit circumstances become clear. At that point, businesses will be able to resume investing knowing what the future will require of them. The U.K. and the U.S. already are talking about the sort of new trade deal they will be able to establish once the U.K. exits the EU arrangement. Certainty always trumps uncertainty even if it is a certainty that has costs associated with it. Once the future is known, it can be prepared for and people can learn to live with new circumstances and prosper in them. The U.K. is still waiting for that transition to be made. And if it is a hard Brexit, there will probably be a further period of waiting for clarification as the actual demands of that future will probably involve some ‘making it up as you go along.’

Sterling is under pressure again reaching a fresh two-year low. The decline in GDP was a sucker punch. But in retrospect, it should not have been so unanticipated. Certainly some of the excesses of the previous quarter were due to unwind. And maybe they unwound a quarter sooner than expected. The Game of Thrones is over. It may not be winter that is coming. But it is Brexit and it will bring a chill of its own. Meanwhile, Boris Johns seems to have chosen to play a game of chicken with the EU even though the EU holds all the cards in this game. We will soon see if Boris Johnson has a plan or just a political death-wish.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief