Global| Aug 17 2016

Global| Aug 17 2016'The World' According to ZEW Experts

Summary

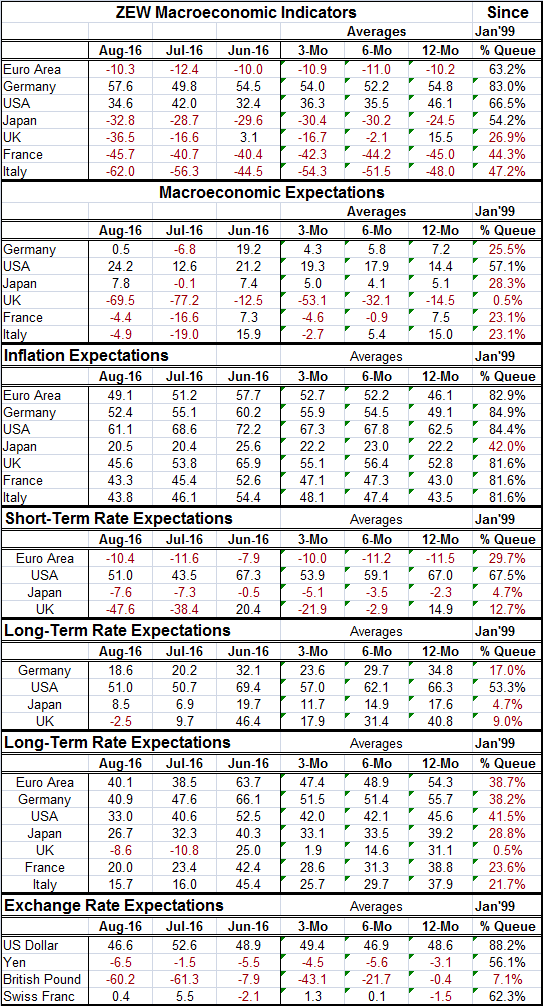

The table and chart array data on the beliefs and expectations of the financial experts in the monthly German ZEW Survey. The experts have a global perspective; as we look at their responses in August, we can get a sense of the sort [...]

The table and chart array data on the beliefs and expectations of the financial experts in the monthly German ZEW Survey. The experts have a global perspective; as we look at their responses in August, we can get a sense of the sort of world environment in which they think we live. The ZEW experts are German and largely have a German view of the world. It may not be exactly the view of the German government or of the Bundesbank, but it is a stylized view by experts immersed in the German economy, steeped in German economic values and trying to understand global events.

The table and chart array data on the beliefs and expectations of the financial experts in the monthly German ZEW Survey. The experts have a global perspective; as we look at their responses in August, we can get a sense of the sort of world environment in which they think we live. The ZEW experts are German and largely have a German view of the world. It may not be exactly the view of the German government or of the Bundesbank, but it is a stylized view by experts immersed in the German economy, steeped in German economic values and trying to understand global events.

While the array of data can be baffling (sometimes `less' is `more'), let's focus our attention on the far right column the queue standings of the ZEW experts making an occasional reference to the data in the table in the left columns. The right hand column is the queue ranking of all responses in each category over a period from January 1999 to date. The rest of the data in the table are net responses (percentage up-minus down expectations multiplied by 100). I keep the percentage signs next to the right hand column data to underscore that the ranking data are intrinsically different from the rest of the data in the table which are net diffusion responses.

To assess conditions, we have three things to look at:

(1) There is momentum. Here we can see if the 12-month to six-month to three-month averages are clearly trending or not. There are also the recent monthly observations (June, July, and August).

(2) There are raw diffusion values in the table whose raw values (positive or negative) also are directional (indicating relatively more positive or negative responses).

(3) There are the queue standings that rank each metric on its raw diffusion score back to 1999.

These schemes give us a number of ways to create context for the ZEW experts' responses in both absolute and relative terms.

Macroeconomic Indicators

In this block, the ZEW experts have weaker than median outlooks for the U.K., France and Italy (each has a queue standing below its respective historic median which occurs at the 50% mark; we calculate these on data back to 1999). Of the seven countries/regions in the top block, all but Germany and the U.S. have negative readings implying deteriorating conditions. The sequential averages over the past year are remarkably stable for each country/region with little change in the ZEW experts' view over the period except for the U.K. where a positive 12-month average has deteriorated to become a significant negative three-month reading and an even weaker monthly reading in the post Brexit environment.

Macroeconomic expectations

Expectations are uniformly weaker than actual performance in terms of their respective queue rankings. In this block, even Germany scores badly (about as badly as the other EMU members in the table and about as badly as Japan) with a 25 percentile standing (weaker only 25% of the time). The U.S. is the lone country with a standing above its historic median with a very moderate 57th percentile reading. In this block, the sequential average shows very slight deterioration in train for Germany, very significant and sharp deterioration for the U.K., and ongoing erosion for France and Italy. The U.S. is gradually gaining momentum here. Despite some strong language from the Bundesbank that has tried to ring fence Brexit off from an impact on ECB policy, there appears to be ongoing deterioration expected in the EMU, at least in the eyes of the ZEW experts. Conditions are weaker in the wake of Brexit than they were before Brexit across the board. `Lo siento mucho Bubacita...'

Inflation expectations

Inflation expectations are a curious block. Despite very moderate economic conditions and eroding expectations, inflation still ranks relatively strongly as a queue standing. The moving average values show that there has been little alteration over the past 12 months in the ZEW experts' views on inflation. Japan continues to be unable to generate any strength in inflation expectations. Yet, ZEW members view that oil remains moderate and have even trended a bit lower in terms of its sequential averages (data not provided).

Short-term rate expectations

Short-term rate expectations are weak everywhere, with an exception; in the U.S. the reading has a top one-third relative standing. The sequential averages do not show much shift at all in the assessment for rates over the past year with two exceptions: (1) in the U.S. the expectation, while staying positive, shows less widespread acceptance, and (2) the U.K. is an exception showing a weakening short-term rate profile.

Long-term rate expectations

Long-term rate expectations are weak with queue standings below their respective medians for all table entries. EMU, Germany and the U.S. have queue standings that are in their respective 40th percentiles compared to standings in the 20th percentile range for Japan, France and Italy. There is a 0.5 percentile standing for the U.K. in the wake of the Brexit vote. There is evidence of some deterioration in this set of responses everywhere as the central bankers' move to negative rate policies was not well anticipated and has had a huge impact, dragging rates down much lower than nearly everyone/everywhere thought. There has been no escape.

Exchange rate expectations

Exchange rate expectations against the euro show a lot of strength expected for the dollar with firmness for the yen and Swiss franc while the pound, which was weak ahead of the Brexit vote, has seen the bottom fall out. Except for the pound, the exchange rate readings have stayed stable.

Summing up and collecting some thoughts

The ZEW experts' view is not encouraging. Their view seems to clash with that of the Bundesbank in so far as there is nothing in this set of assessments that would suggest that the EMU is going to stabilize without more action taken on the policy front. There is a clear correlation of the view for more deterioration to connect with the Brexit vote and events.

Of course, what we can clearly see in the data on Brexit is that these expectations can change in an instant when something significant changes. And in that regard, the ZEW experts see a substantially different world post Brexit than the Bundesbank seems to see. The ZEW experts seem to identify a lot of impact while the Bundesbank wants to dismiss the notion of a different future because markets have stopped reacting to the Brexit vote.

This is not a world environment that is giving Japan much chance to pull itself up by its own bootstraps and to generate any growth or inflation. With such a weak global economy, China's job of reorienting its economy also made that much more difficult.

The policy twist du jour is that U.S. data have begun to show some stronger numbers. Even in the wake of two near 1% GDP growth quarters and with productivity falling for three straight quarters, Fed policy makers may now see enough strength in jobs and in the industrial sector and possibly even in service sector inflation to pull the trigger on a rate hike in September. But all that remains speculative. It is clear, that while you can compile bullish or bearish data on the U.S. economy, you have to put the reports aside to tell a truly bullish or bearish story. The U.S. economy remains mixed with a global environment that is still under a lot of stress if the ZEW experts are anything like right. One can only wonder if the global economy really is safe for a U.S. rate hike or if a rate hike would start a cascade of market selling again as it did at the turn of the year. After all, markets are underpinned by low rates. Once the Fed starts hiking rates, that environment is changed forever. Are the U.S. economy and global markets really ready for a Fed rate hike? That is going to be the next interesting question that markets deal with. How can taking away the markets' key fundamental for strength keep them strong? Riddle me that?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief