Global| Nov 24 2004

Global| Nov 24 2004SUV Demand Drives Up Energy Prices?

Summary

In the five weeks since we have written about the US energy market, prices have eased somewhat. Gasoline, at $2.03/gallon retail in mid-October, has fallen back below $2.00 the past two weeks. Crude oil peaked at $55.23/barrel on [...]

In the five weeks since we have written about the US energy market, prices have eased somewhat. Gasoline, at $2.03/gallon retail in mid-October, has fallen back below $2.00 the past two weeks. Crude oil peaked at $55.23/barrel on October 25, measured by West Texas Intermediate, the US benchmark, and dipped "as low as" $46.12 on November 16. Yesterday, November 23, it had retraced part of the drop, trading at $48.75.

Back in the spring, we wrote about some energy market fundamentals that have contributed to these extraordinary price levels. Over the past 30 years, most energy price spikes have been supply-driven. Oil-producing countries have controlled production in order to push prices higher in the contemporary demand environment. This episode seems different, we noted back in May, in that it looks to be more demand-oriented.

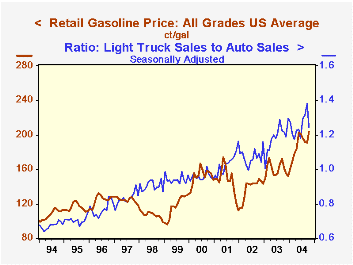

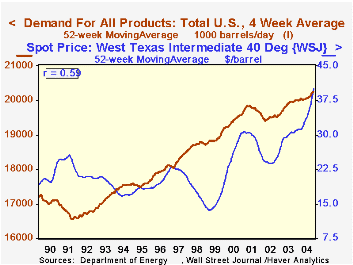

We illustrate this in the current situation with two graphs. In the first, the trend in demand for energy products over the last 15 years is seen to be positively correlated with the trend in crude oil prices. At 59%, the correlation is not numerically exacting, but it shows that demand and prices are moving fairly well in parallel, not in opposite directions that classical supply/demand economics would suggest.

The second graph gives a strong reason for the push in demand and in prices. It highlights the link between light truck sales and gasoline prices. Since the mid-1990s, sales of light trucks, mostly SUVs, have grown both absolutely and in relation to conventional car sales. The resulting ratio of truck to auto sales is seen to have a 75% correlation with retail gasoline prices. This truck/car ratio actually has a 99% correlation with gasoline demand. Thus, the American "love affair" with the large vehicle, which was constrained by the initial energy crisis in the mid-1970s, has returned with the next generation of drivers. Energy prices, moving in more open markets in recent years, have responded to the consequent sharp rise in gasoline consumption. We see in the graph that very recently, the share of truck sales has decreased. If this move becomes a trend, some pressure on the general energy market could be relieved.

| Energy Prices | 11/22/04 | 12/31/03 | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| US Retail Gasoline, Regular ($/Gal.) | $1.948 | $1.48 | 28.8% | $1.56 | $1.35 | $1.42 |

| Domestic Spot Market Price: West Texas Intermediate ($/Barrel) | $48.75 | $32.55 | 64.3% | $32.78 | $31.23 | $19.38 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief