Global| Jul 22 2013

Global| Jul 22 2013Spain's price trends reveal global turbulence

Summary

On the surface Spain's prices appear to be fairly well behaved. In the recession producer prices, import prices and export prices all fell year-over-year. As recovery came, all these prices begin to expand year-over-year and generally [...]

On the surface Spain's prices appear to be fairly well behaved. In the recession producer prices, import prices and export prices all fell year-over-year. As recovery came, all these prices begin to expand year-over-year and generally with a good deal of vigor. That occurred until about the middle of 2012. Since then, prices in Spain have continued to ease their rate of expansion and have been posting extremely week rates of growth. Import prices ratcheted down year-over-year and export import prices both had also posted year-over-year drops and are now closer to posting flat trends.

On the surface Spain's prices appear to be fairly well behaved. In the recession producer prices, import prices and export prices all fell year-over-year. As recovery came, all these prices begin to expand year-over-year and generally with a good deal of vigor. That occurred until about the middle of 2012. Since then, prices in Spain have continued to ease their rate of expansion and have been posting extremely week rates of growth. Import prices ratcheted down year-over-year and export import prices both had also posted year-over-year drops and are now closer to posting flat trends.

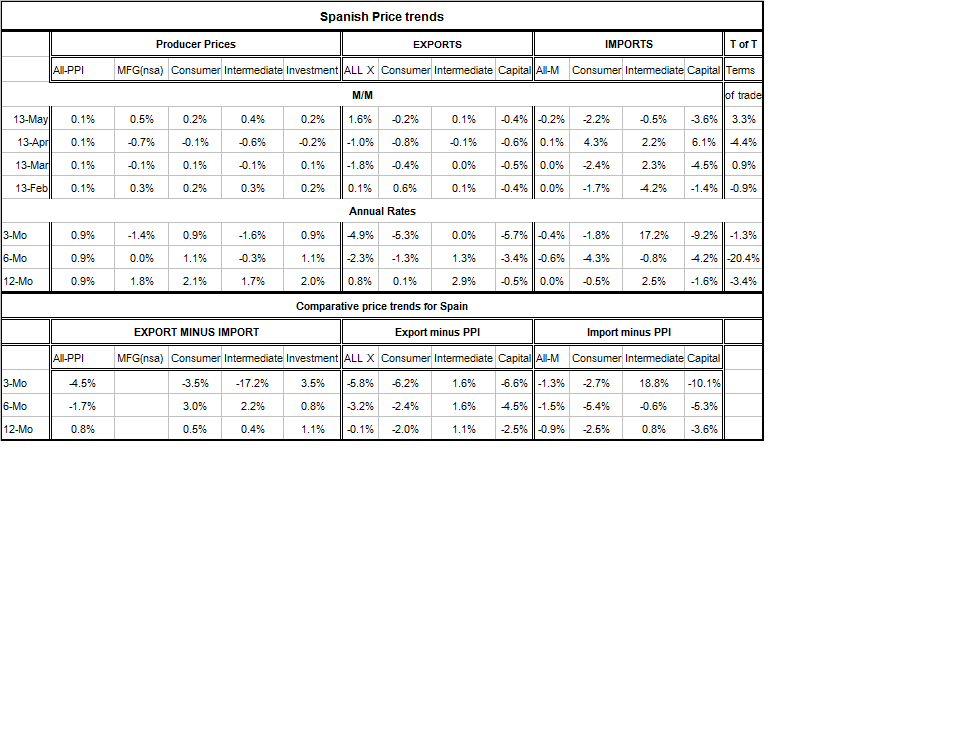

When we dig slightly deeper into the commodity composition of price inflation we see very different things going on at the producer level, at the export level and at the import level for consumer prices, intermediate goods prices, and investment goods or capital goods prices.

We focus on 12-month price trends to simplify the comparisons. PPI prices are rising by 0.8% year-over-year. That's a small increases yet it is faster than for overall export or import prices, both of which are falling on balance over 12-months. Look at individual categories: we find consumer goods import prices are strongest, followed by producer prices and exports. Yet Spain's consumer sector does not seem very strong. Why are its import prices relatively so firm?

Intermediate goods prices are falling for all categories; their strongest result is for producer prices where the decline is only 0.5% over 12 months. For intermediate goods, the weakness grows for export prices and for import prices- the latter are down by 7.8% year-over-year. Lest you think this is being driven by commodity prices, the biggest year-over-year weakness is in imports but it's from capital goods down by 15.3% Year-over-year. By comparison capital goods export prices are down but only by 3.4% year-over-year and domestically investment goods prices are flat over 12 months.

If we look to see where Spain ranks in the Eurozone on inflation performance over the last 12 months it's back in the pack suffering a relatively higher inflation rate than most of the original European monetary union members; its producer price inflation ranks it as the seventh lowest among the original 11 EMU members who have reported figures. Spain is not doing an excellent job on inflation compared to the rest of the Zone. Its producer prices are generally holding up better than either export import prices. This is despite the fact that Spain's economy has been weak, yet the export and import universe appears to be much worse.

With weakness in global demand and rampant conditions of excess supply, it's not so surprising to find weakness in capital goods prices. In Spain's particular business cycle weakness was concentrated in the construction sector. It's not surprising to find capital goods prices are being dragged down by a tremendous oversupply and weakness in Spain's construction sector. Still globally capital goods export and import prices are even weaker than in Spain's domestic market.

Spanish export goods generally are finding world markets weaker than the Spanish markets at home, at least judging from the performance of export prices for goods intermediate goods and capital goods and even for consumer goods.

While the trends for overall export, import and producer prices seem to more or less track together over the cycle, the various sectors are showing very wide differences in performance. And even with Spain as one of the weaker countries in the monetary union, the additional weakness in its export and import prices is not reassuring either for Spain or for the prospects for growth for the rest of EMU.

Since 2001 export prices have risen relative to import prices for each commodity category but the rise has been greatest for intermediate goods where export prices have risen much more than import prices since 1991.

Just today the Bundesbank has issued a warning for a slowdown in the German economy in the second half. The Bundesbank is admitting a pickup in the second quarter but attributing it largely to weather and is seeing further weakness as its view shifts to the third quarter. Germany does depend a lot on capital goods exports and we know it has cultivated Chinese markets. The weakness there may be having blowback effects on Germany and that may be another factor that's been picked up in week Spanish import prices for capital goods.

There are a lot of cross currents in Europe. This analysis of various trends in Spanish prices is a reminder to look deeper into price trends to find out what's really going on rather than to simply rely on headlines to tell the story. The headlines are not telling the story. This is especially true when you look at the headlines being made by our monetary policy makers or our fiscal policymakers or by our international policymakers at the G 20. Be very careful to look at the details because that's where you'll find the real story. The devil is truly in the details.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief