Global| Jul 05 2017

Global| Jul 05 2017Services PMIs Generally Weaken in June; Central Bankers' Policy Quandary Deepens: Do-Do or Don't-Don't?

Summary

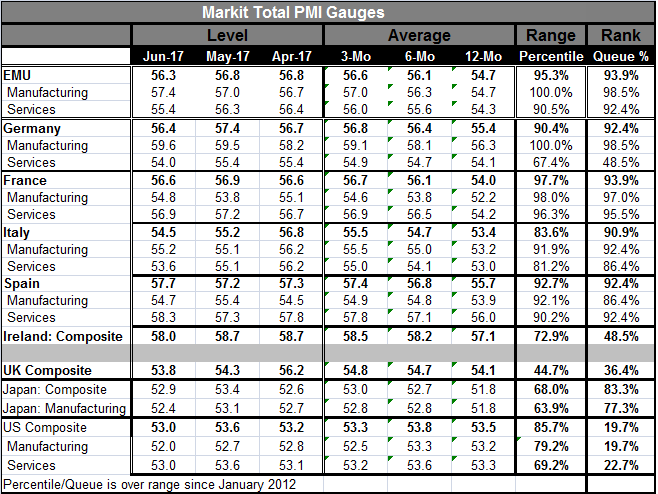

The PMI gauge for Europe has declined in June relative to May, but the final tabulation is a bit stronger than the flash estimate. China's private sector (composite or total PMI) expanded at the slowest pace in a year on a weakening [...]

The PMI gauge for Europe has declined in June relative to May, but the final tabulation is a bit stronger than the flash estimate. China's private sector (composite or total PMI) expanded at the slowest pace in a year on a weakening services sector.

The PMI gauge for Europe has declined in June relative to May, but the final tabulation is a bit stronger than the flash estimate. China's private sector (composite or total PMI) expanded at the slowest pace in a year on a weakening services sector.

Despite what has been upbeat news in the manufacturing sector, the services gauges have deteriorated more or less globally. The services sector carried the ball for growth for a long period in recovery when manufacturing was under pressure and now with some evidence of manufacturing recovering services is showing the wear and tear of its past burden.

Looking at the services sector across a group of seven countries (Germany, France, U.K., Japan, China, Russia, and India), we find the percentile standings for services average in the 62nd percentile over the last five years. For this group, the manufacturing standings average in the 68th percentile. The services gauges have a slightly higher standard deviation among their readings as well. I exclude the important U.S. economy from these comparisons because the ISM nonmanufacturing gauge is not yet available and while Markit gauge is available, the Markit and ISM readings have a stunningly different take on economic performance in the U.S. right now. That split is a major conundrum in its own right.

The service sector is much less visible across economic data, but it generally carries a much greater weight in the economy or in the PMI readings that the frequency of services data availability would suggest. That explains why PMI readings have fallen for the most part in June. In a grouping of 14 countries, 10 have lower Total PMI readings in June than in May. In May, it was a toss-up; seven had lower readings than in April. There is clearly some erosion in the services readings in train and services are not on the same expanding path as manufacturing.

Central banks/inflation

Central bankers seem to be taken by surprise by recent events. Some of this is reflected in their reaction to inflation, a phenomenon whose interpretation has been too-closely linked to oil prices, at least in my opinion. When oil is dominating the inflation result, central bankers need to take and maintain a broader view of inflation forces. Unfortunately, the hawks on various central banks around the world simultaneously pounced on a 'headline' inflation rebound that was not very real and instead apparently was 100% at the behest of oil prices. When oil prices recently receded, so did the push to the CPI and PPI (and in the U.S. PCE) inflation rates. The hawks had built their case for rate hikes on a fragile petroleum base that has since proved unstable and continues to have an uncertain fate as output from unrestricted OPEC members has been rising and as fracking in the U.S. continues to develop. To complicate this picture, at the same time oil prices have lost momentum so has the services sector.

Policy adrift

We have policy adrift. Central banks that were on the cusp of policy change are backtracking. Today ECB executive board member Peter Praet is talking of the importance of patience and persistence. In the U.S., we may learn more from the FOMC meeting minutes to be released later today, but already there are public comments by Federal Reserve officials that seem less hawkish in nature. The Bank of England saw two policy dissents in the direction of tighter policy, but since then more U.K. data have turned up lame and the Bank of England seems to be leaning toward causing banks to carry more reserves and to closely monitor lending to consumers to make sure excess credit is not extended. That may turn out to be a compromise effort between BOE hawks and doves.

On balance, policy is back in the realm of the great unknown. The largest EMU economies are running near five-year highs on their manufacturing PMI readings and for some on their services readings too. But on that same timeline, China's total PMI has a lower 40th percentile standing and the BRCS have a 54th percentile standing. The U.K. has a composite PMI standing in its 36th percentile, just a touch weaker than Brazil with a 38th percentile standing.

The new PMI view

The new total PMI view of the world is not as nice and tidy as the view formed only from manufacturing PMI data. As we have warned in the past, the PMI data are sensitive and can be quick to point out a change in direction. But that can also go off track and give the wrong impressive of strength. PMI data only measure breadth and although we usually make that leap of faith, strength is not breadth and breadth is not strength. After the release of these PMI data, we are perhaps even more confused about policy than we were before. And central bankers certainly are going to be resting their trigger fingers for a while.

The policy view

Attention may back away from the prospect of rate hikes for a while and shift to watching the impact of reverse QE in the U.S. (EQ?) as the Federal Reserve gets ready to shrink its balance sheet, reduce its holding of bonds and put more of a burden on the private sector to step in and take its place as a holder of these assets. One interesting question will be whether the expansion of the supply of high grade bonds to the private financial sector will harm foreign bond markets as the Fed exits and the market looks for replacement investors. There are also foreign exchange consequences as FX markets had shifted to expecting European rates to rise sooner rather than later and now all of that is back up in the air.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief