Global| Aug 12 2019

Global| Aug 12 2019Prices Drop in Portugal...Is It the Canary in the Coal Mine?

Summary

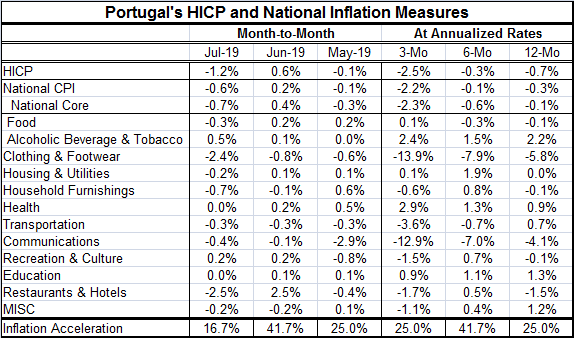

Portugal is not typically one of the low inflation countries in the EMU. That makes its 1.2% price drop in July and its year-on-year drop of 0.7% all the more striking. Compared to early members, Portugal ranks as the country with the [...]

Portugal is not typically one of the low inflation countries in the EMU. That makes its 1.2% price drop in July and its year-on-year drop of 0.7% all the more striking. Compared to early members, Portugal ranks as the country with the third greatest price level rise since the monetary union was formed. Only Spain and Luxembourg have seen their respective price levels rise by more. Portugal is neck-and-neck with Belgium for the third worst performance among the first 12 members. However, over the past five years, Portugal is tied for averaging the fifth best (lowest) inflation rate in the EMU, tied with the Netherlands and France among the 12 longest-lived members.

Portugal is not typically one of the low inflation countries in the EMU. That makes its 1.2% price drop in July and its year-on-year drop of 0.7% all the more striking. Compared to early members, Portugal ranks as the country with the third greatest price level rise since the monetary union was formed. Only Spain and Luxembourg have seen their respective price levels rise by more. Portugal is neck-and-neck with Belgium for the third worst performance among the first 12 members. However, over the past five years, Portugal is tied for averaging the fifth best (lowest) inflation rate in the EMU, tied with the Netherlands and France among the 12 longest-lived members.

Global risks

An IFO global survey has just named the trade war as having an adverse impact on the global economy. Goldman Sachs is not admitting that the war is having a larger than expected impact on the U.S. economy and no longer is expecting a relatively ‘quick end' to the conflict. All of this ramps up the potential for the trade war to be the spark that brings on recession with global dimensions. With inflation already running so low, a period of deflation could well lurk on the horizon.

Oil and gold

Oil and gold

Of course, weakening oil prices would be part of that equation too. On the day, oil is firming despite concerns about growth. But inflation trends are going nowhere higher anytime soon. The global trade situation has capped global demand. And even the mischief Iran is trying to create in the Gulf is not able to boost oil prices. However, there is enough concern to cause gold prices to stir.

Portugal's circumstance

Portugal's national core CPI is also falling year-on-year. All metrics the HICP, the national index and the national core are showing annual rate declines in prices of 2% or more over three months. Over three months, inflation is accelerating in only 25% of Portugal's price categories. Year-over-year, the prices also accelerate in only 25% of the categories. In July, prices are so widely weakening that month-to-month they accelerate in only 16.7% of the categories. Clearly, Portugal represents a good deal of prices weakness.

The canary?

The EMU economy is preparing for more policy ease. And it is beginning to look like it could not be coming a moment too soon. With such weak global growth and clear weakness within the EMU area itself, it can't be good news to see a country that is usually in the middle of the pack on its inflation performance has falling prices. The ECB is already running a negative rate policy and no one can really be sure how that works or if even more deeply negative rates would be more stimulative or would be treated as more alarming.

The coal mine...

While policy ease in the U.S. has met with some discord, one of the reasons for easing has been to keep inflation up. The Fed's inflation target has mostly been missed since it was adopted; as has been the experience of the ECB as well. But the Fed's recent rate cut met with resistance and garnered two member dissents. However, Fed Chairman Powell has spoken on the importance of keeping inflation expectations and interest rates from getting locked in path to the zero bound. Is the zero bound beckoning again?

Global implications

Weakening global growth will certainly raise that specter. Finding that Portugal already is logging prices declines in its headline and core inflation should set off some new alarm bells. In the U.S., President Trump has been acting coy about how soon he expects to wrap up his China trade deal although that may simply be Trump trying to seem in control of process where he has lost control.

Policy-making and policy-breaking

Policy-making in a global economy where important members do not wish to follow the rules or wish to project their own influence over events against the rules create a difficult situation. China has never been one to follow the rules. And unfortunately it was on a path to cut a deal with the U.S. until it began to see the U.S. President as damaged goods and in a political quagmire and backed off. In the wake of that setback, more tariffs have been plied on China and the U.S. has begun to take the position that it welcomes the customs revenues derived from tariffs.

...and as ever there is Brexit

In the meantime, there is also a threat from Brexit that could have some adverse consequences for Portugal either directly or indirectly. The U.K. is Portugal's fourth largest export market with exports of about $4 billion; U.K. exports to Portugal are about $2 billion equivalent.

Danger signal!

The chart of Portugal's inflation shows a relatively sharp fall-off for inflation. That is probably the most worrisome force in play. Inflation tends to move is smooth and steady patterns. When inflation movements are abrupt or exaggerated, it unusually means there is a new motivating force behind it. Since oil prices have been relatively steady and since inflation is falling, the main concern should be that weakening prices are an indication of potentially fast weakening growth. And, of course, when weak growth and weak inflation feed on one another and when interest rates are already at or below the zero bound and, in Europe, where fiscal policy is corseted by Maastricht rules, the consequences of such weakness could be severe and long lasting. If the Portuguese canary is wobbly, policy should be in action already.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief