Global| Apr 26 2016

Global| Apr 26 2016PPI Inflation Meets Euro Area and Friends

Summary

As oil prices gyrate, we continue to see weakness in PPI prices in the EMU and other EU member nations (for now the U.K. is still an EU member nation). However, in March, we do see some evidence of month-to-month PPI increases. [...]

As oil prices gyrate, we continue to see weakness in PPI prices in the EMU and other EU member nations (for now the U.K. is still an EU member nation).

As oil prices gyrate, we continue to see weakness in PPI prices in the EMU and other EU member nations (for now the U.K. is still an EU member nation).

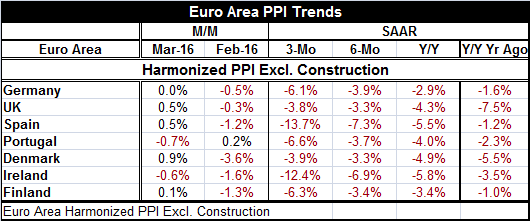

However, in March, we do see some evidence of month-to-month PPI increases. Denmark, especially, as well as Spain and the U.K. show some significant monthly PPI gains. Finland shows a small uptick. Germany exhibits a flat PPI in March. Portugal and Ireland continue to see PPIs fall. Some of this was inevitable as global oil prices have hit `bottom' and bounced putting some positive stimulus into the price pipeline. But oil prices also have flattened out pretty quickly and their future remains in doubt. So it is far too soon to begin to extrapolate PPI increases into the wild blue yonder as some so dearly would like to do.

Note that of the seven early reporters of PPI data in the table, all seven show a stepped up pace of decline over three months compared to six months despite March's scattered bounce in the monthly PPI data. Three of seven show a slower pace of decline over six months than over 12 months with one showing the same pace of decline for six-month as for 12-month. And five of seven still show steeper declines in their respective PPIs over 12 months than they showed over 12 months one year ago.

Spain shadows German inflation instead of being overshadowed

The chart shows one remarkable thing and that is how much more similar Spain's inflation rate has become close to Germany's - especially since 2013. Since late 2013, Spain's PPI has risen by less than Germany's as Spain has been under the constraint of an austerity program to remedy past budgetary and inflation excesses. From March 2008 to March 2016, Spain and Germany have PPI ex-construction inflation rates that have a 0.82R-square. This is up very sharply from their 0.49 correlation from March 1996 to March 2004 when the EMU arrangement was still quite new. The correlation of U.K. inflation with German inflation picked up sharply too between these two periods (although it is still a lesser correlation than for Germany and Spain) despite the fact that the U.K. has an independent currency and can choose its own inflation rate freely and let the currency rate offset it. In the early period, U.K. inflation had a 0.35 correlation with German inflation. In the more recent period, the correlation is up to 0.67. But the change in the correlations between Germany and Spain is almost identical to the change in the correlation between the U.K. and German inflation in the two periods.

More globalization

Very clearly we see the effects of globalization at work as well as the impact of Spain being tied to Germany in the EMU framework. There are certain global forces that are going to bite countries more or less the same. But there are also policy options on how to deal with shocks when they arrive. In the financial crisis aftermath, nearly all countries dealt with the crisis the same way: by keeping fiscal policy tight and trying to fight off weakness using monetary policy alone- to varying degrees. No one has had much success with that approach although those using monetary policy earliest and most aggressively have had the best results.

The oil shock vs. the oil thud

In the early 1970s, there was far more policy divergence and the experience with fluctuating exchange rates was quite new. There were some very different policy results as some countries sought to inflate away the impact of higher oil prices and others did not do so. Interestingly, then the U.S. tried to inflate away some of the pain of the relative price gain in oil only to find that it was generating inflation which led to oil prices going up again and eventually to threats from oil producers that they could unhook oil from dollar-pricing if the U.S. did not control its inflation rate. That eventually bought U.S. monetary policy to heel. I say that that is interesting because in this round it is the deflation that is being promoted by weak oil prices and a strong dollar that sent deflationary forces through the global economy and that the Fed has been all but ignoring until recently.

But in the wake of the financial crisis and tighter bank regulation, overall monetary policy easing is not having the impact in this cycle that it did 40 years ago. Nor is there as much divergence in how countries are approaching their choices. Then inflation took hold. This time deflation took hold. It should be clear which of them is the harder to fight.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief