Global| Dec 15 2004

Global| Dec 15 2004Japan "TANKAN" Eases in Q4, but Still Better Than Forecast

Summary

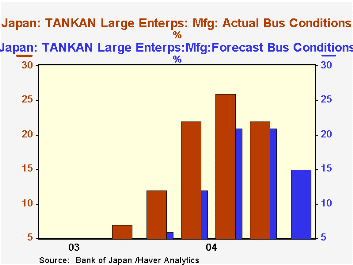

In the December TANKAN Survey, released today by the Bank of Japan, large Japanese manufacturers reported their overall business conditions at +22, off from September's +26 rating, but slightly more than the +21 they had forecast for [...]

In the December TANKAN Survey, released today by the Bank of Japan, large Japanese manufacturers reported their overall business conditions at +22, off from September's +26 rating, but slightly more than the +21 they had forecast for this quarter. Large non-manufacturing concerns maintained their Q3 conditions, with +11, modestly beating their expectation of +10. All businesses in all size categories edged down to +1 from the +2 last quarter, but did marginally better than their forecast for a 0 rating, or flat business. Medium-sized firms fell moderately short of both their Q3 performance and their forecast for this quarter, but small firms improved, albeit still in negative territory.

Individual industries had really mixed results. Among large manufacturing firms, eight industries saw business soften this quarter, while five are improving and two maintaining their Q3 pace. There seems to be no general classification of strength or weakening: such diverse groups as textiles, nonferrous metals and shipbuilding slowed, while petroleum and several machinery categories picked up. In non-manufacturing industries, retailing was sluggish but did better than expected; wholesale activity was somewhat slower than in Q3, but that sector still had one of the highest growth rates.

Despite the reduced vigor of Japanese business conditions as shown in the TANKAN, the Japanese stock market and currency both firmed following publication of the report. Apparently investors focused on components describing expected profits and business investment. Large manufacturing companies now project that their profits are rising 24.0% this fiscal year (ending March 31), 5.1 percentage points higher than the previous forecast. They also anticipate raising investment outlays by 23.4%, 2.2 points more than forecast before and 18 points more than last year's growth. Both of these results would likely raise corporate valuations and enhance the health of Japan's economy.

In the Haver databases, we present the TANKAN data two ways. Owing to the restructuring of the survey classification scheme and new sampling last March, we have segregated the recent detail data into new series in the "Japan" database. In summary data in the "G10" database, we link the all industry-all enterprise data with the history that uses the old methodology. This broad aggregate is less affected by the Bank of Japan's reorganization of the categories. By this special, linked measure, even though the Q4 result is down a point from Q3, it is still, at +1, only the second positive reading since Q1 of 1992, nearly 13 years ago.

| Business Conditions: % Favorable minus % Unfavorable | December 2004 September 2004 June 2004||||||

|---|---|---|---|---|---|---|

| Forecast for Mar |

Actual | Forecast for Dec | Actual | Forecast for Sep | Actual | |

| All Firms | -3 | 1 | 0 | 2 | -1 | 0 |

| Large Firms* | 12 | 16 | 15 | 19 | 16 | 16 |

| Manufacturing ("Headline Series") | 15 | 22 | 21 | 26 | 21 | 22 |

| Non-manufacturing | 10 | 11 | 10 | 11 | 11 | 9 |

| Medium-sized Firms** | -1 | 2 | 3 | 5 | 1 | 3 |

| Manufacturing | 2 | 11 | 10 | 14 | 7 | 11 |

| Non-manufacturing | -3 | -4 | -2 | -2 | -3 | -1 |

| Small Firms*** | -12 | -7 | -9 | -9 | -10 | -10 |

| Manufacturing | -1 | 5 | 3 | 5 | 2 | 2 |

| Non-manufacturing | -18 | -14 | -16 | -17 | -18 | -18 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief