Global| Jul 03 2017

Global| Jul 03 2017Japan's Tankan Survey and Outlook Perk Up

Summary

Japan's Tankan survey is conducted by the Bank of Japan; it is abroad survey executed across various industry classifications of Japanese firms and across firms of different size categories. The large enterprise survey is considered [...]

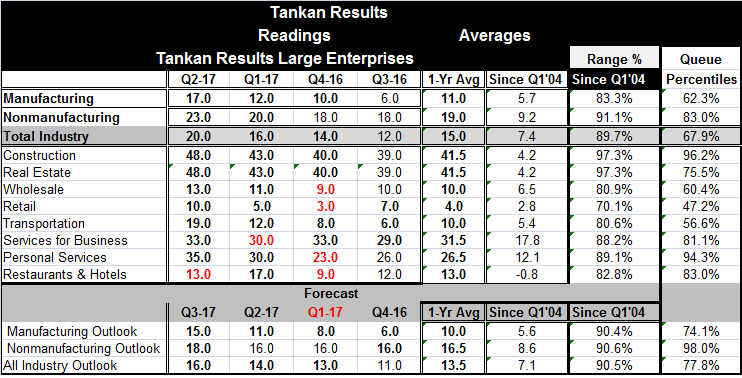

Japan's Tankan survey is conducted by the Bank of Japan; it is abroad survey executed across various industry classifications of Japanese firms and across firms of different size categories. The large enterprise survey is considered to be the bellwether with an emphasis on the performance of manufacturing.

Japan's Tankan survey is conducted by the Bank of Japan; it is abroad survey executed across various industry classifications of Japanese firms and across firms of different size categories. The large enterprise survey is considered to be the bellwether with an emphasis on the performance of manufacturing.

In Q2 the large manufacturing enterprise reading rose to 17 from 12 in Q1. This is the strongest reading since Q1 2014. The reading historically has only been only 17% higher at its best since Q1 2004 and it has only been better than this reading 38% of the time. These are not stellar metrics, but they are solid readings for manufacturing and they beat what had been expected.

Nonmanufacturing rose to a raw reading of 23 in Q2 from 20 in Q1. It was last higher in Q4 2015. Still, this index has only been higher historically by about 9% and has only been higher 17% of the time. Nonmanufacturing is more impressively firm in Q2.

As a result of the two sectors' results, the total industry reading rose to 20 in Q2 from 16 in Q1 to a reading that has only been higher historically by about 11% and a reading that has been higher about one third of the time. These are respectable metrics.

The real strength is in the outlook

However, what is more impressive in this report is the outlook for Q3. The outlook metric rose to 15 from 11 for manufacturing and to 18 from 16 for nonmanufacturing. For all of industry, the outlook rose to 16 from 14. More impressively, the manufacturing outlook has only been higher than this 26% of the time; the nonmanufacturing outlook has been better only 2% of the time. The all-industry outlook has been better only about 22% of the time. The outlook is very solid across both main sectors for large Japanese enterprises.

Sub-sector detail is solid

Sub-sector detail for the current Tankan readings shows increases in every sub-sector except restaurants and hotels where the Q2 reading slipped to 13 from 17. The strongest industry standings are for construction (96th percentile), personal services (94th percentile) and restaurants and hotels despite the slippage this quarter (83rd percentile). Only retailing (47th percentile) is below its historic median (which occurs at the 50th percentile mark) although transportation at a 56th percentile standing was only slightly above its historic median.

Summing up

On balance, Japan shows few truly weak sectors. It has strength across most of its survey industry groups. There is good strength in the manufacturing sector, the portion of this survey that Japanese specialists like to emphasize. However, the manufacturing sector lacks some of the gusto we see in nonmanufacturing and the outlook for the yen does not increase confidence that there is any surge ahead. Nonetheless, the outlook portion of the survey was especially strong and better than the current assessment. The Tankan did much better than had been expected.

The Bank of Japan will want to take this as a sign that its policies are on track, but there is no direct evidence in the report about inflation progress. Still, better growth and even better expectations for the future are more likely to be consistent with the BOJ's goals. There also was an increase in plans for investment in the current financial year from survey respondents with capital spending plans up by 8% compared to a 0.6% increase projected in the previous survey.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief