Global| Apr 01 2016

Global| Apr 01 2016Japan's Tankan: Firms Cut Back Outlook and Current Assessment

Summary

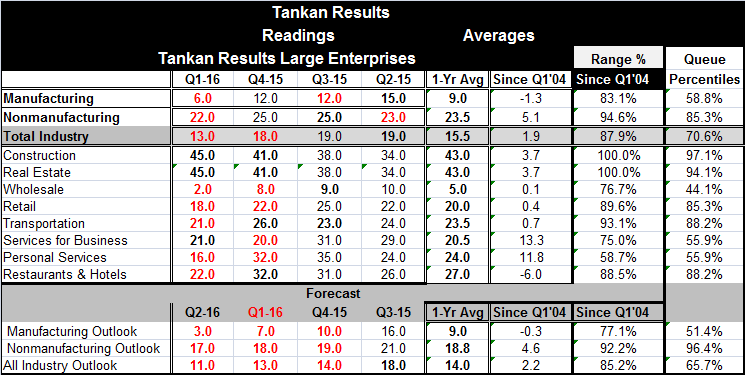

Japan's Tankan survey in which we focus on the responses of large firms shows a sharp reduction in the manufacturing firm assessment which has dropped back to +6 in Q1 2016 from +12 in Q4 2015. This is the weakest reading in 11 [...]

Japan's Tankan survey in which we focus on the responses of large firms shows a sharp reduction in the manufacturing firm assessment which has dropped back to +6 in Q1 2016 from +12 in Q4 2015. This is the weakest reading in 11 quarters (since Q2 2013; which had been the first positive reading after 6 straight negative quarterly readings).

Japan's Tankan survey in which we focus on the responses of large firms shows a sharp reduction in the manufacturing firm assessment which has dropped back to +6 in Q1 2016 from +12 in Q4 2015. This is the weakest reading in 11 quarters (since Q2 2013; which had been the first positive reading after 6 straight negative quarterly readings).

The large nonmanufacturing firm assessment also stepped back to an assessment of +22 in Q1 2016 from +25 in Q4 2015. This is its weakest reading since Q1 2015. The all-industry aggregate assessment fell to +13 in Q1 from +18 in Q4 2015, its weakest level since Q3 2014.

These are not the kinds of benchmarks that Japan wants to put in play. But firms obviously are scaling back their assessments of conditions and Japan is now more closely linked to China than to the U.S. economy and it is paying the price for that decision.

The all-industry outlook for Q2 2016 posted a reading of +11, down from +13 for Q1 2016. This is its weakest level since +11 was projected for Q2 2014. But that sharp downshift (from +16 in Q1 2014) was short-lived as firms quickly jumped back into a more positive outlook mode the very next quarter. This time, however, the scale back is part of an ongoing eroding process from +18 in Q3 2015 to +14 in Q4 2015 to +13 in Q1 2016 and finally to +11 in Q2 2016.

The outlook for manufacturing fell to +3 in Q2 2016 from +7 in Q1. This is the weakest outlook since a -1 was registered for Q2 2013. The all-industry outlook for Q2 2016 slips to +11 from +13 in Q1, the weakest reading since Q2 2014. Nonmanufacturing made a smaller step down to a reading of +17 for Q2 from +18 in Q1, the weakest reading since Q2 2015.

The perspective on these levels is that the total industrial Q1 assessment has a 70th percentile standing with nonmanufacturing in the 85th percentile and manufacturing in the 58th percentile. The outlook ranking is quite different for goods than for services. For manufacturing, the outlook at the 51st percentile is lower than the 58th percentile current assessment. For nonmanufacturing, the outlook standing is a still very robust 96th percentile standing, well above the 85th percentile assessment for Q1 activity. Japanese firms are relatively more upbeat on the future for nonmanufacturing than they are for manufacturing. Nonmanufacturing is quite upbeat and the forecast is a bit stronger than the Tankan current assessment and even more robust than that obtained from other current indicators of services or nonmanufacturing like the sector indices, the nonmanufacturing PMI and the economy watchers index. We will soon see if this kind of optimism is warranted.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief