Global| May 20 2009

Global| May 20 2009Japan GDP in Record Drop As Trade Collapses

Summary

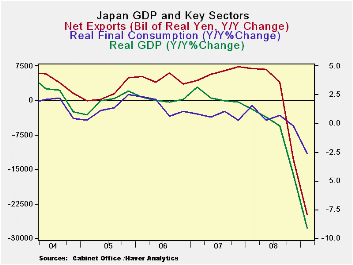

Japan is being led lower by its trade dependence as much as any large developed country. Exports are lower at a 70% annual rate Q/Q and by 37% Yr/Yr. Imports meanwhile are dropping at a lesser but still outsized 47% annual rate in Q1 [...]

Japan is being led lower by its trade dependence as much as

any large developed country. Exports are lower at a 70% annual rate Q/Q

and by 37% Yr/Yr. Imports meanwhile are dropping at a lesser but still

outsized 47% annual rate in Q1 and are off by nearly 15% Yr/Yr.

Japan’s import to GDP ratio has fallen by 6.2% Yr/Yr less than

in the US where that ratio has fallen by a huge 14%. But exports are a

much larger part of Japan’s economy, so the drop has hurt it more.

Import-to-GDP ratios have fallen sharply among the large developed

economies in general.

Japan’s GDP drop at 15.2% Q/Q saar outstrips Germany’s drop of

14.4% and its Yr/Yr decline of 9.1% exceeds Germany’s 6.9%. It is no

coincidence that these large set backs -- the largest among G-7

countries by a long shot -- befall two of the most highly efficient

global economies that also are highly dependent on trade.

Trade tends to be a highly income elastic GDP component.

Export and import growth rates are pro-cyclical. In good times trade

dependence will help to pump-up GDP growth, but in bad times –

recessions - it will drag it down as it is now. In the US, since it is

a trade deficit county, the trade setback actually boosts GDP. What we

are seeing in Japan is the mirror image of that relationship.

In Japan domestic demand is down by less than GDP itself. But

housing and business capital formation are each down at a more rapid

pace than GDP. Japan will need world trade to recover before it can

mend its economy. Its economic structure means that some of its

required fixing it out of its control.

| Japan GDP | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Consumption | Capital Formation | Trade Domestic | Domestic | |||||||

| GDP | Private | Public | Gross Fixed Capital |

Plant& Eqpt |

Housing | X-M | Exports | Imports | Demand | |

| % change Q/Q at annual rates of change; X-M is Q/Q change in Billions of real yen | ||||||||||

| Q1-09 | -15.2% | -4.2% | 1.3% | -27.5% | -35.5% | -20.0% | -11.2 | -70.1% | -47.7% | -9.8% |

| Q4-08 | -14.4% | -3.1% | 6.4% | -14.6% | -24.2% | 23.7% | -15.6 | -47.1% | 13.1% | -2.3% |

| Q3-08 | -2.5% | 0.4% | -0.7% | -9.7% | -16.4% | 13.2% | 0.0 | 4.0% | 6.3% | -2.3% |

| Q2-08 | -3.5% | -3.8% | -3.1% | -9.5% | -11.2% | -7.7% | 1.9 | -3.2% | -15.7% | -5.7% |

| % change Yr/Yr; X-M is Yr/Yr change in Gap in Billions of real yen | ||||||||||

| Q1-09 | -9.1% | -2.7% | 0.9% | -15.7% | -22.4% | 0.8% | -24.9 | -36.8% | -14.7% | -5.1% |

| Q4-08 | -4.5% | -0.2% | 0.2% | -7.8% | -12.0% | 11.8% | -13.1 | -12.5% | 2.8% | -1.8% |

| Q3-08 | -0.2% | 0.7% | 0.4% | -4.9% | -4.5% | -5.5% | 4.0 | 4.5% | 0.1% | -1.1% |

| Q2-08 | 0.6% | 0.3% | 0.1% | -3.6% | 0.5% | -16.5% | 6.7 | 6.3% | -2.1% | -0.8% |

| 5-Yrs | -0.4% | 0.5% | 1.2% | -2.8% | -0.7% | -3.5% | na | -2.6% | 0.2% | -0.1% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief