Global| Feb 06 2008

Global| Feb 06 2008Italy’s Inflation Rate Shows Core Pressure Through Dec; In Jan Headline Abates

Summary

Not every inflation report or trend in the EMU is bad news. But the news is still not pleasing to an ECB that is trying to inherit the mantel of inflation fighting respectability from the Bundesbank. Inflation in the Euro Area [...]

Not every inflation report or trend in the EMU is bad news.

But the news is still not pleasing to an ECB that is trying to inherit

the mantel of inflation fighting respectability from the Bundesbank.

Inflation in the Euro Area consists of an overall HICP measure but

there is also the country level data that contribute to the HICP.

Italy’s new inflation report is shown below. Headline inflation slowed

sharply in January and the three-month growth rate edged slightly lower

from its six-month value. Even so, that rate is unacceptably high.

Across categories inflation slowed producing a diffusion rate of 42%

implying that the deceleration was relatively widespread. But over six

months diffusion shows that it has accelerated and over 12 months it is

about the same as it was a year ago in terms of the breadth of the

acceleration/deceleration (diffusion) even though it is higher in terms

of the headline and the core.

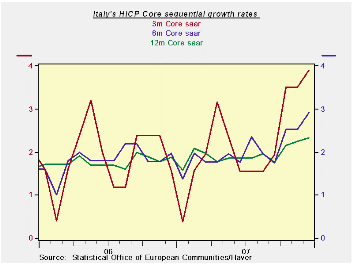

The chart shows that the core rate has been steadily accelerating. But if energy prices abate that trend should be truncated. In short Italy’s data are the exact reason that the ECB remains wary. While the current month hints at a break in the pace the trends are simply not good enough to take the ECB off guard.

| Italy HICP and CPI details | |||||||

|---|---|---|---|---|---|---|---|

| Mo/Mo % | Saar % | Yr/Yr | |||||

| Jan-08 | Dec-07 | Nov-07 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| HICP Total | 0.1% | 0.4% | 0.4% | 3.5% | 3.9% | 3.1% | 1.9% |

| Core | -- | 0.3% | 0.2% | -- | -- | -- | 1.6% |

| CPI | |||||||

| All | 0.4% | 0.4% | 0.4% | 4.9% | 3.8% | 2.9% | 1.8% |

| CPI excl Tobacco | -- | 0.4% | 0.4% | -- | -- | -- | 1.6% |

| Food | 0.5% | 0.5% | 0.5% | 6.0% | 6.9% | 4.5% | 2.6% |

| Alcohol | 0.9% | 0.2% | 0.1% | 4.6% | 4.7% | 3.5% | 4.6% |

| Clothing & Shoes | 0.1% | 0.1% | 0.2% | 1.8% | 1.8% | 1.6% | 1.4% |

| Rent & Utilities | 1.1% | 0.5% | 0.7% | 9.8% | 7.4% | 4.0% | 4.2% |

| Housing & Furniture | 0.8% | 0.2% | 0.2% | 4.7% | 3.6% | 3.6% | 1.6% |

| Health Care | 0.2% | -0.2% | -0.2% | -1.0% | 0.5% | 0.7% | -1.5% |

| Transport | 0.9% | 1.1% | 0.7% | 11.7% | 7.4% | 5.5% | 1.7% |

| Communication | -0.7% | -0.1% | 0.0% | -3.4% | -4.2% | -8.4% | -4.5% |

| Recreation & Culture | -1.1% | 0.6% | 0.1% | -1.6% | -0.2% | 0.6% | 0.9% |

| Education | 0.1% | 0.1% | 0.1% | 1.5% | 2.1% | 2.2% | 2.3% |

| Restaurant & Hotel | -0.1% | 0.2% | 0.1% | 0.8% | 1.4% | 2.4% | 2.4% |

| Other | 0.4% | 0.1% | 0.4% | 3.7% | 3.5% | 3.1% | 2.3% |

| Diffusion | 41.7% | 66.7% | 50.0% | -- | |||

| Type: | Diffusion: Compared to | 6-mo | 12-mo | Yr-Ago | -- | ||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief