Global| Feb 27 2015

Global| Feb 27 2015Italy's Inflation In An About Face

Summary

Suddenly after outright falls for two straight months, Italy's inflation rate is up by 0.6% in February. The monthly gain is the largest since October 2011. Italy's domestic inflation gauge also reversed to gain 0.3% after two [...]

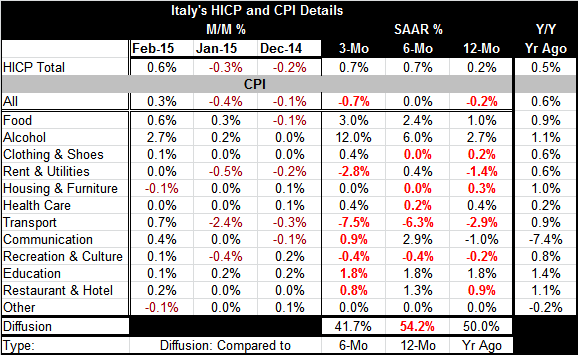

Suddenly after outright falls for two straight months, Italy's inflation rate is up by 0.6% in February. The monthly gain is the largest since October 2011.

Suddenly after outright falls for two straight months, Italy's inflation rate is up by 0.6% in February. The monthly gain is the largest since October 2011.

Italy's domestic inflation gauge also reversed to gain 0.3% after two straight monthly drops and five drops in the last eight months. Of the 12-main Italian domestic components, only two showed price drops in February: `housing and furniture' and `other.' Despite ongoing weak global energy prices, rent and utilities prices were flat after being flat or falling since October. And even transportation prices rose 0.7% after being either flat or falling since July. This reflects the relatively greater role of taxes in the European energy market. The full extent of the global market energy price slide never makes it all the way to consumers' pockets because taxes are a larger portion of the prices that Europeans pay.

Still, inflation in Italy across most price categories is still net lower over three months than over six months with a diffusion value on inflation rate comparisons of 41.7 (50 would be a neutral reading). Over six months inflation is showing some slight diffusion tendency to be higher than over 12 months with a value of 54.2. This compares with a `pure' agnostic 50 diffusion reading for 12 months vs. 12 months ago. These diffusion readings reflect comparing inflation rates for the 12 major CPI categories and their respective rates of inflation over various step-wise horizons: three months, six months and 12 months. As a perspective, overall domestic inflation in Italy falls at a 0.7% pace over three months in the aggregate, it is flat at zero percent over six months and it is falling at a 0.2% annual rate over 12 months. Over this whole 12-month stretch, inflation in Italy is very low and flits with deflation persistently. But the comparison across categories shows some uneven trends for inflation momentum.

We use diffusion metrics to try to test or establish the veracity of overall trends. Since price trends in the aggregate inflation measures apply weights to various components, we are always interested in knowing how much the headline trend reflects similar movements in the inflation readings across components. Especially when energy prices are shifting, we like to be sure that energy alone is not dictating the measure of inflation. When one component is making most of the inflation change while its movement and weight may `justify that' it is also true that in such a situation we are really looking at a change in relative prices more than simply a change in inflation. When one price components with a large weight makes a sharp shift it affects the measured rate of inflation while it is moving and then that effect ceases to exist when it stops moving. The actual overall and persisting impact on inflation really depends on other macroeconomic events especially the behavior of monetary policy. Only monetary policy can turn a change in relative prices into persisting deflation or inflation.

In Europe, with energy prices pushing all the buttons for the down elevator, the ECB is pressing the up buttons and launching a program of QE to try to counteract that.

Italy's inflation rate remains low at 0.2% over 12 months. Its HICP pace is still 0.2% higher than Germany's rate which is flat over 12 months. Europe still has to be mindful of being on a path for improvement. Since the EMU was formed, Germany has simply become too competitive and too different from its fellow trade partners in the EMU for the good of EMU stability. Not only do countries like Italy that have not been careful enough about controlling their inflation since the EMU was launched need to get back lost competiveness, they need to make sure that the slippage stops. This month Italy continues to slip relative to Germany.

With energy prices still so low, it is surprising to see evidence in Europe that the impact on monthly prices has stopped pushing price levels lower at least in Germany and in Italy as of February. Maybe this is more of a hiatus that a cessation. The next few months will tell. But whatever it is, EMU members must take care to not go back to their old ways and allow Germany to continue to run the lowest inflation rates in the EMU. If that happens, the EMU will just be sowing the seeds of another future unraveling.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief