Global| Jan 14 2016

Global| Jan 14 2016Italy's Industrial Output Declines

Summary

Reporting later than most EMU nations, Italy released industrial output figures for November showing that IP fell by a sharp 0.7% one month after October's 0.8% gain. Despite the relatively sharp drop, Italian overall IP trends are [...]

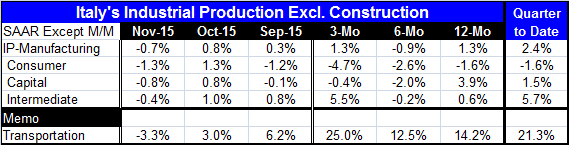

Reporting later than most EMU nations, Italy released industrial output figures for November showing that IP fell by a sharp 0.7% one month after October's 0.8% gain. Despite the relatively sharp drop, Italian overall IP trends are largely still intact. However, several key IP components are showing signs of wear.

Reporting later than most EMU nations, Italy released industrial output figures for November showing that IP fell by a sharp 0.7% one month after October's 0.8% gain. Despite the relatively sharp drop, Italian overall IP trends are largely still intact. However, several key IP components are showing signs of wear.

Industrial production fell across the board in November with consumer goods and capital goods each making their third drop in four months. Intermediate goods output is down in two of the last four months. Consumer goods show encroaching weakness with short-term growth rates demonstrating more intense declines. While capital goods output shows a solid 3.9% gain over 12 months, output in the sector declines over three months as well as over six months. Intermediate goods, with a shallow 0.6% 12-month gain, show a strong 5.5% pace of expansion over three months.

While overall IP trends are more or less steady, the IP sectors show a good deal more variation than the headline and more weakness. Consumer goods output is a particular problem. Strength in intermediate goods without accompanying strength in either consumer goods or capital goods is suspiciously unreliable. Of course, the weakness in Italy dovetails with yesterday's EMU-wide report that showed similar weakness spreading across the euro area. Globally, manufacturing is still weak; demand is still slack and supply is still overly plentiful.

As 2015 ends, manufacturing is still on the ropes. And as 2016 begins, there is global turbulence in markets. Stocks are not finding a solid economy to underpin them in this environment as manufacturing weakness has been in train for some time and the services sector has been doing little more than limping ahead. Growth has been about little more than sustenance.

In the U.K. today, the Bank of England held its interest rates steady. In Indonesia, the central bank cut rates to try to stimulate growth. There are no magic bullets and the old fashioned macroeconomic levers simply are not producing results. Italy is a prime example of this malaise, as its manufacturing sector continues to advance, albeit sluggishly late in 2015 as global markets unravel around it amid little sign of repair.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief