Global| Mar 18 2015

Global| Mar 18 2015Italian Trade Trends Stagnate Along with Much Else in Europe

Summary

Italy's trade picture showed a weakening in exports and still-weak import growth as it echoed the message from the broader European trade data today. European data showed a larger surplus in January as exports remained flat and [...]

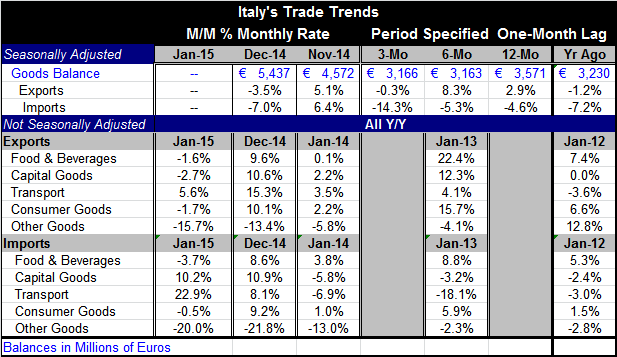

Italy's trade picture showed a weakening in exports and still-weak import growth as it echoed the message from the broader European trade data today. European data showed a larger surplus in January as exports remained flat and imports fell. The picture from Italy shows imports growing more slowly than exports since 2011 with both flows slowing, having lost some upward momentum recently. Seasonally adjusted flows show exports rising by 2.9% over 12 months with imports falling by 4.6% over 12 months. Sequential growth rates from 12-months and in on the same flows show exports sputtering and shrinking over three months with imports progressively weakening. As is the case for Europe these are `good enough' trends to keep Italy in trade surplus position.

Italy's trade picture showed a weakening in exports and still-weak import growth as it echoed the message from the broader European trade data today. European data showed a larger surplus in January as exports remained flat and imports fell. The picture from Italy shows imports growing more slowly than exports since 2011 with both flows slowing, having lost some upward momentum recently. Seasonally adjusted flows show exports rising by 2.9% over 12 months with imports falling by 4.6% over 12 months. Sequential growth rates from 12-months and in on the same flows show exports sputtering and shrinking over three months with imports progressively weakening. As is the case for Europe these are `good enough' trends to keep Italy in trade surplus position.

The commodity composition of Italy's trade shows NSA (not seasonally adjusted) exports lower year-on-year for all categories except for transportation equipment. Imports show a surge in capital goods and transportation equipment imports with both flows up year-over-year for two months running. But other imports are lower across the board at least in January compared to one year ago.

Italy and the EMU as a whole are struggling to reestablish growth. Meanwhile the ECB has launched its program of QE to spur growth. Still, today, there was a chilling protest in Frankfurt of the ECB as enforcing austerity rules. Cars were set on fire and there were real clashes by protestors from Germany as well as participants from across the euro area in the sleepy town of Frankfurt.

The drop in EMU-wide imports in January is evidence that austerity is still holding back growth. While the ECB is trying to jump start growth with QE, it has also been supporting the notion that Greece has to toe the line on its past debt negotiations and stick to its agreed austerity plan in order to get the last monies comping to it under that plan and certainly if it wants to gain any new funds. But does that make the ECB the guardian of austerity?

European trade performance is evidence that competiveness is not fully restored in the euro area, although one consequent of QE has been to topple the euro, a currency that now appears to be below its parity on a number of metrics. Since it takes a while for trade flows to respond to exchange rate changes and since the euro has been falling for some time and since global growth is still weak, the response of European trade to the weaker euro to date will take at least another year to be fully reflected in trade flows; even then it could be muted because of weak international growth.

Italy's trade surplus data underline that Italian trade has been improving as its string of surpluses trace back to mid-2012. However, this has not been a case of surging exports driving improved trade flows as much as it is the same EMU-wide story that weak and falling imports stemming from weak domestic demand have paved the way for even listless exports to produce trade surpluses.

As the protests in front of the ECB tell us, Europe is still confused. Is the ECB the source of the euro area's problems or its savior with QE? Is it simply the most visible institution to protest?

The recent back and forth over Greece is the most recent outward sign of unresolved issues in the euro area. However, we now have this clash in Frankfurt and have no idea who the protestors are or where they are from. In the most recent negotiations with Greece, it was reported that Spain and Portugal- not Germany- were the two countries that were the most strident about what Greece had to do. That might have been because they are the two countries closest to the `edge' with the most to lose if things go badly in Greece.

What we lean from today's data is that European and Italian trade flows are still pressured. The impact on the drop of the euro has not yet turned around these trade flows. Yet, these flows do not represent the impact of the euro's current low value- that is still in train.

With the markets waiting for the Fed at today's meeting to sweep away the word `patient' from its policy statement, Christine Lagarde is warning of some potential adverse market impacts. The Fed is not close to hiking rates. But its actions today could take away the two-meeting security blanket that past Fed language had provided. Taking away this security blanket may put the markets more at risk to a policy move in some technical sense, but the U.S. economy will still have to support such a move. Weakening U.S. data on a broad front over a period of several months no longer seems to do that. Just as Europe is waiting to see a kick from the weak euro exchange rate on its trade and growth, so the U.S. is starting to see some impact from the opposite ongoing rise in the dollar exchange rate.

The international situation is a mess. Central banks are trying their best to just ignore it. But the falling euro makes the huge German trade surplus bigger even as the rising dollar will make the massive U.S. current account deficit even larger. Exchange rates may be moving in a sensible direction to spur growth, but they are insensibly making trade imbalances worse. A different set of policies should substitute domestic policy action for the reliance on exchange rates and their perverse international effects. But that is not going to happen. Exchange rates have been pressed into action precisely because domestic action (or EMU-wide action) is not possible. Thus, the global economy continues to destabilize itself.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief