Global| May 26 2016

Global| May 26 2016Italian Retail Sales Fall in March Amid Other Signs of Weakness

Summary

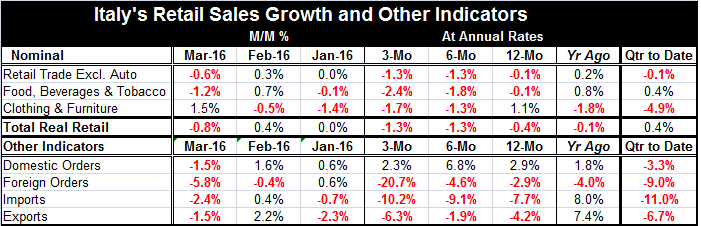

Weak march; weak trends Recent Italian data have been backtracking...big time. Today's retail sales report shows that nominal sales fell by 0.6% in March with real retail sales down by 0.8%. This is the first drop in real retail sales [...]

Weak march; weak trends

Weak march; weak trends

Recent Italian data have been backtracking...big time. Today's retail sales report shows that nominal sales fell by 0.6% in March with real retail sales down by 0.8%. This is the first drop in real retail sales in five months; although in two of the last five months, sales were flat. To put another way, there have only been four month-to-month real sales gains reported in the last 11 months.

Widespread slowing in retailing

Growth trends show pronounced weakness in sequential retail sales over the last three-month, six-month and 12-month. On all those horizons, real and nominal sales are falling as are food, beverages & tobacco and clothing & furniture (the latter category is a minor exception with a gain over 12-month). Real and nominal sales in addition to falling also are decelerating on these horizons.

Q1 is weak and mixed

In the just-completed first quarter (Qtr to Date), nominal ex-auto sales are slightly lower while real sales are showing slight growth. Nothing is `strong' or `firm.'

Both Italy and EMU show weakness in retailing

However, Italy's story is not just about weak sales. In the chart, we can see that the weakness in Italian sales has been mirrored by weakening sales in all of the EMU- its surrounding environment. And Italy also has weakness in many other areas.

Many Italian gauges flash weakening signals

Yesterday a rash of reports put Italy's economy in a poor light. Italy reported a drop in domestic industrial orders in March and a large drop in foreign-sourced industrial orders. Imports fell by 2.4% in March and exports fell by 1.5%. For Italy a variety of measures show economic weakness and show that weakness is spreading.

Other indicators show a breadth of slowing trends as well

Turning to the sequential growth picture from 12-month to six-month to three-month, we find that Italian domestic sourced orders still are growing steadily despite their setback in March. But foreign-sourced orders are declining and contracting at an alarmingly fast accelerating pace. Imports, too, show an acceleration in their sequential pace of decline, but a milder slowdown is in train there. Weak imports are often a sign of weak domestic demand. To that extent, weak imports dovetail with the weakness reported for retail sales. Italian exports do not show consistent deceleration over these periods, but exports are falling on all horizons and the pace of contraction has stepped up over three-month compared to six-month. In short, there is no good news here, only bad news and worse news.

Indicator weakness in the quarter-to-date with mixed signals for manufacturing

In the quarter-to-date, all these indicators are showing drops. Italy is clearly experiencing rather broad weakness. Italian consumer confidence has peaked and is now eroding off peak. Industrial production in Italy shows a decline for IP in all three sectors in March: consumer goods, capital goods and intermediate goods. But sequential growth rates show some strength except for consumer goods output. And contrarily manufacturing output sill posts a very solid 3.8% rate of growth in the just completed first quarter.

Summing up the bad news

Italy is showing widespread weakness not just weakness in retailing- but the weakness in retailing and involving the consumer is echoed in many different reports. Meanwhile, factory sector weakness is encroaching underpinned by weak trade and indicators of weaker domestic demand (weak imports) and slipping consumer confidence. The weakening trend for EMU retailing is not an encouraging statement about the broader environment either. In the EMU, both money and credit growth have failed to ignite in the face of greater ECB stimulus; both money and credit growth still are slowing. Negative interest rates are putting more pressure on banks. Earlier this week, we showed that the EMU-wide PMI data were much weaker for the EMU than for its two largest economies, Germany and France. Today's tour through Italian trends reveals Italy as one of those countries still bearing the brunt of weakness in the EMU. Germany is doing well and that always helps to dress up the EMU-wide-reported data. But there is still a lot of weakness in the EMU outside Germany. The Italian data trends are a testament to how a relatively large economy in the EMU can continue to struggle even when given the joint tail winds of ECB stimulus and a weak euro exchange rate. Italy's problems seem to be entrenched and worsening.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief