Global| Jan 20 2010

Global| Jan 20 2010Italian Orders Continue Upswing

Summary

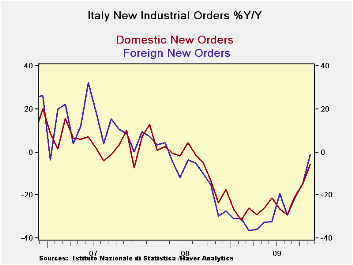

Italian orders surged beyond expectations in November rising by 2.6%, marking three straight months of increases and increases in seven of the last eight months. These statistics register in the sequential growth rates in the table [...]

Italian orders surged beyond expectations in November rising by 2.6%, marking three straight months of increases and increases in seven of the last eight months. These statistics register in the sequential growth rates in the table above as Italy’s orders growth is posting progressively higher rates of growth over shorter periods of time. This is a sign of acceleration in action. While foreign orders are leading the way Italy’s domestic orders have been surprisingly strong, especially over the past three months.

As impressive as these results are they are distorted to some extent by having that one drop in the past seven months (coming four months ago) as an outsized drop of nearly 9%. Foreign orders still have not gotten back to their July 2009 peak levels and have fallen in two of the past four months.

Surprisingly, domestic orders have just moved beyond their July level with this report and seemingly are gaining momentum. The sequential growth rates exaggerate a bit the strength of the rebound, yet the transition to a better industrial sector seems to be real.

In an economy that had fiscal excesses prior to the financial crisis and was not able to mount the stimulus that some other countries did, Italy’s performance is impressive. It is also impressive that at a time that other economies are struggling mightily, Greece with debt, Spain with real estate and Iceland with responsibility, Italy, a favorite target of speculators, has been able to mount a very good looking recovery.

Business confidence is still somewhat circumspect as is consumer confidence, but all-in-all, the industrial rebound is looking especially sound in November, coming at a time when others have been foundering. Germany’s orders did snap back partially in November after an October set back and France has had two declines in orders in a row in October and November.

There are no new initiatives to account for Italy’s improvement. For the time being we can welcome the progress while at the same time being somewhat skeptical of this progress in the face of difficulties elsewhere.

| Italy Orders | ||||||

|---|---|---|---|---|---|---|

| Saar exept m/m | Nov-09 | Oct-09 | Sep-09 | 3-mo | 6-mo | 12-mo |

| Total | 2.6% | 0.6% | 6.0% | 42.9% | 11.9% | -4.1% |

| Foreign | 2.8% | -0.1% | 8.1% | 51.9% | 25.3% | -1.1% |

| Domestic | 2.4% | 1.0% | 4.7% | 38.0% | 5.9% | -5.6% |

| Memo | ||||||

| Sales | 1.5% | -1.6% | 2.4% | 9.4% | 1.5% | -9.7% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief