Global| Jul 11 2017

Global| Jul 11 2017Italian IP Perks Up

Summary

Italy's industrial production gained 0.9% in May, reversing a 0.7% drop in April. IP growth in Italy has been a very steady and solid at 3% or better over 12 months and six months; however, having stepped up to a 5.6% pace over three [...]

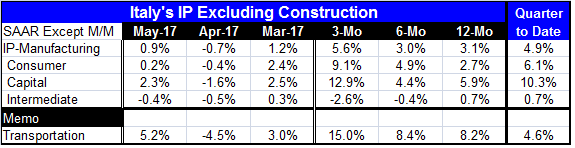

Italy's industrial production gained 0.9% in May, reversing a 0.7% drop in April. IP growth in Italy has been a very steady and solid at 3% or better over 12 months and six months; however, having stepped up to a 5.6% pace over three months.

Italy's industrial production gained 0.9% in May, reversing a 0.7% drop in April. IP growth in Italy has been a very steady and solid at 3% or better over 12 months and six months; however, having stepped up to a 5.6% pace over three months.

The step up in output is led by capital goods output and consumer goods output. Capital goods output is up to a 12.9% annualized pace over three months with consumer goods output up to a 9.1% pace. This strength is offset by intermediate goods where output is actually on a contracting run and decelerating with a decline at a -2.6% annual rate over three months.

The quarter-to-date results echoes these trends with capital goods output up at a 10.3% annual rate, consumer goods output up at a 6.1% pace and intermediate goods bringing up the rear on a 0.7% gain.

Transportation equipment has had a firm trend, accelerating to a strong gain of 15% at an annual rate over three months. The output of transportation equipment is up at a 4.6% pace in the quarter-to-date.

Italian industrial orders data are only up-to-date through April. But even on that timeline, orders are not showing a lot of momentum. Over three months ended in April, Italian industrial orders are flat. Orders are only up 4.2% over 12 months. Orders are led by domestic strength with a 12-month gain of 5.6% compared to 2.5% for foreign orders. Neither foreign nor domestic orders are strong over three months.

While Italian IP is doing well and thriving based on domestic demand, retail sales growth in Italy is not strong nor is it gaining momentum. Consumer confidence has been in a long slow slide as well. Despite those trends, business optimism is still on the rise.

On balance, Italian IP seems in good shape on solid trends. However, output is not well underpinned by orders and consumption trends have been faltering, a potential problem for a sector being importantly boosted by domestic demand.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief