Global| Mar 13 2013

Global| Mar 13 2013IP Slows Its Growth in EMU

Summary

Manufacturing industrial production fell by 0.6% in January. The drop follows a gain of 1.1% in December which follows a 0.8% drop in November. Although manufacturing production is declining over all horizons its pace of decline seems [...]

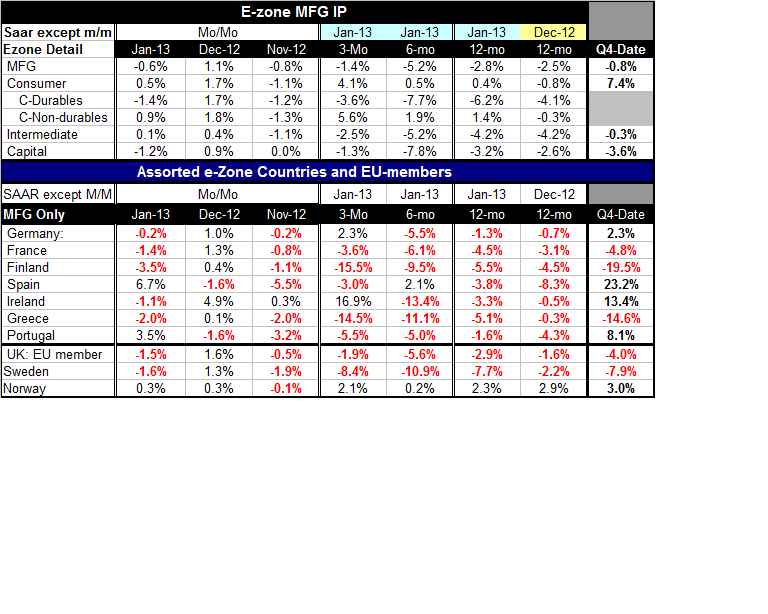

Manufacturing industrial production fell by 0.6% in January. The drop follows a gain of 1.1% in December which follows a 0.8% drop in November. Although manufacturing production is declining over all horizons its pace of decline seems to be slowing. Over three months as its 1.4% annual rate of decline compares to a 5.2% annual rate of decline over six months. In January output of consumer goods increased by 0.5% intermediate goods increased by 0.1% the capital goods fell by 1.2%.

Manufacturing industrial production fell by 0.6% in January. The drop follows a gain of 1.1% in December which follows a 0.8% drop in November. Although manufacturing production is declining over all horizons its pace of decline seems to be slowing. Over three months as its 1.4% annual rate of decline compares to a 5.2% annual rate of decline over six months. In January output of consumer goods increased by 0.5% intermediate goods increased by 0.1% the capital goods fell by 1.2%.

The pattern of growth has been such for industrial production that manufacturing output is falling is falling at a 0.8% annual rate one month into new quarter with declines in intermediate goods of 0.3% at an annual rate and a drop in capital goods output of 3.6% at an annual rate. The output of consumer goods is considerably stepped up to a positive rate of growth of 7.4%. The consumer sector is starting to take the lead as Q1 2013 begins.

Output has undergone a January decline in most countries of the Eurozone the exceptions are very some of the weaker countries. Spain had an increase of 6.7%, Portugal an increase of 3.5%. Most reporting countries are showing declines over three months as manufacturing output is declining across most of the reporting countries except Ireland and Germany. For example France has a decline of 3.6%, Spain's IP is declining at a 3% pace, Portugal posts a decline of 5.5% but Greece and Finland show stepped up rates of decline of over 10%. Over six months only Spain has an increase in manufacturing output; over 12 months all the countries the table show declines in industrial production if they're EMU members. From these patterns we see the hint of progress in the basic trends for IP.

The quarter to date finds manufacturing output in Germany, Spain, Ireland and Portugal increasing while France, Finland and Greece are showing declines in the first quarter compared of fourth quarter of last year.

In terms of recovery in this cycle Norway actually leads the pack among European countries it's not EMU member but it's manufacturing output is only 3% below its past cycle peak followed by Germany that is only 6% below its past cycle peak. After that we find the UK which is 11% below its past cycle peak. The countries that are still having the biggest difficulty are Greece which is 32% below its past cycle peak, Spain which is 29% below its past cycle peak and Finland is 23% below its past cycle peak of manufacturing output.

The bottom line is that the manufacturing sector remains under a great deal of pressure in the countries of the European Monetary Union. Upward momentum still has not been reestablished but it is fighting to take hold. Consumer goods output seems to be leading the way as it has risen in two consecutive months. Intermediate output also is up in two consecutive months, but by small amounts. Capital goods output remains jagged. It was flat in November, up by 0.9% in December and now off by 1.2% in January. It's not clear where the trend is going for capital goods. But since consumer moods remain so depressed it is somewhat surprising and yet encouraging to see that consumer goods output is showing the most life among the output sectors in the European Monetary Union. With such a high degree of slack throughout the Union consumer goods demand will have to lead since there can hardly be any demand for investment goods in such a slack-ridden economy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief