Global| Apr 14 2010

Global| Apr 14 2010IP Rebound Screams Recovery

Summary

Even with that strong-seeming chart and rock solid 0.9% gain in February, manufacturing IP in the Zone remains some 14% below it past cycle peak. But eh current progress looks good as growth over 3-and 6-months have average a pace of [...]

Even with that strong-seeming chart and rock solid 0.9% gain in February, manufacturing IP in the Zone remains some 14% below it past cycle peak. But eh current progress looks good as growth over 3-and 6-months have average a pace of 19%. The consumer sector continues to lag with a three-month growth rate of 2.2%.

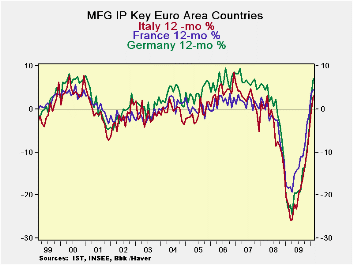

Among large Euro-Area member countries Spain grew the strongest in Feb, but it is a volatile report from Spain that fell by 3.4% in January, undercutting the impact of the gain in February. The UK, an EU member, had the next strongest gain among large European economies at 1.3% but that was a recoup from a -0.9% result in January. Italy with a 0.2% rise on the heels of a 1.7% gain has the best two-month result followed by Germany at 0.2% and 0.6%, in Feb and Jan, respectively. Still, both Germany and Spain show IP contractions over three-months. Spain’s output is still falling over 12-months but over 12-months German IP is up by 7.1%., followed by France at 3.3% Italy at 3% and the UK at 1.5%.

The February gains were on the back of a spike in intermediate goods output which advanced by 1.5%. Capital goods output rose by 0.9%. The consumer categories receded. Europe needs to get its consumer in gear. Europe, like many countries is trying to let its export sector pull it out of its recessionary hole almost all by itself. This is imbalanced growth that leans heavily on demand with origins elsewhere. Europe needs to learn to stand on its own two feet.

| Euro-Area MFG IP | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | Mo/Mo | Feb 10 |

Jan 10 |

Feb 10 |

Jan 10 |

Feb 10 |

Jan 10 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Euro-Area Detail | Feb 10 |

Jan 10 |

Dec 09 |

3Mo | 3Mo | 6mo | 6mo | 12mo | 12mo | Q-4 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| MFG | 0.9% | 1.3% | 0.3% | 10.6% | 12.6% | 10.1% | 9.0% | 4.2% | 0.9% | 12.3% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Consumer | -0.3% | 0.5% | 0.3% | 2.2% | 9.1% | 1.2% | 2.2% | 1.1% | -0.1% | 5.1% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| C-Durables | -0.6% | 2.6% | -1.5% | 1.4% | 12.2% | 7.3% | 10.5% | -0.3% | -2.5% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| C-Non-durables | -0.2% | 0.3% | 0.6% | 2.8% | 7.5% | 3.1% | 1.3% | 1.5% | 0.6% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Intermediate | 1.5% | 0.8% | -1.1% | 4.6% | 1.8% | -4.2% | 6.2% | 6.9% | 3.6% | 5.1% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Capital | 0.9% | -1.1% | 0.0% | -0.7% | 1.5% | 4.5% | 5.9% | 3.1% | -0.8% | -0.7% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Main Euro-Area Countries and UK IP in MFG | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mo/Mo | Feb10 | Jan10 | Feb10 | Jan10 | Feb10 | Jan10 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| MFG Only | Feb 10 |

Jan 10 |

Dec 09 |

3Mo | 3Mo | 6mo | 6mo | 12mo | 12mo | Q:4 Date |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Germany: | 0.2% | 0.6% | -1.3% | -2.1% | 1.3% | 4.5% | 8.7% | 7.1% | 3.2% | -3.1% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| France: IPxConstruct'n |

0.0% | 1.1% | -0.3% | 3.2% | 6.9% | 0.7% | 5.3% | 3.3% | 2.6% | 4.1% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Italy | 0.2% | 1.7% | -0.6% | 5.3% | 6.8% | 7.6% | 3.8% | 3.0% | -0.6% | 5.3% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Spain | 1.6% | -3.4% | -0.6% | -9.3% | -15.4% | -11.9% | -7.3% | -2.1% | -2.0% | -9.9% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| UK: EU member | 1.3% | -0.9% | 0.9% | 5.5% | 0.5% | 6.3% | -0.7% | 1.5% | 0.1% | 3.3% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief