Global| Feb 10 2009

Global| Feb 10 2009IP Plunges in Main EMU Countries and Beyond

Summary

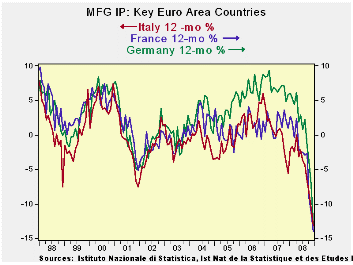

The list of countries reporting steep declines in industrial output continues. In the quarter-to-date (a full quarter now since we have December data) the pace of decline is roughly at a 25% annual rate. And that is steep indeed. [...]

The list of countries reporting steep declines in industrial output continues. In the quarter-to-date (a full quarter now since we have December data) the pace of decline is roughly at a 25% annual rate. And that is steep indeed. Among large economies only Spain saw a rise in IP in December, but that followed a drop of 9.4% in November. Spain’s monthly gyrations are extreme. Its Yr/Yr declines are bit more consistent and consistently weak.

But the BIG NEWS on the day may not have been these weak IP figures as much as the quote attributed to Bundesbank and ECB member Axel Weber who said that the ECB should not be worried about the long term impact of its moves since the economy in Europe was in ‘freefall.’ ‘Freefall’ was apparently the word that Weber himself used. He said the ECB should not worry about ‘lowering rates aggressively.’ This is key statement since last week with weak economic reports all around it, with inflation having fallen more than expected, and with the BOE cutting rates, the ECB chose to standstill. Barely a week later here comes Weber with his guns blazing urging more rapid rate cuts. This is a clear shift for Europe since up to this point there has been a bit more emphasis from the Germans, who tend to be the monetary conservatives, no longer so worried about the stubbornness of inflation. That position had been essentially a reference to the core rate. That concern now seems to have been set aside in favor of concern over the economy itself.

| Mo/Mo | 3-Mo | 6-mo | 12-mo | ||||

| MFG Only | Dec-08 | Nov-08 | Oct-08 | Dec-08 | Dec-08 | Dec-08 | Q-to-Date |

| Germany: | -5.3% | -3.8% | -2.1% | -36.5% | -23.8% | -13.1% | -26.9% |

| France: IP excl Construction | -1.8% | -2.8% | -3.8% | -28.8% | -15.1% | -11.1% | -24.1% |

| Italy | -2.7% | -3.2% | -2.2% | -28.1% | -22.8% | -13.1% | -26.0% |

| Spain | 2.7% | -9.4% | -2.0% | -30.9% | -10.1% | -15.0% | -29.8% |

| UK | -2.2% | -3.0% | -1.6% | -24.1% | -16.6% | -10.2% | -19.1% |

| Mo/Mo are simple percent changes others are at Saars | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief