Global| Dec 11 2009

Global| Dec 11 2009Inflation's acceleration is clear, so is the policy conundrum

Summary

While it would seem to pose a conundrum for the Bank of England, few are expecting any monetary response to the rising inflation trends that are developing in the UK. Both core and headline factory gate prices are showing the same [...]

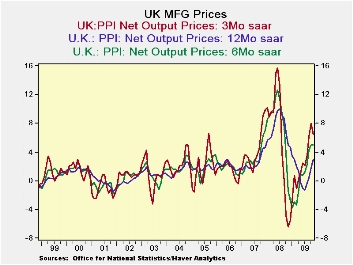

While it would seem to pose a conundrum for the Bank of England, few are expecting any monetary response to the rising inflation trends that are developing in the UK. Both core and headline factory gate prices are showing the same sort of pressure building. Yr/Yr inflation at the producer level already is at 2.9% for the headline and at 2% for the core, levels that would be at or above the ceiling rate were this the CPI (HICP; actually the HICP itself is running at a 2% pace as of September). PPI price trends took a bit of a break in November with the headline rate below its pace of the previous three months; the core showed its smallest rise in four months.

The UK economy is still struggling and getting recovery going is still job-one. So it is not expected that the BOE will react to the rising inflation rate. Indeed, it is hoped that the weakness in the economy will keep these pressures from building and that the current rise proves to be a rogue wave of inflation that is not followed by any others and that dissipates harmlessly on the shores of discretion. That prognosis may prove be correct, but for the moment it seems a bit of wishful thinking. Still, if I were a BOE governor I doubt I would have the stomach to attack inflation now under the circumstances. Even so that does not make it the right thing to do. It is a conundrum of the first order.

| UK PPI MFG net output prices | |||||||

|---|---|---|---|---|---|---|---|

| %m/m | %-SAAR | ||||||

| NOV-09 | OCT-09 | SEP-09 | 3-mo | 6-mo | 12-mo | 12-moY-Ago | |

| MFG | 0.3% | 0.6% | 0.7% | 6.5% | 5.0% | 2.9% | 5.0% |

| Core | 0.1% | 0.5% | 0.5% | 4.8% | 2.7% | 2.0% | 5.1% |

| Core: ex food beverages, tobacco & Petroleum | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief