Global| Apr 24 2008

Global| Apr 24 2008IFO Weakness: A New Trend Lower or a ‘Mild’ Offset to a Spurious Jump?

Summary

Germany’s IFO index has dropped sharply in March to 102.4 from 104.8. Its current conditions index fell to 109.4 from 111.5. The April expectations index moved lower to 96.8 from 98.4. On a Yr/Yr basis the percentage declines in the [...]

Germany’s IFO index has dropped sharply in March to 102.4 from 104.8. Its current conditions index fell to 109.4 from 111.5. The April expectations index moved lower to 96.8 from 98.4. On a Yr/Yr basis the percentage declines in the IFO index accelerated for each of these components (see table below).

The readings for the IFO and its components are not yet dour, but they clearly have weakened and are no longer strong. The Business Climate index stands in the 73rd percentile of its range, a firm reading. The current situation is a bit better than that, lodged at its 78th percentile. Expectations, the forward-looking indicator, are weaker; still standing in the 60th percentile of their range. That is still above the midpoint but longer looking very strong and certainly losing momentum. Expectations readings, while above their range mid point stand at their period average at a value of 96.8.

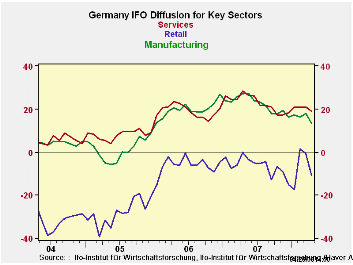

The sector indices tell curious stories. Compared to their respective average values since January of 2001, all are still well above average. But all are not well-off. Retailing is the most curious having moved strongly higher earlier this year even as the euro was gaining in value. But in April it is falling sharply even as it was retaining some of those gains. The message from this sector is not clear. It resides in the 78th percentile of its range. In that respect it is the relative strongest of the sectors in its range since 2001. Wholesaling is the weakest sector residing in the 65th percentile of its range. MFG Construction and retailing are in the low seventieth percentiles of their respective ranges. All of them fell in the month, retailing fell the mostly sharply shedding 10 points in one month. Wholesaling lost over 6 points on its diffusion index. Manufacturing lost about four and one-half points.

It was not a good month for the IFO report that was generally worse than the Zew index has suggested. The IFO’s details are yet to be revealed. A MFG morale report from neighboring France, a fellow EMU member, (also released today) showed that French morale was off and that orders had dropped sharply. That result accords with the Belgian National Bank index released on Wednesday, just one day ago. We are getting confirming signs with similar causes about spreading weakness in the Euro Area. Even the UK’s CBI MFG survey showed a similar pattern of weakness made more nettlesome by reports that more firms were passing through price increases.

The reports for the EMU in the coming months are going to be important. On today’s weakness the Euro shed a large dollop of its recent outsized dollar gains. The ECB rhetoric about tightening rates has done a quick 180-degree turn, suddenly the IMF is pleased with the state of ECB policy and the ECB itself no longer seems to threaten a rate-hiking agenda.

What a difference a few bad economic reports can make. Stay tuned as we try to discern how weak things will get. For its part the German government has not cut its growth rate further for 2008 but has lowered the outlook for 2009. In the face of all the complaining that the euro is too strong, some of this is going have to undergo a credibility check. If the euro is far, far above parity (and seems to suggest that is so) then the recent strength in a number of euro indicators would seem to at risk. More weak readings from the IFO and its companion reports must lie ahead. All this talk of a resilient and robust economy in Europe surely must be about to go by the boards.

| IFO Survey: Germany | ||||||||

|---|---|---|---|---|---|---|---|---|

| Percent: Yr/Yr | INDEX NUMBERS | |||||||

| Apr-08 | Mar-08 | Feb-08 | Jan-08 | Dec-07 | CURRENT | Average | Percentile | |

| Biz Climate | -5.7% | -2.7% | -2.7% | -4.2% | -5.3% | 102.4 | 96.0 | 73.1% |

| Current Situation | -4.2% | -0.7% | -1.1% | -4.3% | -6.2% | 108.4 | 95.2 | 78.6% |

| Biz Expectations | -7.2% | -4.7% | -4.4% | -4.1% | -4.3% | 96.8 | 96.8 | 60.5% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief