Global| Apr 24 2014

Global| Apr 24 2014Ifo Shows Unexpected Strength as Europe Makes Some Progress

Summary

Climate in Germany's Ifo index improved unexpectedly in April. The climate index moved to 14.8 in April from 13.8 in March with current conditions improving to 18.9 from 18.7 as expectations rose to 10.8 from 9.0. The rise in [...]

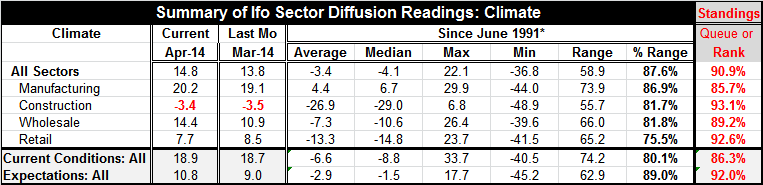

Climate in Germany's Ifo index improved unexpectedly in April. The climate index moved to 14.8 in April from 13.8 in March with current conditions improving to 18.9 from 18.7 as expectations rose to 10.8 from 9.0. The rise in expectations was unexpected as previous indicators had suggested expectations would decline in April. On the other hand, the increase in current conditions was quite small, smaller than expected for April.

Climate in Germany's Ifo index improved unexpectedly in April. The climate index moved to 14.8 in April from 13.8 in March with current conditions improving to 18.9 from 18.7 as expectations rose to 10.8 from 9.0. The rise in expectations was unexpected as previous indicators had suggested expectations would decline in April. On the other hand, the increase in current conditions was quite small, smaller than expected for April.

Sector indices show increases up and down the board with the exception of retailing. The manufacturing index improved to a level of 20.2 from 19.1. Construction posted a small improvement to -3.4 from -3.5. The wholesaling index improved sharply to 14.4 from 10.9. The retailing sector had a setback, falling to 7.7 from a value of 8.5 last month.

The rank standings of the various sectors remain high across the board. The all-sector reading is in its 90.9 percentile, the current conditions reading is in the 86.3 percentile, and expectations stand in the 92nd percentile of their historic queue. By sector, the strongest reading is from retailing at 92.6, despite the back off this month; the weakest reading is from manufacturing which stands in its 85.7 percentile.

There was some anticipation that the expectations index would backtrack because of problems in Ukraine, but that did not happen. But current conditions compensated by being weaker than expected. Still, the strength of the Ifo index is surprising this month.

Beyond Germany

France also released an industry survey. It saw slight backing off in April. France's industry reading has been extremely stable at a moderate level over the past four months. There is no sense in this index of any reaction to events in Ukraine. The French climate index fell back to 100 after edging up to 101 in March with readings of 100 in February and in January in the preceding months. The French index shows deterioration in the trend of IP (industrial production) with that index falling to -15 in April from -10 in March. Orders and demand also withered in April compared to March. The French index shows wavering momentum for an index that already only sits only in the 51st percentile of its historic rank.

The French manufacturing deterioration is worse and its weakness is progressive as the industrial production trend posts readings of -15 in January, -6 in February, -10 in March and -15 in April. These are not the trends that are being sought in a recovering euro area. The recent trend for production in France has been more erratic and flat. The likely trend continues to be a positive number that doesn't show any trend. The industrial trend IP reading sits in the 39th percentile of its historic rank, while the recent trend is in its 43rd percentile and the likely trend in the 61st percentile. These readings all are in clustered around the middle of the distribution for France and are not encouraging.

France and Germany are the two largest countries in the euro area. Their economic circumstances and trends are quite different. France is still struggling to establish a firm toehold for growth. The German economy is operating at a very high level across all sectors.

Spain is showing continued growth in GDP, and both Spain and Greece have been able to enter the capital markets again on favorable terms. Still, the euro area is fighting its way toward a stronger recovery. The process is not yet smooth. European Central Bank President Mario Draghi reiterated today his intent to engage a program of asset purchases if the outlook for inflation worsens. While Europeans deny that they are at risk of deflation, the EMU-wide inflation rate is hovering around a 0.5% annual rate and we are still seeing prices weaken in some places such as in Ireland today where the PPI dropped again on a year-over-year basis.

Europe's recovery has not kicked into a sustainable gear yet. However, the month's flash PMI indices (released yesterday) suggest some improvement is in train. But the early reading on Germany is stronger and for France its moderately improved PMI reading of last month just got weaker, again. The euro area continues to be bifurcated with Germany dragging the EMU metrics higher and everyone else lagging behind and the community logs an erratic trend higher. Will that be good enough?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief