Global| Mar 25 2009

Global| Mar 25 2009IFO Index Drops But Sentiment Drops But Sentiment Makes Some Gains

Summary

The IFO Index fell again in March but the IFO expectations index rose. Expectations are still only in the 16th percentile with this ongoing bounce. The overall business climate and the current situation indices are at lows. The chart [...]

The IFO Index fell again in March but the IFO expectations

index rose. Expectations are still only in the 16th percentile with

this ongoing bounce. The overall business climate and the current

situation indices are at lows.

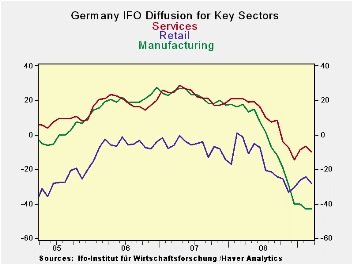

The chart above shows how some of the sector indices based on

diffusion indices are doing. All three pictured indices are falling

sharply. The services and retail sectors have made a small rebound.

Manufacturing is slowing its descent. Manufacturing and the all- sector

index (not pictures) are at the bottom of their range. The wholesaling

and services sectors (wholesaling not pictured) hover around the bottom

10% of their respective ranges. The retail sector is in the bottom 20%

of its range. Construction is nearly midrange, being far less affected

overall – so far.

On the month the manufacturing index ticked a bit lower.

Retailing, services and wholesaling moved a bit lower too. But

Construction showed higher diffusions reading. Contraction in there is

becoming less pronounced. And even though manufacturing deteriorated it

was by the slimmest of margins. In broad terms the IFO reading is in

agreement with the PMI sector indices from Market that show a reduction

in the rate of decline in both MFG and services.

Still, the news from IFO was not good and was not a positive

as some had hoped for. The upshot is that the report weighed on the

euro. However there might be enough evidence of an abatement in the

slowdown for Europe to call for additional stimulus. Today the EU’s

Junker was saying Europe would not simply cave into the US wishes for

more European stimulus because the economy’s spiral was still so

severe. But if the severe phase of the European downturn is abating, a

dollop of stimulus might be helpful. If Europe turns more to look at

the facts of its circumstance in stead of being disagreeable with the

US, it might find that the US urging is pushing it in the right

direction.

| IFO Survey: Germany | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Percent: Yr/Yr | Index Numbers | ||||||||

| Mar 09 |

Feb 09 |

Jan 09 |

Dec 08 |

Nov 08 |

Current | Feb 09 |

Curr/Avg | %tile | |

| Biz Climate | -21.5% | -20.6% | -19.7% | -20.0% | -17.8% | 82.1 | 82.6 | 85.5% | 0.0% |

| Current Situation | -25.8% | -23.5% | -19.7% | -18.1% | -14.2% | 82.7 | 84.3 | 86.2% | 0.0% |

| Biz Expectations | -16.9% | -17.5% | -19.8% | -22.0% | -21.3% | 81.6 | 80.9 | 84.8% | 16.3% |

| average & range since | Jun-91 | ||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief